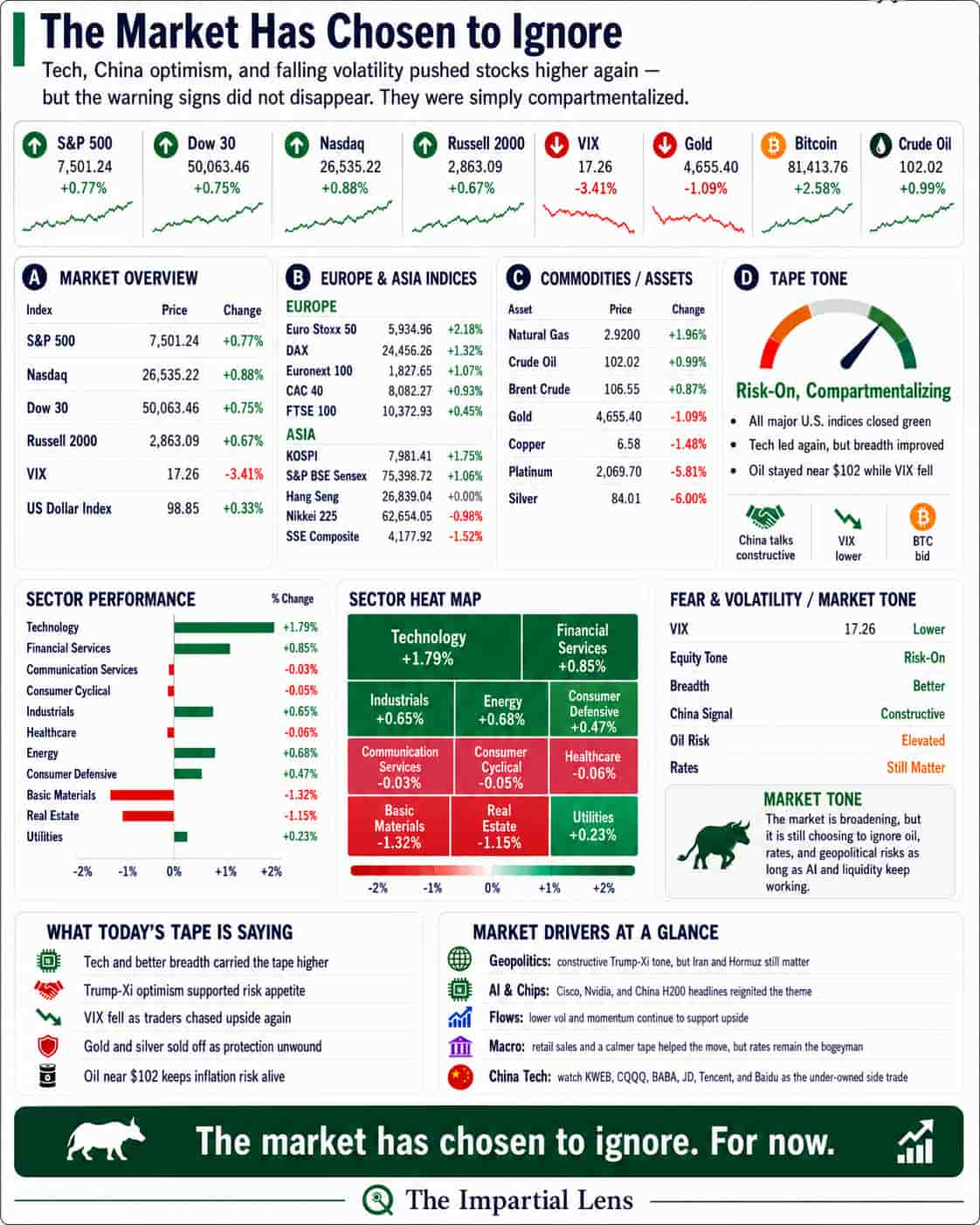

The market rallied again yesterday — and this time, the move felt broader. The S&P 500 climbed 0.77%, the Nasdaq rose 0.88%, the Dow added 0.75%, and even the Russell 2000 joined in with a 0.67% gain. Volatility eased as the VIX dropped more than 3%, Bitcoin bounced, and risk appetite returned with a vengeance.

At first glance, it looked like a healthy, broad-based risk-on session. But dig a little deeper, and the story becomes far more nuanced. The market isn’t calm because the risks have vanished. It’s calm because it has neatly compartmentalized them — placing the good news in one box and the warnings in another, then choosing which box to open.

Better Breadth, Same Dependence

Yesterday’s action was cleaner than recent sessions. Major indices all closed green, and the sector heatmap showed genuine participation: Technology surged 1.79%, Financial Services rose 0.85%, Industrials gained 0.65%, and Energy turned positive.

That improved breadth matters. A rally supported by multiple sectors tends to last longer than one carried solely by the Magnificent Seven.

Yet the leadership told the real story. The day’s biggest winners clustered around AI infrastructure, chips, China exposure, and high-beta growth names. Nvidia stayed strong, Cisco exploded higher on its AI infrastructure outlook, and momentum plays like POET, Ondas, and others piled in.

This was broader than the day before — but it was still very much a tech-led risk chase, not a classic value-led recovery. The gravitational center of this market remains AI, chips, data centers, China, and liquidity.

Trump-Xi Gave the Market Permission

The clearest catalyst was the constructive tone surrounding the Trump-Xi summit. Headlines spoke of a “fantastic day,” potential 200-jet Boeing orders, China offering help around Hormuz, and approvals for roughly 10 Chinese firms (including Alibaba, ByteDance, Tencent, and JD.com) to buy Nvidia H200 chips.

The market got exactly what it craved:

- A trade-relief narrative

- A China-tech story

- An AI-export extension

- A geopolitical cooling signal

It didn’t need a full resolution — just enough positive narrative to justify buying the next leg higher. And that’s precisely what it received.

China Tech: From Side Note to Squeeze Candidate

China tech is no longer an afterthought. With U.S. AI names becoming increasingly crowded, the combination of summit optimism and potential Nvidia chip access has traders revisiting under-owned Chinese names like BABA, JD, TCEHY, BIDU, PDD, NIO, LI, XPEV, and BYDDY — along with ETFs such as KWEB and CQQQ.

These stocks now function as a secondary AI and liquidity expression. The market doesn’t need them to fully catch up to U.S. leaders. It only needs investors to realize they’re still underweight. That’s how violent squeezes begin.

Cisco Reignites the AI Infrastructure Trade

Cisco’s surge was significant because it expanded the AI story beyond just Nvidia. The narrative now comfortably includes networking, optics, power, cooling, data centers, cloud infrastructure, and more.

Every time the AI theme broadens, the market discovers fresh pockets of stocks to chase. The risk? More and more capital flows into the same overarching idea — until AI stops feeling like a sector and starts feeling like the market’s operating system.

The Market Is Compartmentalizing Risk

This is the defining feature of the current tape: “Compartmentalize & move on.”

One box holds the bullish narrative:

- Tech is working

- China talks are constructive

- AI chips may flow again

- Breadth is improving

- Volatility is falling

- Bitcoin is bid

The other box contains the warnings:

- Rates remain the ultimate bogeyman

- Oil hovers near $101

- Gold and silver sold off sharply

- Geopolitical and shipping risks persist

- Gamma remains stretched

- Downside protection is being ignored

- New lows continue beneath the strong headline indices

Yesterday, the market chose the first box. That doesn’t mean the second box disappeared.

The Warnings That Refuse to Vanish

Rates continue acting as the foundation beneath everything. Sustained bond weakness has rarely been a long-term positive for equities. Higher rates eventually pressure valuations, borrowing costs, consumer credit, and long-duration growth stocks.

Oil at ~$101 is no small detail. Despite the Hormuz relief headlines, crude refused to collapse. That keeps inflation risk and geopolitical tension alive.

Gold and silver — the market’s traditional insurance policies — were sold aggressively. Investors chose to shed protection and chase risk instead.

The VIX dropping more than 3% feels comforting on the surface, but in today’s environment, falling volatility often just fuels even more mechanical risk-taking and gamma-driven upside.

Investor Translation: What Should You Do?

This remains a momentum-driven market. You don’t blindly short a tape where every major index is green, volatility is falling, and positive China/AI narratives are flowing. That’s a fast way to get run over.

At the same time, you shouldn’t blindly trust a market that’s growing skilled at ignoring warning lights. The rally is supported by real tailwinds, but the risks — elevated oil, sticky rates, crowded positioning, and geopolitical chokepoints — haven’t gone away. They’ve simply been placed in boxes.

The market isn’t saying “risk is gone.”

It’s saying, “Risk can wait. The upside is still working.”

The Impartial Lens

Yesterday wasn’t just a good day for stocks. It was a good day for the market’s ability to selectively ignore. The rally broadened, but the mindset narrowed. The market trained itself once again to look past risk — as long as the AI and liquidity story stays intact.

That approach works beautifully during melt-ups… until the day one of those ignored boxes refuses to stay closed.

Stay alert, stay nimble, and keep both boxes in view.

What do you think — is this compartmentalization bullish or dangerous? Drop your thoughts in the comments below.