Wednesday wasn’t just another bad day for stocks.

It was a stark reminder that markets don’t live in clean spreadsheets. They live in the real world — where inflation, oil shocks, geopolitics, debt, and technology collide all at once.

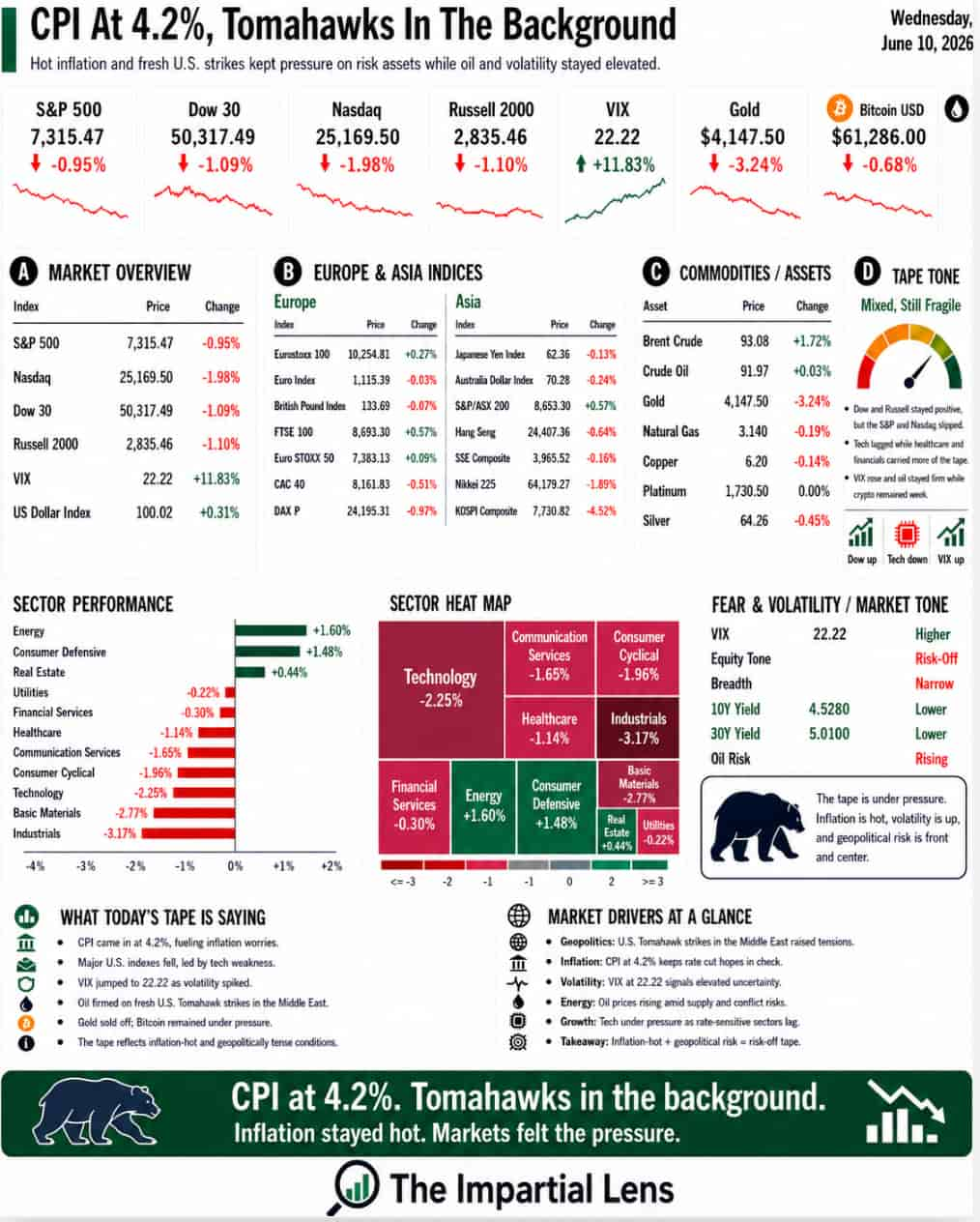

The headline CPI hit 4.2% — the highest in three years. That alone stung. But the market also had to absorb fresh U.S. strikes on Iran, Trump warning that the U.S. would “bomb the sh*t out of them” again if no deal is reached, Iranian retaliation claims, and renewed pressure on the Strait of Hormuz.

This wasn’t just about inflation.

It was politics turning macro again.

The tape delivered the verdict:

- S&P 500 –0.95%

- Dow –1.09%

- Nasdaq –1.98%

- VIX +11.83% to 22.22

Source: Yahoo Finance

Not panic. But a clear signal: something fundamental has shifted.

Inflation Is Not Dead

The market desperately wanted a clean victory over inflation. It didn’t get one.

A 4.2% CPI print is not “mission accomplished.” It’s inflation still very much alive — sitting comfortably in the corner, refusing to leave.

The real problem isn’t just the number. It’s the company it keeps: rising oil, elevated war risk, surging government borrowing, exploding AI power demand, and sticky costs for food, energy, insurance, and services.

This is not the backdrop for easy money or a quick Fed rescue. It’s the backdrop for a central bank that must remain cautious while markets beg for relief.

Wednesday pushed back hard on the narrative that inflation was yesterday’s problem.

Oil Is Politics with a Price Tag

Oil made the connection explicit.

Crude rose 2.13% to $90.08. Brent climbed to $93.02.

Oil isn’t just a commodity — it’s transport, food, shipping, manufacturing, and inflation expectations all rolled into one. And right now, it’s being priced through geopolitics.

U.S. strikes, Iranian responses, threats of escalation, and Hormuz tension mean the oil market is no longer ignoring the Tomahawks in the background. Once politics drives oil prices, it flows straight into inflation, the Fed, and valuations.

That chain tightened on Wednesday.

This Is Not a Clean Ceasefire Story

Markets keep hoping for a neat resolution in the Middle East: quick deal, calm shipping, contained oil risk.

What we’re getting instead is messy “peacefire” — diplomacy and military action happening simultaneously. Strikes followed by talk of restraint, then more pressure. Uncertainty that refuses to be modeled cleanly.

Markets hate that kind of fog. So they add a risk premium. Geopolitics is no longer a side story — it’s now embedded in market structure.

Tech Cracked Where It Was Supposed to Be Strong

The Nasdaq fell nearly 2%, with tech down 2.25%. That matters because tech — and especially AI — has been the market’s emotional engine.

Oracle disappointed. AI capex is running hot. Financing questions are surfacing. Power constraints are real. The easy narrative (“just build it and profits will come”) is meeting reality.

Source: Yahoo Finance

The market is finally asking the right questions:

Who pays for the chips, the electricity, the cooling, the debt, and the grid upgrades?

And who actually earns the return?

AI is real. But real things have costs — and those costs matter more when CPI is 4.2% and yields remain elevated.

This Wasn’t Healthy Rotation — It Was Risk Reduction

Some called it rotation. It looked more like selective selling of the parts of the market that need everything to go right.

Industrials (–3.15%), tech (–2.25%), consumer cyclicals (–1.96%) took the brunt.

Winners? Energy (+1.60%) and consumer defensives (+1.43%).

That’s not growth leadership. That’s a defensive shift — reaching for oil exposure and staples while trimming the expensive bets.

Not exactly a roaring endorsement of risk appetite. More like a polite cough before leaving the room.

Gold and Bitcoin Didn’t Save the Day

In theory, gold should thrive on inflation and war risk. Instead, it fell 2.43%. Bitcoin slipped too.

Source: Yahoo Finance

When both traditional and “digital” hedges weaken amid rising CPI and geopolitics, it signals broad risk reduction, not calm rotation. Investors weren’t hedging — they were liquidating what they could.

The Bond Market Still Runs the Show

The 10-year yield sat near 4.54%, with the 30-year around 5.03%. In a world of expensive long-duration assets, those levels matter.

When the 30-year is around 5%, money is not free. When CPI is 4.2%, the Fed is not free. When oil is rising, inflation expectations are not free. And when the government is issuing debt at record pace, the bond market does not get to quietly disappear.

This is the part equity investors keep trying to skip.

Stocks can argue. Tech can dream. Politicians can shout.

But the bond market decides what future earnings are worth.

And right now, the bond market is not handing out unlimited permission slips.

The Real Read

Wednesday was a political-macro collision.

The market wanted inflation relief → got 4.2% CPI.

Wanted calm geopolitics → got strikes and Hormuz tension.

Wanted AI leadership → got capex reality checks.

Wanted hedges → got liquidation.

Inflation isn’t dead. Oil isn’t quiet. AI isn’t free. Geopolitics isn’t contained. And politics is now part of the pricing mechanism.

The market didn’t just reject the CPI number.

It rejected the fantasy that one clean data point could fix a world this messy.

Reality showed up with 4.2% CPI, higher oil, weaker tech, and Tomahawks in the background.