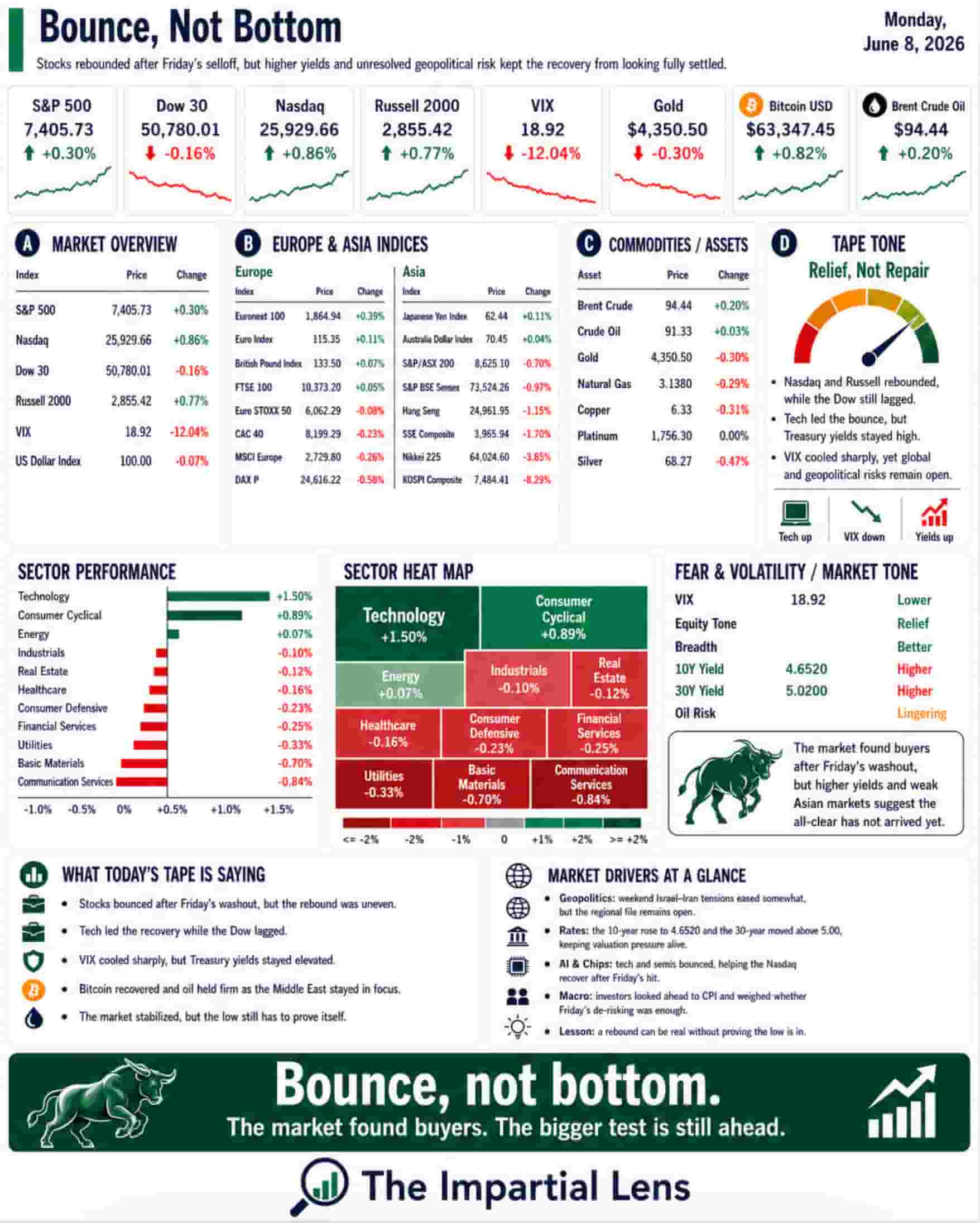

Stocks bounced after Friday’s selloff, but the bigger question is whether this was real repair or just a reflex move after a crowded trade got hit.

Monday gave investors the thing they always want after a rough Friday: green on the screen.

Stocks rebounded. Bitcoin caught a bid. Oil pared its overnight jump. Tech recovered some ground. Israel and Iran both signaled some willingness to pause direct strikes after pressure from Washington.

So yes, the tape looked calmer.

But calmer is not the same as fixed.

That is the main lesson from Monday.

After Friday’s sharp selloff, the market needed to show whether buyers were returning with conviction or simply buying the first dip because that has worked for years. The old saying is that markets do not usually bottom on Fridays. Monday tested that idea.

For now, the answer is mixed.

The bounce was real.

The repair is still unproven.

Friday Still Matters

Friday was not just a bad day. It was a warning shot.

The jobs report came in stronger than expected. That sounds good in the real economy. But in the market economy, strong labor data can mean fewer rate cuts, higher yields, and a Fed with less room to help.

That hit the most crowded areas first.

Semis sold off. Tech weakened. Volatility jumped. The dollar rose. Crypto cracked. Leveraged trades were forced to adjust. Options positioning made the move sharper.

That matters because forced selling does not always end in one session.

When markets fall because investors voluntarily take profits, the damage can be contained.

When markets fall because leverage, options, and positioning start feeding on themselves, the aftershocks can last longer.

Monday’s bounce did not erase that.

It only gave the market a chance to prove the selling was temporary.

The Middle East Did Not Take The Weekend Off

The geopolitical file stayed open.

Israel and Iran exchanged strikes over the weekend. Trump pushed both sides toward restraint. Iran declared an end to military operations against Israel but warned it would respond if Israel continued operations against Hezbollah in Lebanon. Netanyahu said Israel was holding fire “for now,” but rejected Iran’s red line on Lebanon.

That is not a clean ceasefire.

That is a temporary pause with conditions attached.

Markets like clean stories. This is not one.

The Middle East still matters because it runs straight through oil, inflation, shipping, defense spending, and political risk. Hormuz remains the transmission channel everyone is watching.

If the Strait stays disrupted, oil risk rises.

If oil risk rises, inflation pressure can return.

If inflation pressure returns, bond yields matter more.

And if yields matter more, expensive technology and AI trades become more vulnerable.

That chain has not gone away.

Monday simply gave it a quieter soundtrack.

Oil Is Still The Swing Factor

Oil pared gains Monday after de-escalation comments, but the risk did not vanish.

JPMorgan’s warning was straightforward: if Hormuz remains blocked beyond June, each additional month of disruption could lift average prices meaningfully in the second half of the year as inventories are depleted.

That is the part investors should understand.

Oil shocks do not always hit all at once.

They can build slowly.

First, the market uses inventories.

Then workarounds get stretched.

Then shipping costs rise.

Then consumers feel it.

Then inflation expectations adjust.

Then central banks get more cautious.

By the time the average person notices, the market has usually been wrestling with it for weeks.

That is why oil remains central even on days when crude is not screaming higher.

AI Rebounded, But The Fragility Problem Remains

Tech bounced Monday, helped by news around Nvidia, SK Hynix, Intel, Google, and Apple’s AI announcements.

But the bigger issue is not whether AI is dead.

It is not.

The issue is whether the AI trade became too crowded, too leveraged, and too dependent on constant good news.

Friday exposed that risk.

Several reports pointed to forced selling, leveraged ETF rebalancing, rising correlations, and pressure in semis. That is not about AI disappearing. It is about market structure.

A great theme can still become a dangerous trade if everyone owns the same version of it.

That is the difference between a business story and a positioning story.

AI may still be transformative.

But the trade around it can still become fragile.

The Consumer Is Still Strained

Monday also brought reminders that the real economy is not as shiny as the index.

Restaurants remain under pressure as the tax-refund boost fades. Campbells pointed to continued at-home cooking trends. Bankruptcy filings rose year over year in May. Mortgage payments remain historically painful. Labor market expectations weakened in the NY Fed survey even as inflation expectations dipped.

That matters because the market keeps pricing a soft landing.

But the consumer is not one thing.

Higher-income households can keep spending.

Lower- and middle-income households feel food, insurance, rent, energy, and borrowing costs much more directly.

The index can bounce while the household budget does not.

That is not contradiction.

That is the modern market.

The Real Read

Monday was better than Friday.

But it was not a clean bill of health.