Markets love a clean narrative. On Monday they got two stories instead — and they flatly refused to pick just one.

One story was genuinely good for the broader tape: real progress in U.S.-Iran talks sent oil prices lower again and eased the biggest geopolitical energy risk in months. The other story was bad news for the market’s favorite trade: tech, especially anything tied to AI, got sold hard as investors started asking whether the spending spree has finally gotten ahead of the returns.

The market didn’t panic. It rotated. And that rotation told us something important.

Oil Relief Is Real — And It Matters

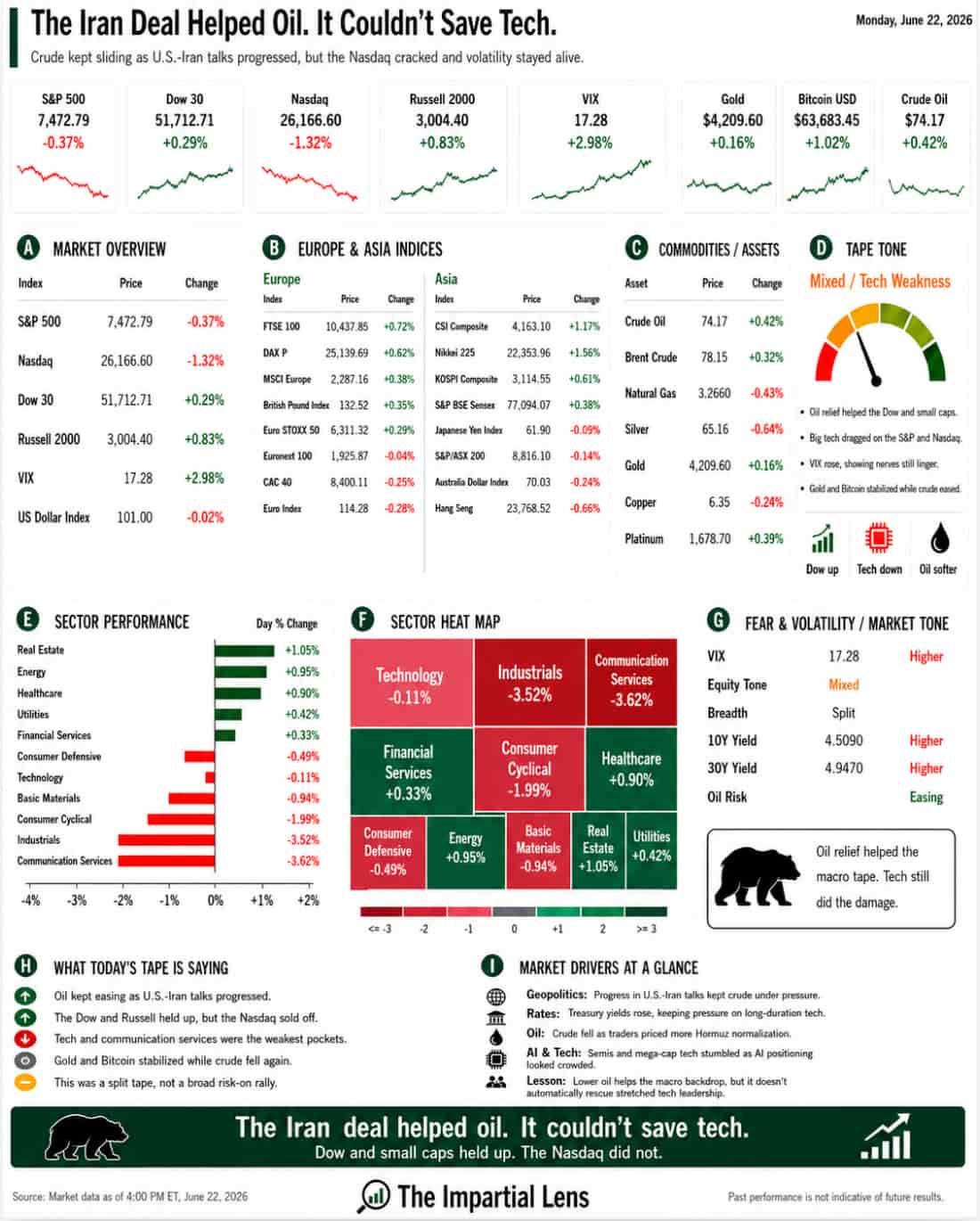

Crude kept sliding as Washington issued an Iran-related oil license and negotiators in Switzerland made headway on ship passage, frozen assets, and keeping communication lines open. The Strait of Hormuz stayed open. Prices responded: crude fell 0.42% to $74.17.

That move wasn’t just about barrels. Lower oil is lower inflation pressure, lower transportation costs, lower consumer stress, and less anxiety at the Fed. It’s oxygen for risk assets in general.

The U.S.-Iran process is still fragile — inspections, sanctions plumbing, and regional trust don’t normalize overnight — but markets correctly priced out the worst-case energy shock for now. That relief showed up in several places:

- Dow gained 0.29%

- Russell 2000 rose 0.83%

- Gold caught a bid, up 0.16% to $4,209.60

- Bitcoin rose 1.02% to $63,683

So far, so good. But the broader market didn’t follow the script.

Tech Took the Hit — And It Wasn’t Random

While small caps and the Dow celebrated cheaper energy, the S&P 500 slipped 0.37% and the Nasdaq dropped 1.32%. The VIX jumped 2.98% to 17.28.

The pressure wasn’t one bad headline. It was the growing sense that the AI trade has entered a more dangerous phase. Here’s what’s piling up:

- Semiconductors are increasingly compared to dot-com era extremes.

- AI-related capital spending is raising serious questions about future depreciation and returns.

- Server rental costs are softening in places.

- China’s open-source models are getting dramatically cheaper and more competitive.

- Amazon is now willing to sell its Trainium chips to outsiders.

- Microsoft wants to own more of the infrastructure the models run on.

- SpaceXAI is turning compute into a standalone business.

- Chevron just signed long-term power deals specifically to feed Microsoft’s AI expansion.

That’s not a list of random news items. It’s a signal that AI has stopped being a pure growth story. It has become a capital-spending story, an energy story, a chip story, a depreciation story, a geopolitical story, and a valuation story — all at once.

The companies are real. The demand is real. The spending is real. But when too much future success is already priced in, even real progress can feel like a letdown.

This Wasn’t a Classic Risk-Off Day

Monday looked strange on the surface:

Small caps up. Dow up. Gold and Bitcoin up. Oil down.

S&P and Nasdaq down. Volatility up.

That’s not fear. That’s rotation and stress testing. Investors are trying to separate two things that used to move together:

- Macro relief from lower oil and calmer inflation expectations.

- Valuation risk inside the concentrated AI leadership.

For weeks the hope was simple: Iran progress → lower oil → lower inflation fears → friendlier Fed → broad stock rally. Monday showed the harder version. Oil can fall and tech can still struggle. A calmer Middle East can reduce one pressure point while another opens inside AI valuations.

The Fed (and Kevin Warsh) Still Loom Large

None of this happens in a vacuum. Kevin Warsh’s recent message — forward guidance is gone, inflation credibility is the priority — is still echoing. The market can no longer assume the Fed will talk every step of the way toward easier policy.

Tech valuations are extremely sensitive to the price of money. If yields stay contained, expensive growth stories can breathe. If yields rise, every far-out earnings promise gets discounted harder and faster.

That’s why the next few weeks matter so much: Core PCE, global PMIs, Micron earnings, and a steady stream of Fed speakers. The market might want to focus on the Iran deal. The Fed still controls the price of money — and right now, tech depends on that price more than almost anything else.

The Real Read

Monday was a split decision, and the market told us exactly what it thinks.

The Iran deal helped. Crude fell. The worst energy shock was avoided. That relief is real and it showed up in small caps, the Dow, gold, and Bitcoin.

But oil relief couldn’t save tech.

The market’s leadership remains heavily concentrated in AI, semiconductors, big tech, cloud, data centers, and compute infrastructure. That leadership is now under real scrutiny. Investors are asking harder questions:

- Is the spending producing returns fast enough?

- Are semis priced for perfection?

- Are China’s cheaper models a bigger threat than we thought?

- Are hyperscalers spending too much, too fast?

- Are power and data-center bottlenecks becoming the new constraint?

- Are traders still in this trade because they believe — or because they’re afraid of missing it?

The Iran deal lowered one risk. It couldn’t paper over the growing doubts about how much future perfection is already baked into AI prices.

That’s the market we’re in now: one that can celebrate cheaper oil while simultaneously stress-testing its most crowded trade. The rotation has started. How far it goes depends on what comes next from the Fed, from earnings, and from whether AI can deliver returns that justify the trillions still being poured in.