Monday gave the market what it wanted.

A tech bounce.

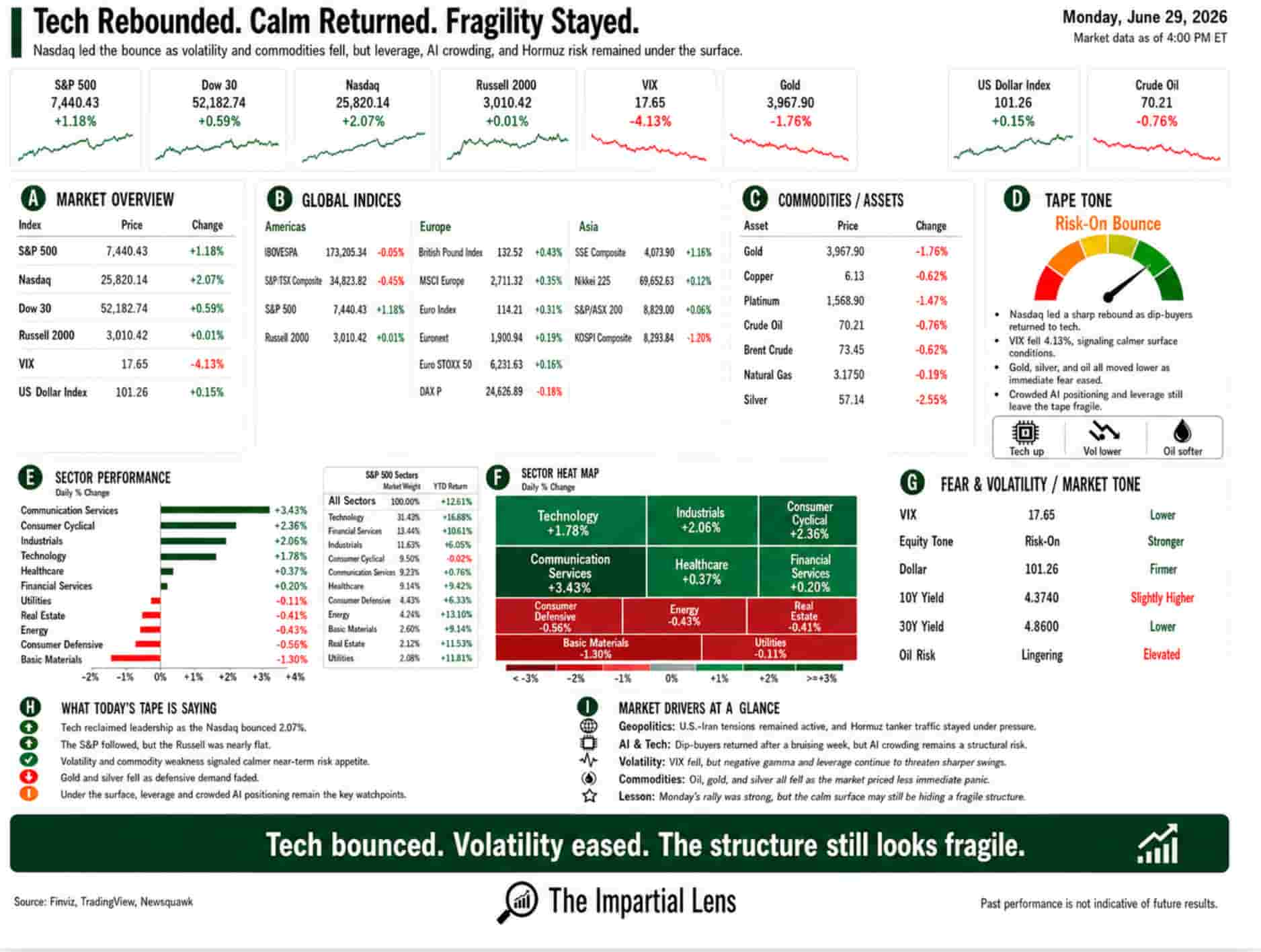

After last week’s pressure, dip-buyers stepped back into the trade that had been wobbling hardest. The Nasdaq jumped 2.07%. The S&P 500 rose 1.18%. The Dow gained 0.59%. The Russell 2000 barely moved, up 0.01%.

Volatility cooled too, with the VIX down 4.13%.

On the surface, that looked like a clean risk-on day.

But beneath the surface, the picture was not quite that simple.

Oil fell. Gold fell. Silver was hit hard. Energy lagged. Defensive sectors were weak. And the geopolitical story that supposedly calmed markets last week became messy again over the weekend.

So yes, the bounce came back.

But so did the risks.

Tech Reclaimed The Tape

The main story was technology.

After a bruising week for AI, semiconductors, hyperscalers, and mega-cap tech, buyers returned. Technology rose 1.78%. Communication services jumped 3.43%. Consumer cyclical gained 2.36%. Industrials rose 2.06%.

That is a strong leadership mix.

It tells us investors were not running away from risk on Monday. They were rotating back into the growth trade.

But the important question is why.

Was this renewed conviction?

Or just positioning repair after one of the sharpest tech selloffs in years?

That distinction matters.

Last week’s headlines were not small. Hedge funds reportedly sold tech aggressively. The AI trade started to fracture. OpenAI’s IPO delay raised questions about private-market timing. Memory, chips, data centers, power, and hyperscaler capex all came under scrutiny.

Then Monday arrived, and investors bought the dip.

That does not erase the questions.

It just proves the trade still has muscle.

AI Is Still The Center Of Gravity

The market is still orbiting around AI.

That is the good news and the bad news.

The good news is obvious: AI remains the most powerful growth story in the market. It touches semiconductors, software, data centers, energy, robotics, defense, cloud, and infrastructure. When the AI trade catches a bid, the indexes can move quickly.

The bad news is also obvious: too much depends on it.

The headlines keep pointing to the same pressure points. Inference costs are falling. Investors are questioning whether hyperscalers need to keep spending at the same pace. The BIS has warned that disappointment in AI returns could tighten financing conditions. Data-center opposition is growing locally. Power demand is becoming political. And the old “buy anything AI” trade is starting to split into winners, losers, and companies simply wearing the costume.

That is why Monday’s rally needs to be handled carefully.

AI bounced.

But AI is still on trial.

Oil Fell Despite Fresh Iran Stress

The strangest part of Monday was oil.

Over the weekend, the U.S. and Iran reportedly exchanged strikes again. Hormuz tanker traffic plunged as ship owners and operators pulled back. Iran contradicted Trump’s claim that talks were set to resume immediately. The diplomatic picture became less clear, not more clear.

And yet crude fell.

Crude oil dropped 0.76%. Brent fell 0.62%.

That tells us the market is not pricing maximum energy panic right now. It may be assuming that the weekend flare-up remains contained. It may also be looking at vessels leaving the Gulf, weak demand signals, or the idea that the worst-case Hormuz shock is still unlikely.

But this is not a clean oil signal.

If tanker traffic is falling and political rhetoric is worsening, lower crude does not necessarily mean risk is gone. It may mean the market is discounting the risk again.

That can work until it doesn’t.

The Strait of Hormuz remains a pressure point because it connects geopolitics directly to inflation, shipping, insurance, and central-bank expectations.

The market can ignore that for a day.

It cannot ignore it forever.

Gold And Silver Took The Hit

Gold fell 1.76%. Silver dropped 2.55%.

That was notable.

If investors were genuinely worried about a fresh Middle East escalation, gold should have been stronger. Instead, bullion was sold while tech rallied.

That suggests Monday was less about fear and more about rotation back toward risk.

But again, the message is not perfectly clean.

Gold has been pulled between several forces: geopolitical risk, the dollar, rate expectations, central-bank demand, and investor positioning. When gold falls on a day when Iran headlines are messy, it tells us investors are not treating geopolitics as the only driver.

The Fed still matters.

The dollar still matters.

Real yields still matter.

And positioning still matters.

The Calm Surface May Be Misleading

This is where the market gets interesting.

The headline tape looked calm. Stocks rose. VIX fell. Tech bounced. Oil declined.

But several warnings remain underneath.

Gamma risk has been flagged. Leverage has been rising. Retail sentiment has been strong. The AI trade remains crowded. Correlations are shifting. Old leadership has been unwound. And the market has become more sensitive to liquidity shocks.

That does not mean a selloff is guaranteed.

It means the market is more fragile than the index level suggests.

A quiet tape can hide a lot of pressure.

That was Monday’s lesson.

The market rallied, but the rally came with a warning label.

The Real Read

Monday was a bounce.

A real one.

Tech reclaimed leadership. Communication services surged. Consumer cyclical and industrials joined in. Volatility cooled. The Nasdaq led.

That is constructive.

But it was not a clean all-clear.

Oil fell despite renewed U.S.-Iran tension. Gold and silver sold off. Energy lagged. The AI trade bounced after a difficult week, but the deeper questions about capex, leverage, hyperscalers, power demand, and return on investment did not disappear.

This market is still asking the same question:

Is AI the next durable productivity cycle?

Or has it become the world’s most crowded trade?

The answer may be both.

And that is what makes it dangerous.

The market can rally hard when AI works. But if too much money, too much leverage, and too much faith are tied to the same story, then even small disappointments can move through the system quickly.

Monday proved that buyers are still there.

It did not prove that the risks are gone.

The bounce came back.

Tech reclaimed the tape.

Volatility cooled.

But under the calm surface, the market is still carrying the same problem:

Too much depends on AI staying perfect.