The party was loud. The music was pumping. Tech stocks were dancing like it was 2024 all over again.

Then the lights flipped on.

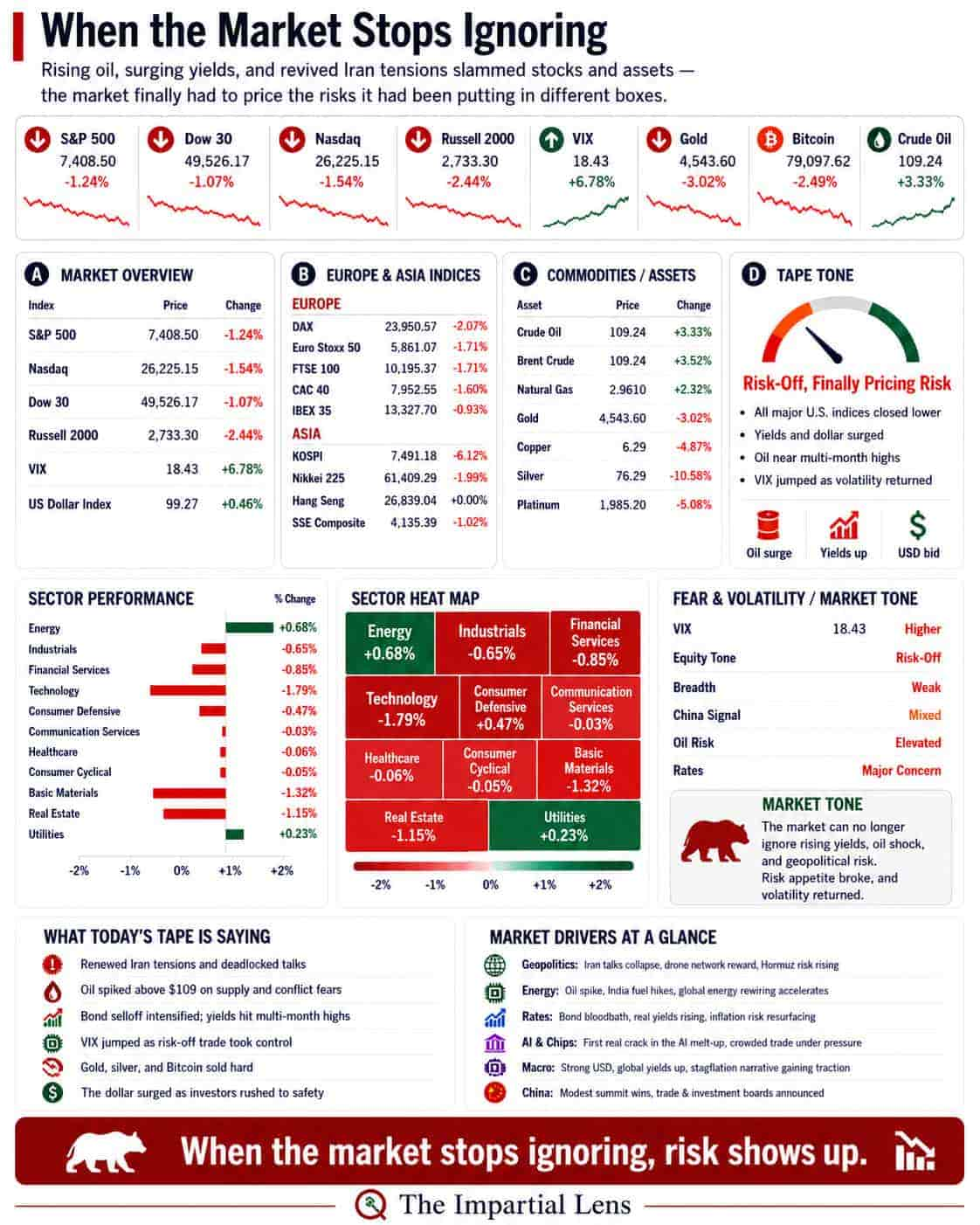

On Friday, the market didn’t just pause — it sobered up hard. The S&P 500 dropped more than 1%, the Nasdaq fell over 1.5%, and the Russell 2000 got absolutely hammered, down more than 2%. Volatility spiked, oil exploded above $109, bonds sold off aggressively, and suddenly everyone remembered that risks still exist.

This wasn’t a normal red day. This was the tape saying: *“Enough with the compartmentalization.”*

Friday’s Dashboard Turned Blood Red

Thursday’s vibe? Green indices, collapsing volatility, China hope, and AI supremacy.

Friday? A completely different movie.

– S&P 500: ~7,408 (-1.24%)

– Nasdaq: ~26,225 (-1.54%)

– Dow: ~49,526 (-1.07%)

– Russell 2000: 2,733 (-2.44%)

– VIX: 18.43 (+6.78%)

– DXY: 99.27 (+0.46%)

Textbook risk-off. Dollar bid. Volatility bid. Oil bid. Stocks offered. Small caps crushed.

Oil Just Became the Main Character Again

Crude oil surged to roughly $109.24, up over 3%. Brent matched it. Natural gas joined the party.

This isn’t just a price spike. Oil has become the transmission mechanism for the entire macro nightmare:

Oil → Inflation

Inflation → Higher yields

Higher yields → Lower valuations

Lower valuations → Tech pain

Tech pain → Index pain

Index pain → Sentiment collapse

The headline drivers were crystal clear: renewed U.S.-Iran tensions, stalled talks, threats around the Strait of Hormuz, tightening gasoline inventories, and India hiking fuel prices. The market isn’t just worried about the price of oil anymore — it’s worried that energy logistics and chokepoints are becoming structural problems.

A one-day spike can be ignored. A structural energy shock cannot.

Iran Risk Is Back, and It’s Not Playing Nice

The brief optimism from the Trump-Xi summit evaporated faster than morning dew. Trump reportedly shot down Iran’s latest proposal, talks remained deadlocked, and the market finally realized it can’t have it all: a China thaw and contained geopolitical chaos.

China progress is nice.

But $109 oil and rising yields speak louder.

Bonds Stopped Whispering — They Started Shouting

For days the bond market had been sending quiet warnings. On Friday it screamed.

Headlines screamed “Bond Bloodbath” for good reason. When Treasuries sell off alongside surging oil, you don’t get a clean growth signal — you get a cost-of-capital shock. And nothing reprices faster than long-duration assets when that happens.

That includes the entire AI complex.

The AI Melt-Up Just Hit an Air Pocket

The AI trade didn’t die on Friday, but it looked mortal for the first time in a while.

We’ve reached the ridiculous stage where everything is trying to slap an AI label on itself. Memory stocks. Data centers. Nuclear. Even Ford is apparently an AI company now. That’s not sustainable leadership — that’s late-cycle froth.

Crowded trades don’t need the story to break. They only need liquidity to tighten.

On Friday, liquidity tightened. Oil up. Yields up. VIX up. Dollar up. Risk appetite down. The crowded long got shaken.

Small Caps Were the Canary

The Russell 2000 getting hit hardest was no accident. Smaller companies feel higher rates, higher energy costs, and tighter financial conditions first. When the small caps underperform this badly, it’s rarely just rotation — it’s tightening.

The mega-cap AI names may still have endless capital. The rest of the market? Not so much.

Even the “Safe Havens” Got Hit

Gold sold off hard. Silver got crushed. Bitcoin dropped back below $80,000.

This wasn’t a clean flight to safety. This felt like de-risking and liquidation. When both stocks and traditional hedges fall together, investors aren’t rotating — they’re raising cash.

What Friday’s Tape Was Really Saying

1. The market stopped ignoring risk

2. Oil is back in the driver’s seat

3. Bonds are the main event now

4. AI is powerful but vulnerable to liquidity shifts

5. Small caps are flashing warning lights

6. The stronger dollar is tightening conditions globally

7. This was global risk-off — Europe and Asia confirmed it

So… Is the Rally Dead?

Not necessarily.

AI momentum can recover. Dip buyers might show up. Oil could pull back. Bonds could stabilize. China talks could improve.

But the **easy part** of this rally — the part where the market could blissfully ignore oil, rates, geopolitics, and froth — just ended **on Friday**.

The rally has been priced for perfection. On Friday, perfection cracked.

The Only Questions That Matter Now

– Can oil cool off quickly?

– Will the bond market stabilize?

– Does the dollar keep tightening financial conditions?

– Can AI leadership regain control?

If the answer to most of these is “no,” Friday was the first real warning shot of a much bigger problem.

If the answer is “yes,” the bulls get another chance to push higher.

Either way, the market just reminded everyone:risk still matters.

The easy money was made by ignoring reality. The next phase will be made by those who respect it.

Stay sharp out there.

The tape doesn’t lie — it just takes its time delivering the message.