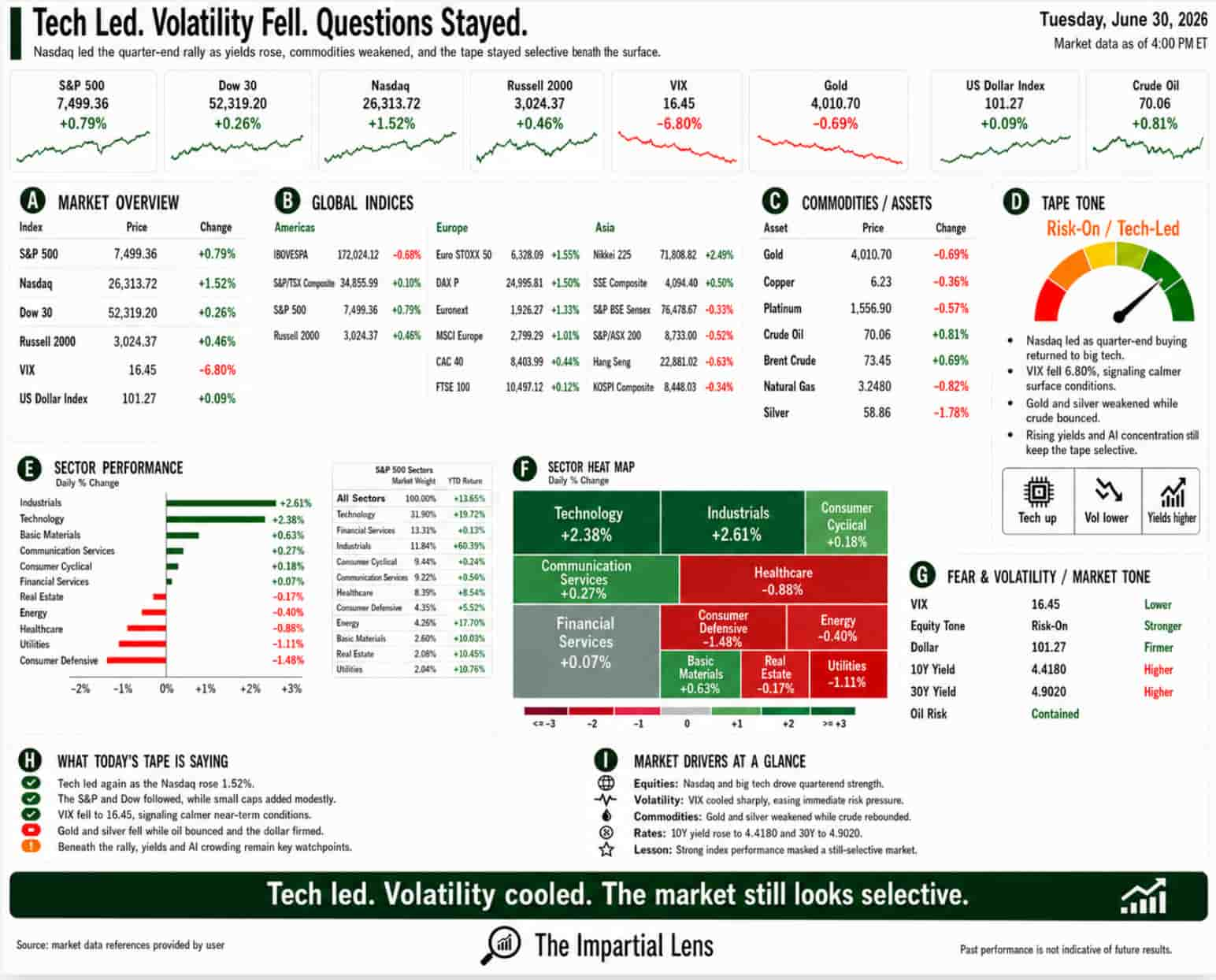

Tuesday gave the market what it wanted.

Leadership.

After several days of messy rotation, AI worries, oil volatility, Bitcoin weakness, and fragile sentiment, the tape finally found a cleaner driver again: technology.

The Nasdaq rose 1.52%. The S&P 500 gained 0.79%. The Dow added 0.26%. The Russell 2000 climbed 0.46%.

Volatility cooled sharply, with the VIX down 6.80%.

That is the kind of move bulls wanted to see.

But it was not a perfect risk-on day.

Bitcoin fell 2.05%. Gold dropped 0.69%. Silver lost 1.78%. Defensive sectors lagged. Healthcare was weak. Consumer defensive names were hit. Energy slipped even as crude bounced.

So the market looked stronger.

But not simple.

Tech Took The Wheel Again

The key message came from the sector tape.

Technology rose 2.38%. Industrials gained 2.61%. Communication services added 0.27%. Consumer cyclical names were slightly higher. Financials were barely positive.

That tells us buyers came back to the parts of the market that matter most for index direction.

This is important because last week’s question was whether the AI trade had started to fracture.

On Tuesday, the market answered with a bounce.

But a bounce is not the same thing as a full repair.

The AI story still has plenty of pressure around it. OpenAI’s IPO timing remains a source of debate. Hyperscaler capex is being questioned. Data-center resistance is growing. Power demand is becoming political. Some executives are starting to rethink the costs of replacing humans with AI tools. And analysts are still asking whether AI is actually boosting margins outside the technology sector.

That is the tension.

The market keeps coming back to AI because it is still one of the few visible earnings-growth stories.

But the story is becoming more complicated.

The Quarter Was Strong. The Path Was Not.

The headline numbers for the quarter looked impressive.

The S&P 500 and Nasdaq reportedly posted their biggest quarterly gains in years. Stocks finished the month, the quarter, and the first half higher.

That sounds clean.

It was not.

The path included war risk, Warsh’s hawkish Fed message, AI valuation concerns, leveraged ETF stress, negative gamma warnings, Bitcoin weakness, gold volatility, oil shocks, Hormuz headlines, and repeated questions about whether the market’s most important trade had become too crowded.

That is why the quarter-end rally deserves respect, but not blind trust.

Markets can go up while the structure underneath gets more fragile.

That is the uncomfortable part.

A strong index can hide a lot of stress if the gains are concentrated, leveraged, or dependent on one dominant story.

Right now, that story is still AI.

Oil Bounced, But Hormuz Stayed Messy

Crude rose 0.81%, while Brent gained 0.69%.

That matters because oil had been under pressure as markets priced a calmer Middle East setup. But the headlines remain messy. U.S. envoys traveled to Qatar. Iran disputed the idea of direct talks. Oman’s role in Hormuz fees and transit language remained unclear. Israel warned that conflict with Iran could resume quickly. And market attention stayed fixed on whether the Iran memorandum actually reduces risk or merely delays the next flare-up.

The market wants to believe energy transit is normalizing.

But the details are still not clean.

This is why oil remains important.

If crude stays contained, it helps inflation expectations and gives equities breathing room. If Hormuz risk comes back, the inflation story can change quickly.

The market has been treating oil relief as a gift.

It may not be permanent.

Bitcoin And Gold Did Not Confirm The Party

The strange part of Tuesday was that Bitcoin and gold both weakened.

Gold fell. Silver fell harder. Bitcoin dropped more than 2%.

That is not what you would expect from a perfectly clean risk-on day.

It suggests the market was not simply buying everything speculative. It was buying a specific kind of risk: technology, AI, growth, and selected equity leadership.

Bitcoin weakness also came with headlines about crypto regulation, shadow-banking concerns, and position stress. Gold weakness reflected the continuing pull between the dollar, rates, Fed credibility, and reduced immediate geopolitical fear.

So the message was not “everything is fine.”

The message was more specific:

Tech was back in charge.

Other assets were less convinced.

The Fed Is Still In The Room

The Fed did not disappear just because tech rallied.

The labor market data was mixed. Job openings beat expectations, but hiring remained soft. Consumer confidence missed. The Fed remains worried about inflation. Some Fed commentary still leaned hawkish. Warsh’s credibility-first approach remains the backdrop.

That matters because the market is trying to price two things at once.

It wants AI-led earnings strength.

And it wants enough macro weakness to keep rate relief alive.

That is not an easy balance.

If the economy is too strong, the Fed stays tight.

If the economy is too weak, earnings get questioned.

If AI spending stays hot, inflation and power costs may stay sticky.

If AI spending slows, the market’s favorite growth story gets tested.

That is the narrow path.

Tuesday’s rally helped.

It did not widen the path.

The Real Read

Tuesday was a good day for the bulls.

Tech led. The Nasdaq bounced. The S&P followed. Industrials joined. Volatility fell. The quarter closed with strength.

That matters.

But it was not a broad all-clear.

Bitcoin fell. Gold fell. Silver sold off. Healthcare and consumer defensive sectors lagged. Energy slipped at the sector level even as oil bounced. The market remains heavily dependent on AI leadership, and the questions around that leadership are getting sharper.

Can AI keep driving earnings?

Can hyperscalers keep spending without pressure?

Can power grids and data centers keep up?

Can companies outside tech actually see margin benefits?

Can the market absorb more leverage without becoming unstable?

Can the Fed stay credible without choking the rally?

Can Hormuz stay quiet long enough for oil relief to matter?

That is the real story.

The rally found its leader again.

But the leader is still carrying a lot of weight.

Tech took the wheel.

Volatility cooled.

The quarter ended strongly.

But under the surface, this market still depends on one big assumption:

AI has to keep working.