Tuesday was not about oil.

That is the first thing to understand.

Oil fell again. The Iran story stayed alive. Hormuz remained part of the global discussion. Bonds caught a bid. Some defensive sectors held up.

And none of that saved the market.

The real story was tech.

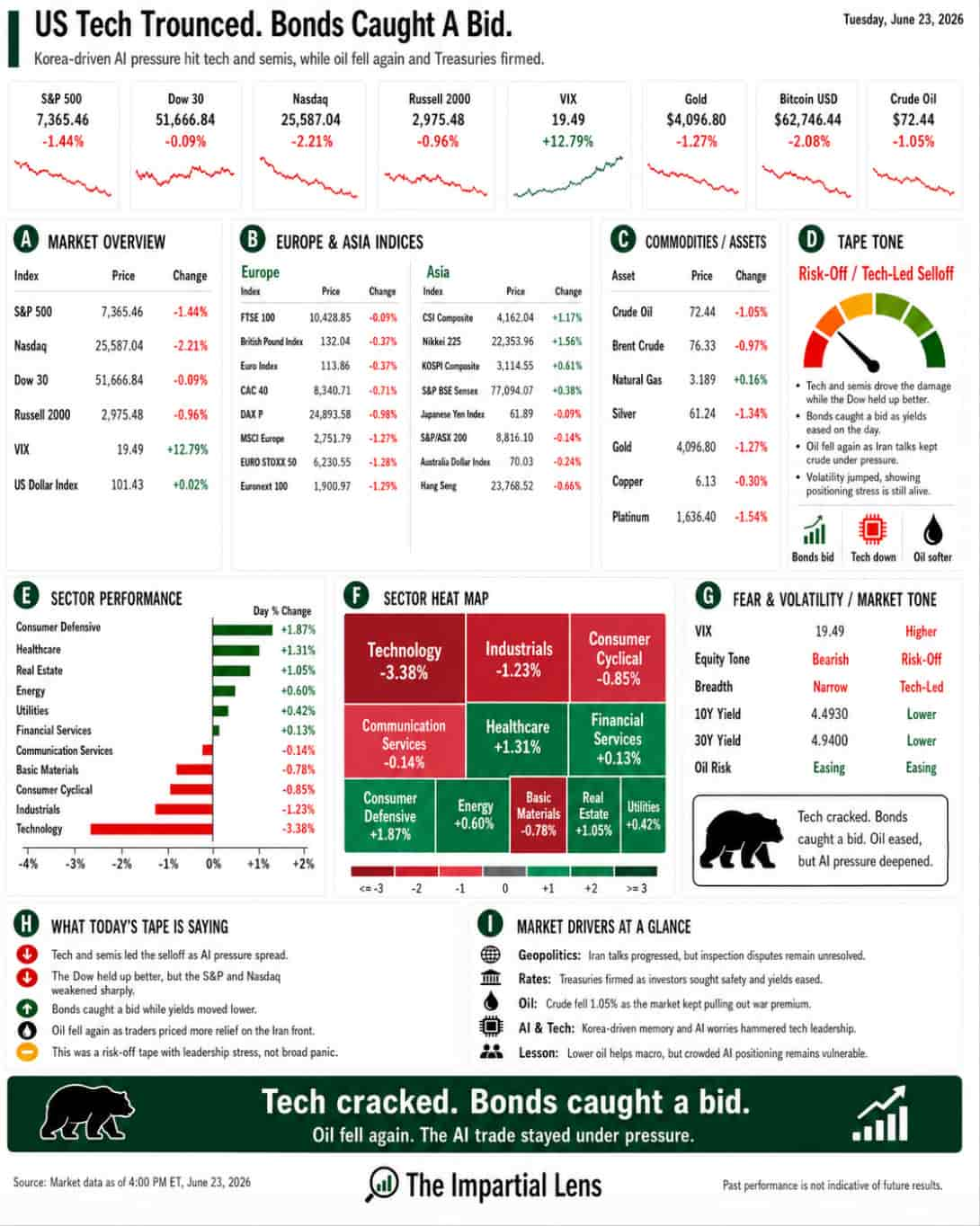

The Nasdaq dropped 2.21%. The S&P 500 fell 1.44%. The Russell 2000 lost 0.96%. The Dow slipped just 0.09%, which tells you this was not a traditional broad market collapse.

It was more targeted than that.

The VIX jumped 12.79% to 19.49. Crude fell 1.05% to $72.44. Gold dropped 1.27% to $4,096.80. Bitcoin fell 2.08% to $62,746.

So the market gave us a clear message:

Oil relief is no longer enough.

When tech cracks, the whole tape changes.

Tech Was The Problem

The pressure came from the same part of the market that has carried the rally.

AI. Semiconductors. Memory. Data centers. Mega-cap tech. The whole machinery of the “future growth” trade.

The headline flow was brutal.

Korea’s AI-linked market suffered a sharp selloff. Memory stocks came under pressure. Semiconductor and memory ETFs were hit. Concerns grew that recent AI upside was being amplified by leverage, retail flows, product structure, and crowded positioning — not just fundamentals.

That matters.

Because the AI trade has become the market’s psychological center of gravity.

When AI is working, investors forgive almost everything: valuation, rates, capex, energy demand, depreciation risk, and crowding.

When AI starts wobbling, all those questions come back at once.

That is what happened Tuesday.

The market did not suddenly decide AI is fake.

It started questioning the price being paid for it.

That is a very different thing.

Korea Was The Warning Shot

The Korean selloff mattered because it pointed to something bigger than one market.

It showed how fragile leverage can become when everyone crowds into the same theme.

The AI trade has not just been a U.S. story. It has been global. Korea, Taiwan, Japan, U.S. semis, memory suppliers, power infrastructure, cloud providers, data-center builders — all of it has been tied together by one belief:

AI demand will keep accelerating.

That belief may still be right.

But markets do not move only on whether the story is right. They move on whether expectations are too high.

And expectations in AI are no longer modest.

They are stretched.

When a trade becomes this crowded, even a small disappointment can become a large move. That is why a Korean memory-stock shock can echo through U.S. tech, semis, ETFs, and volatility.

The butterfly flapped its wings in Korea.

The Nasdaq felt it in New York.

Oil Relief Took A Back Seat

This is the uncomfortable part for the market.

Oil did what bulls wanted.

Crude fell. Brent fell. Natural gas was slightly higher, but the broader energy panic kept cooling. The Iran talks remained active. Washington and Tehran continued arguing over inspections, frozen assets, and the terms of the deal, but the market still treated the worst Hormuz outcome as less likely than it was a week ago.

That should have supported risk.

But it did not support tech.

That is the lesson.

Lower oil can ease inflation pressure.

Lower oil can help consumers.

Lower oil can help airlines.

Lower oil can reduce one geopolitical risk premium.

Lower oil can give the Fed a little more breathing room.

But lower oil cannot fix an overcrowded AI trade.

It cannot fix leverage.

It cannot fix valuation.

It cannot fix forced selling.

It cannot fix a market where too many investors own the same story.

The market got oil relief.

Tech sold off anyway.

Bonds Were Saying Something Different

The bond market was more calm than the equity tape.

Treasury yields eased across parts of the curve. The 5-year yield fell. The 10-year yield moved lower. The 30-year yield was also softer. That suggests investors were not simply pricing a hotter economy or a fresh inflation scare.

They were looking for safety.

That matters because it shows the selloff was not just about rates rising and crushing growth stocks.

It was about risk being reduced inside the most crowded part of the market.

The Fed still matters, of course. Kevin Warsh’s credibility-first approach has changed the backdrop. Investors cannot assume easy forward guidance or a quick rescue if markets wobble.

But Tuesday’s action looked less like “rates are killing tech,” and more like “tech positioning is finally being questioned.”

That is a different kind of risk.

The Sector Tape Told The Story

The sector map was ugly where it mattered most.

Technology fell 3.38%. Industrials dropped 1.23%. Consumer cyclical names were weak. Communication services slipped.

But not everything broke.

Healthcare was positive. Financials were slightly green. Consumer defensive, energy, utilities, and real estate showed pockets of strength.

That confirms the message:

This was not a full liquidation.

It was a rotation away from the market’s favorite trade.

When investors sell everything, it is panic.

When they sell one leadership group and hide elsewhere, it is a warning.

Tuesday looked like a warning.

The Real Read

The market’s biggest risk may have shifted.

For weeks, the story was Hormuz. Oil. Iran. Inflation. War risk. Shipping risk. Energy security.

That risk is still there. The Iran deal is not clean. Tehran disputes key U.S. claims. Hormuz tolls and ship passage issues remain unsettled. There are still reports of covert cyber disruption inside Iran’s banking system. The region is calmer than it was, but it is not solved.

Still, Tuesday’s tape said the market is now focused somewhere else.

AI is the risk.

Not because AI is unimportant.

Because it has become too important.

Too much market leadership depends on it.

Too much capex depends on it.

Too much semiconductor demand depends on it.

Too much retail enthusiasm depends on it.

Too much valuation support depends on it.

Too much “soft landing” optimism depends on it.

That is why Tuesday mattered.

Oil went down.

Bonds caught a bid.

But tech still cracked.

The market’s old fear was that Hormuz would break the rally.

Tuesday’s lesson was different.

The bigger danger may be that AI became the rally.