Wednesday looked calmer.

That does not mean the market looked healthy.

After Tuesday’s tech-led selloff, investors came into Wednesday looking for proof that the AI trade could stabilize. They got some relief, but not a clean answer.

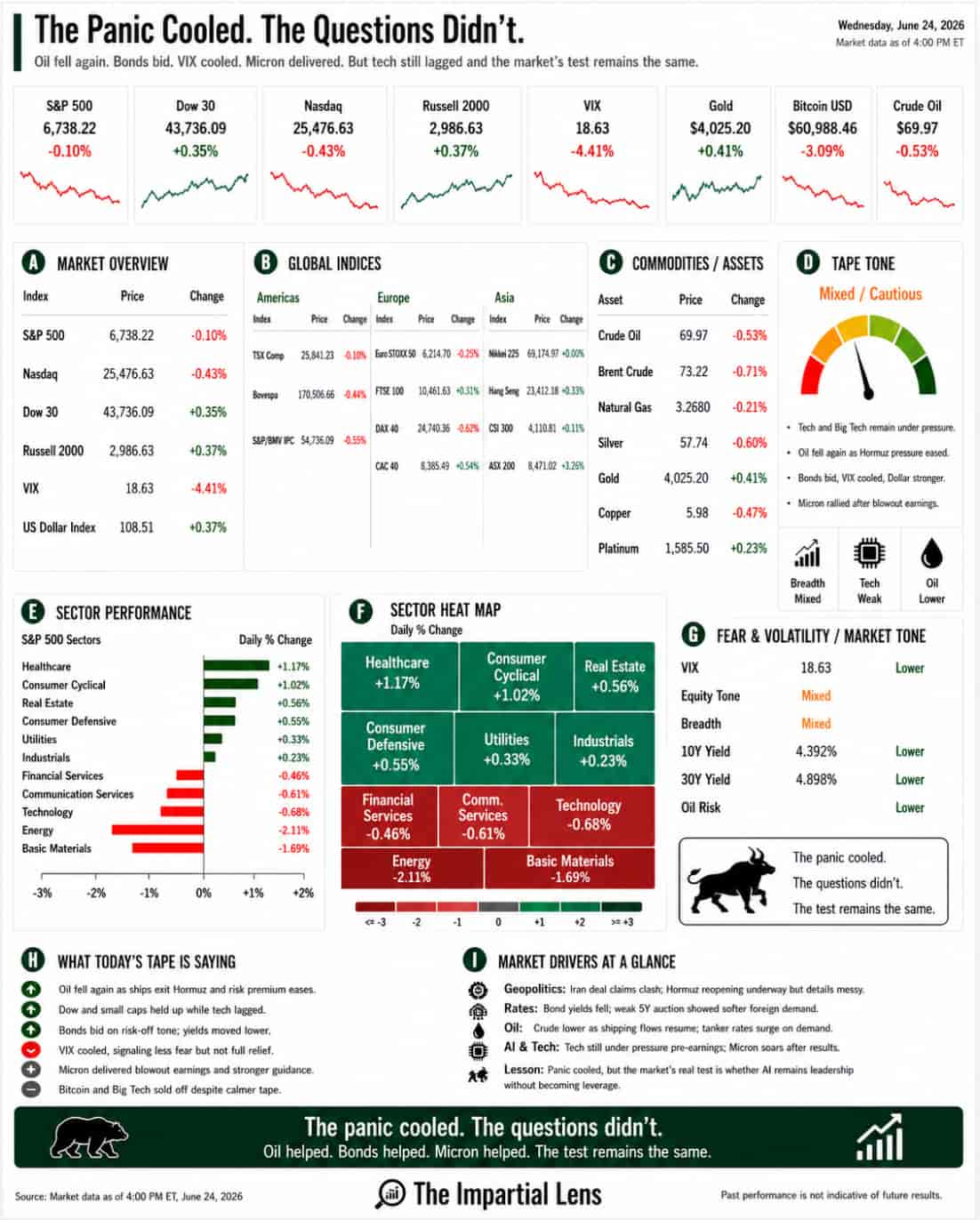

The Dow rose 0.35%. The Russell 2000 gained 0.37%. The S&P 500 slipped 0.10%. The Nasdaq fell 0.43%.

That is not a crash.

But it is not a convincing recovery either.

The VIX fell 4.41% to 18.63, which tells us fear cooled. Crude oil dropped again, down 0.53% to $69.97. Brent fell 0.71% to $73.22. Gold rose 0.41% to $4,025.20. Bitcoin fell hard again, down 3.09% to $60,988.

So the surface message was simple:

The panic eased.

But the pressure points stayed open.

Tech Did Not Fully Bounce

The most important part of Wednesday was what did not happen.

Tech did not roar back.

The Nasdaq remained lower. Technology fell 0.68%. Communication services slipped 0.61%. Financials were down 0.46%. Energy fell 2.11%. Basic materials dropped 1.69%.

That matters because the market’s biggest question is no longer whether oil can keep falling.

Oil is already falling.

The bigger question is whether AI and big tech can keep carrying the market.

For months, investors treated AI leadership as the answer to almost every concern. Higher rates? AI can offset it. Expensive valuations? AI can justify them. Slower growth? AI can power earnings. Capex concerns? AI demand will be large enough.

That worked while the trade kept rising.

But now the tone has changed.

The headlines are no longer just about growth. They are about crowded positioning, leverage, semiconductor pressure, memory expectations, AI researcher departures, dollar strength, data-center constraints, and whether everyone has the same trade on.

That is a different environment.

AI is still powerful.

But the market is no longer giving it a free pass.

Micron Became The Test

Micron was the obvious focal point.

After the close, Micron delivered blowout earnings and stronger guidance. That matters because memory is at the center of the AI buildout. If Micron had disappointed, the pressure on semiconductors could have worsened quickly.

Instead, the stock helped calm the after-hours tape.

But the setup before earnings was already intense. Sentiment was extremely high. Expectations were elevated. Investors were not asking whether AI demand exists. They were asking whether the market has already priced too much of it.

That is the key distinction.

Good earnings can support the story.

But they do not automatically erase crowding risk.

When a trade becomes this popular, the bar moves higher. Strong results are expected. Guidance must be better. Margins must hold. Capex must make sense. Supply must stay tight enough to support pricing, but not so tight that costs explode.

That is a narrow path.

Micron helped.

But the AI trade still has to walk that path.

Oil Kept Falling, But The Story Got Messier

Oil continued to come out of the market.

The Strait of Hormuz reopening story gained more traction. Reports said dozens of ships exited the Strait in the past day. The UN-led evacuation corridor began moving. U.S. officials argued that Iran’s leverage over Hormuz had been reduced.

That helped push crude lower.

But the political story remains messy.

Trump says Iran was forced into major concessions. Iran says the deal represents a U.S. defeat. Washington says unfrozen Iranian funds will be overseen and restricted to food and medicine. Tehran’s public statements do not match Washington’s version. Hormuz tolls, insurance, tanker rates, and ship passage issues remain part of the dispute.

So yes, oil is lower.

But lower oil does not mean the geopolitical story is settled.

The market is trying to treat Hormuz as a solved problem.

The details say otherwise.

And the tanker market is already telling a more complicated story. Rates have surged as importers rush to secure cargoes while the window is open. That means energy risk has shifted. It is no longer just about whether oil can move. It is about what it costs to move it, who controls the route, and whether confidence returns.

Lower crude helps.

But the plumbing still matters.

Bonds Caught A Bid

The bond market also mattered.

Treasuries were bid as oil fell and risk appetite stayed uneven. The 10-year yield moved lower. The 30-year yield fell. The 5-year yield dropped sharply. The dollar stayed firm.

That is not the kind of backdrop that screams easy risk-on.

It looks more like a market hiding in quality while trying to decide whether tech weakness is contained.

That is important.

When yields fall because inflation pressure cools, that can support stocks.

But when yields fall because investors are seeking safety, that sends a different message.

Wednesday looked closer to the second version.

Oil helped. Bonds helped. Volatility cooled.

But tech still could not take full control.

The Sector Tape Was Split

The sector map showed a market trying to rotate.

Healthcare rose 1.17%. Consumer cyclical gained 1.02%. Real estate, consumer defensive, utilities, and industrials were positive. That helped keep the broader tape from looking worse.

But the old leaders remained under pressure.

Technology was negative. Communication services were negative. Financials were negative. Energy and basic materials were weak.

That is the split.

The market is not falling apart.

But leadership is changing, and not in a clean way.

The Dow and Russell held up. The Nasdaq lagged. VIX cooled. Oil fell. Gold caught a bid. Bitcoin sold off.

That is not panic.

It is a market searching for a new center of gravity.

The Real Read

Wednesday was a cooling-off day.

The market did not collapse after Tuesday’s AI shock. That matters. Volatility fell. Small caps held up. The Dow rose. Defensive and cyclical pockets found support. Micron’s results helped repair some confidence after the close.

But the deeper questions remain.

Is the AI trade still in leadership, or has it become crowded?

Can semiconductors keep justifying the expectations built into them?

Can lower oil prices help the market if tech keeps leaking?

Can bonds support equities if yields are falling for the wrong reason?

Can the Iran deal keep crude under pressure while the political details remain contradictory?

Can the market rotate without losing the group that carried it?

That is the real story.

The panic cooled.

But the questions did not.

The market is no longer just trading Hormuz. It is no longer just trading oil. It is no longer just trading Fed expectations.

It is a trading belief.

Belief that AI spending will pay off.

Belief that semis can keep delivering.

Belief that oil relief will cool inflation.

Belief that the Fed can stay credible without breaking risk assets.

Belief that crowded trades can unwind gently.

That is a lot of belief for one market to carry.

Oil helped.

Bonds helped.

Micron helped.

But the market’s real test is still the same:

Can AI remain leadership without becoming leverage?