AI euphoria didn’t die on Thursday—it just ran into reality.

The party tried to keep going. Futures were green, oil slipped on fresh hopes of a breakthrough in the Strait of Hormuz, and the usual suspects (semis, calls, FOMO) were doing their thing. But by the close, the vibe had completely shifted. The major indexes faded. The Nasdaq slipped. The S&P softened. The Dow turned lower. The Russell lagged. The VIX woke up. And the broader market stopped pretending it was invincible.

Wednesday was upside panic. Thursday was what happens when that panic meets the real world.

The Market Was Green in the Morning—Then the World Crashed the Party

At the open on Thursday, everyone wanted to believe the clean story: ships might finally move through Hormuz, crude would stay tame, and the AI train could keep rolling without interruption. Traders leaned in. Futures firmed. Optimism felt almost reasonable.

Then the headlines turned messy. Reports of renewed U.S. strikes, warships under fire, explosions in Iran—suddenly the relief rally didn’t feel so relieving. That’s the brutal part about geopolitics-driven moves: they reverse as fast as they appear. One peace headline knocks oil lower. One military update brings fear roaring back.

This is exactly why Thursday felt so different from Wednesday. The market tried to pull the future forward. The future pushed back—hard.

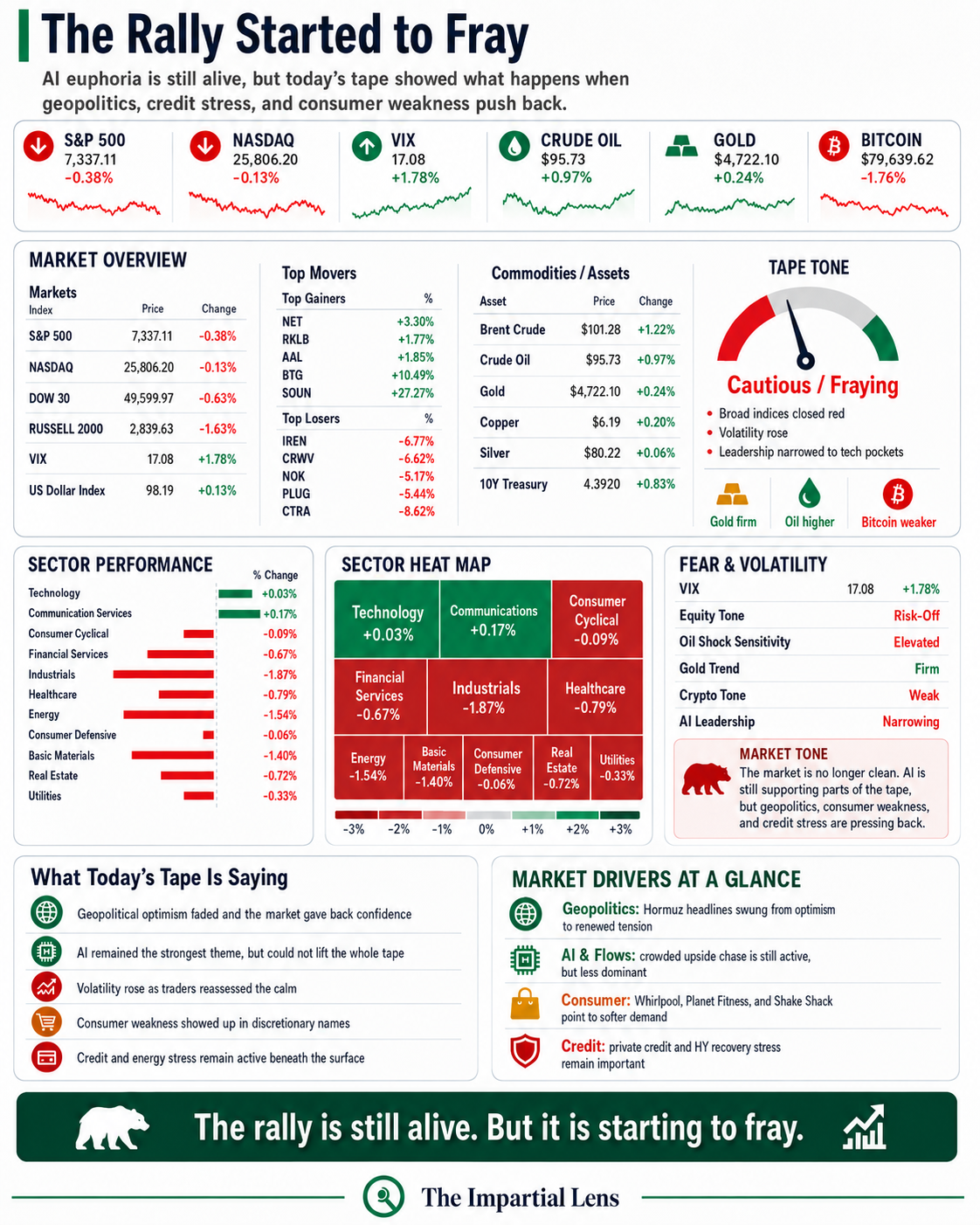

The Screenshot Doesn’t Lie: This Wasn’t Broad Strength

Check any market dashboard from Thursday and the picture was clear. Tech was barely hanging on. Communication Services eked out a small gain. Everything else—Financials, Industrials, Healthcare, Energy, Consumer Defensive, Real Estate, Utilities—closed in the red.

That’s not a healthy rally. That’s a market leaning on a couple of tired pillars while the rest of the tape starts to sag. Wednesday, AI dragged the whole thing higher. Thursday, even AI couldn’t quite carry the load against geopolitics, credit jitters, and growing consumer fatigue.

AI Is Still the Story—But It’s Getting Crowded and Noisy

Let’s be honest: the AI buildout is real. Explosive demand for chips, power, infrastructure, and agents isn’t going away. Goldman’s wild projection of 120 quadrillion tokens monthly by 2030 gives you a sense of the scale.

But the trade around AI is starting to feel very crowded. Record call option activity. “Semi-irrational” chase mode. Headlines screaming that nobody owns enough upside. These aren’t early-cycle signals. They’re late-momentum warnings. When everyone piles into the same narrative at once, even the best story can become a dangerous, fragile trade.

The Consumer Is Starting to Say “No”

This was the part that really stood out on Thursday.

Whirlpool tanked after warning of a “recession-level” slump in appliances. Planet Fitness dropped hard on slowing memberships. Shake Shack got hit as McDonald’s flagged a faltering consumer. These aren’t isolated data points. They’re signs that real people are pulling back on big-ticket purchases, expensive gym contracts, and even casual dining.

AI can supercharge capex and data centers all it wants. But if Main Street weakens, the broader economy eventually feels it. Thursday’s tape started reminding everyone that the consumer still matters.

Credit Is the Quiet Shadow Under the Rally

While equities chased narrative, credit markets kept whispering warnings. Jeffrey Gundlach talking about private-credit “bagholders.” High-yield recovery rates plunging to 35%—the lowest since COVID. BlackRock cutting values on private-credit funds. These aren’t screaming headlines, but they matter.

Equities trade hope. Credit trades survivability. Right now, those two messages are diverging, and history shows they can’t stay apart forever.

Oil Remains a Messy Hinge

Crude slipped on peace hopes, which helped the relief narrative. But the underlying picture is still chaotic—UK jet fuel rationing risks, Iranian refinery issues, suspicious tanker movements, and fresh military activity. Lower oil is great for inflation and consumers… until it isn’t, because the energy system still looks unstable.

This isn’t a clean disinflation story. It’s a geopolitical risk premium swinging wildly.

Gold Quietly Doing Its Job

Meanwhile, gold stayed firm. China keeps buying. The metal refuses to roll over even as equities try to rally. That strength isn’t screaming panic, but it’s a clear message: investors still want upside, but they’re not fully trusting the system.

What Thursday’s Action Really Means

- AI is alive — but no longer effortlessly carrying everything.

- The rally is narrowing — a few names and sectors doing the heavy lifting.

- Volatility is back — the VIX jump showed Wednesday’s calm was fragile.

- Energy is unresolved — peace headlines help, but risks remain.

- Consumer pressure is real — people are starting to cut back.

- Credit stress lingers — underneath the surface, balance sheets are feeling it.

The Impartial Lens View

This market isn’t broken. But it’s no longer clean.

The AI story is powerful. The liquidity backdrop is supportive. Call-chasing momentum can still squeeze higher. But the other side of the ledger is getting louder: weakening consumers, private credit cracks, high-yield stress, oil instability, geopolitical whiplash, and gold’s quiet insurance bid.

This is classic late-stage momentum behavior. Not a sudden crash. Not blind panic. Just more and more cracks appearing while the strongest narrative keeps pulling prices higher.

Wednesday was pure upside panic.

Thursday was the first clear sign that panic is meeting resistance.

The rally is still breathing.

But it’s starting to fray at the edges.

And that’s exactly when things get interesting.