Stocks pushed higher again, but the calm is getting harder to trust. AI is still doing the heavy lifting, geopolitics is still driving the tape, and the market is acting as if every bad headline will be fixed before it matters.

Monday gave us another strange market day.

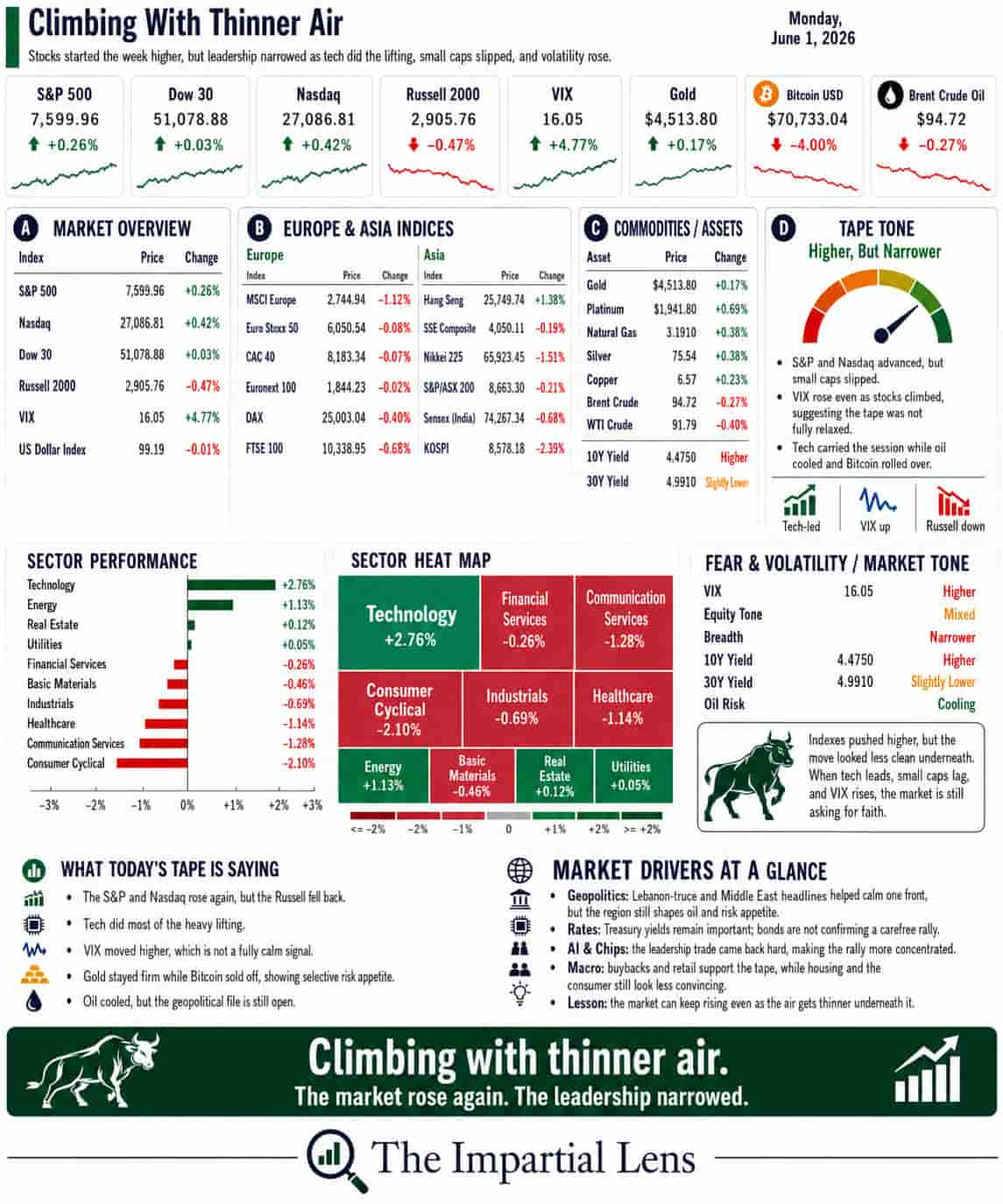

The major indices finished mostly higher. The S&P extended its winning streak. Tech remained strong. AI enthusiasm stayed alive. Retail flows kept chasing upside. Buybacks continued to support the tape.

On the surface, that looks constructive.

But underneath, the story was much less comfortable.

Bonds were hit. Gold was hit. Bitcoin was hit. Oil headlines swung with every update from the Middle East. And the market kept responding to geopolitics as if every crisis is now just another tradable headline.

That is the key point.

The market is not calm because the world is calm.

The market is calm because investors believe the next rescue headline is always coming.

The Dashboard Says: Strength, But Concentrated

The headline tape still favors the bulls.

Tech strength helped carry the market. Nvidia kept the AI story alive. Microsoft and Nvidia announced new AI-PC related developments. IBM rallied. Software quietly matched semis over the recent stretch. Retail investors remained relentless. Corporate buybacks are still active.

That is real support.

But it is also increasingly concentrated support.

Goldman’s desk noted a market that is “more convinced, more concentrated, and more levered in AI.” That matters. Concentration can make an index look healthy while the actual market underneath becomes more fragile.

The lesson is simple:

A strong index does not always mean a strong market.

Sometimes it means a few powerful trades are carrying the whole structure.

That is what we need to keep watching.

Geopolitics Is Now Part of the Daily Tape

The biggest driver was not just earnings or economic data.

It was geopolitics.

Trump reportedly pressured Netanyahu to accept a Lebanon truce. Hezbollah and Israel ceasefire headlines moved risk sentiment. Iran threatened to block the Bab al-Mandab Strait and reportedly paused messaging with the U.S. before later headlines turned more positive. Russia banned jet fuel exports after Ukrainian attacks damaged refining capacity. French commandos seized another Russian shadow-fleet vessel. Taiwan remained in the background. China chip restrictions tightened again.

This is not background noise.

This is the market’s operating environment.

Geopolitics now affects oil, shipping, defense spending, sanctions, chip access, supply chains, inflation expectations, and bond markets.

That is why we keep bringing it into the commentary.

War headlines are not separate from markets.

They move through markets.

Oil responds first.

Inflation expectations respond next.

Bonds respond after that.

Then equities get repriced.

The market keeps trying to skip that chain and go straight back to AI.

That may work for a while.

But it is not a stable framework.

Oil Still Matters, Even When It Does Not Rally

One strange feature of this tape is that oil has not surged the way many expected, even with Hormuz and Bab al-Mandab risk still alive.

Goldman asked the right question: why does oil refuse to rise despite continued shipping disruption?

The answer seems to be demand.

The market is not only watching supply risk. It is also watching weakening demand, consumer stress, and the possibility that high prices are already doing damage.

That is important.

Oil can fall for good reasons.

But it can also fall for bad reasons.

If oil falls because a peace deal is credible, that is helpful.

If oil falls because demand is weakening, consumers are exhausted, and global trade is slowing, that is a different story.

Same price move.

Different message.

Bonds Are Still the Referee

The bond market remains the part of the story that investors would rather not talk about.

Monday reminded us why that is dangerous.

Bonds were battered as stocks pushed higher. The Fed remains under political pressure. Powell warned that Fed credibility matters. Manufacturing data looked mixed: activity improved, but producer costs jumped. That is the kind of combination central banks dislike.

Growth is fine.

Inflation pressure is not.

The bond lesson stays simple:

If yields rise because growth is improving, markets can handle that.

If yields rise because inflation pressure is returning, markets have a problem.

That distinction matters.

Higher real yields make safer assets more competitive. They raise the cost of capital. They pressure housing, private credit, AI capex, government borrowing, and long-duration equities.

The AI trade can keep running.

But it does not get a free pass from the bond market forever.

AI Is Still the Engine — And the Risk

AI remains the center of the market.

Nvidia is still leading the psychology. Hyperscalers are still spending. AI-PC headlines are back. Anthropic is moving toward an IPO. SpaceX is expanding AI compute partnerships. The market still wants more AI, more leverage, more upside, and fewer hedges.

But the AI story is also becoming more complicated.

There are now questions about capex, power demand, memory shortages, token costs, infrastructure funding, and whether AI spending produces enough real economic return.

This is no longer just a software story.

It is a financing story.

An energy story.

A labor story.

A national-security story.

A political story.

That is why the AI trade is both powerful and fragile.

The market is treating it as the solution.

But it may also be creating the next problem.

The Real Read

Monday was constructive at the index level.

Stocks rose.

Tech led.

Retail kept buying.

Buybacks helped.

AI remained the dominant theme.

But the market underneath is not as calm as the index suggests.

Bonds were weak.

Gold was weak.

Bitcoin was weak.

Oil headlines remain unstable.

Geopolitics is still driving intraday direction.

AI concentration is getting more extreme.

Consumer stress remains visible.

And the Fed is still trapped between inflation pressure and political pressure.

The market is not pricing certainty.

It is pricing the belief that every problem can be managed.

That the Middle East can be contained.

That oil can stay under control.

That AI can keep lifting earnings.

That bonds will not revolt.

That consumers will keep spending.

That political dysfunction will remain a headline, not a market event.

That is a lot to ask.

The lesson is clear:

Calm index action can hide a much noisier market underneath.

For now, the rally still works.

But the more it depends on AI, headline relief, and investors refusing to buy protection, the more fragile it becomes.

The market may still be climbing.

But it is climbing with thinner air.