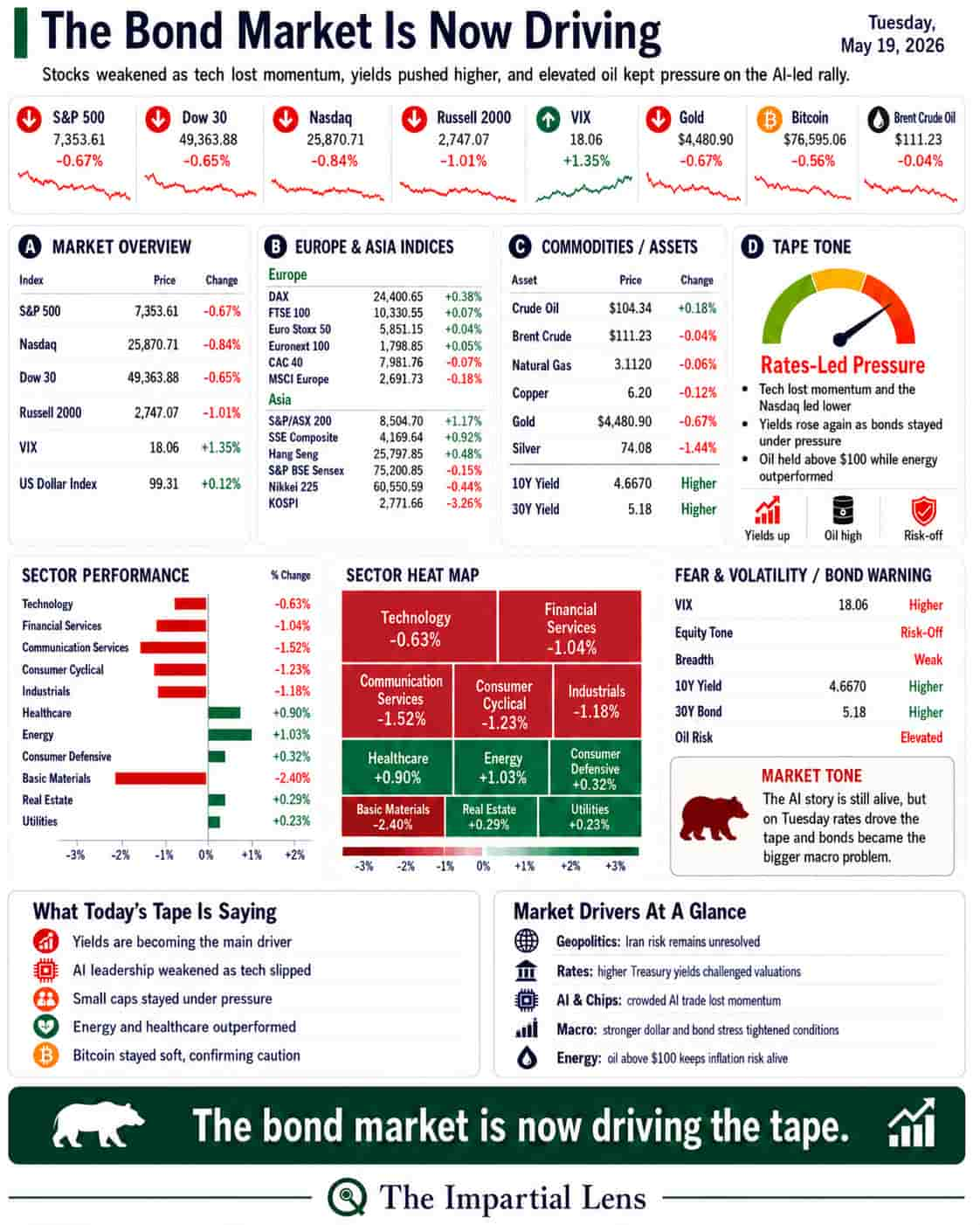

Stocks weakened again as tech lost momentum, yields pushed higher, oil stayed elevated, and the AI melt-up faced a harder macro test.

Monday’s message was simple:

The bounce was not the repair.

Tuesday confirmed it.

The market did not collapse, but the pressure continued to spread. The S&P 500 fell about 0.67%, the Dow dropped roughly 0.65%, the Nasdaq lost about 0.84%, and the Russell 2000 fell just over 1%.

The VIX rose 1.35%, the U.S. Dollar Index gained 0.12%, and bond yields moved higher again, with the 10-year around 4.67% and the 30-year near 5.18%.

That is the important part.

This is no longer just an AI story.

It is now a rates story.

For weeks, the market has been treating AI as the answer to every question. Weak breadth? AI. Higher oil? AI. Geopolitical risk? AI. Expensive valuations? AI.

But Tuesday’s tape suggested the narrative is shifting.

The headline stack captured it clearly: “Supply, Supply, Supply,” “The Bond Market Is Becoming Stocks’ Biggest Problem Again,” “The Bond Market Is Starting To Break The AI Melt-Up,” and “Inflation Is Coming For The Overcrowded AI Trade.”

That is the new market battle.

AI still matters.

But bonds are now driving.

The Dashboard Says: Pressure Is Spreading

Tuesday’s tape was broadly soft.

The Nasdaq fell 0.84%, which matters because technology and AI have been the market’s main leadership group. The Russell 2000 fell 1.01%, showing that smaller companies remain vulnerable to higher financing costs and weaker risk appetite.

The sector heat map made the rotation clear.

Technology fell 0.63%.

Financial Services dropped 1.04%.

Communication Services fell 1.52%.

Consumer Cyclical lost 1.23%.

Industrials fell 1.18%.

Basic Materials dropped 2.40%.

The relative winners were defensive or energy-linked.

Energy rose about 1.03%.

Healthcare gained about 0.90%.

That is not a classic growth rally.

That is a market rotating away from the most crowded momentum areas and toward more defensive, inflation-sensitive pockets.

In plain English:

The market is not breaking.

But leadership is changing.

AI Is Still Real — But the Trade Is Crowded

The AI story has not disappeared.

If anything, it is becoming more important to the real economy. The headline stack included more signs of AI replacing labor, token costs becoming a business issue, and AI moving from software dream to metered utility headache.

But the market is starting to separate the story from the trade.

That difference matters.

AI can be real.

AI can transform business.

AI can drive massive capital spending.

And the AI trade can still be overcrowded.

Tuesday’s headlines made that point repeatedly: “The Most Crowded Trade On Earth Is Cracking,” “King Of AI Cracks,” “DeepSeek Blues,” and warnings that semiconductors remain exposed if liquidity tightens.

That is the danger.

When a trade gets too crowded, it does not need bad news to fall.

It only needs buyers to get tired.

Rates Are the 800-Pound Gorilla

The biggest shift is that rates are no longer background noise.

The 10-year Treasury yield moved around 4.67%, while the 30-year sat near 5.18%. That is a tough backdrop for a market still carrying high valuations, crowded AI exposure, and heavy momentum positioning.

Higher rates hit the market in several ways.

They pressure valuations.

They raise discount rates.

They tighten financial conditions.

They make long-duration growth stocks harder to justify.

They increase refinancing pressure.

They reduce the room for speculative excess.

That is why the bond market matters more than any single AI headline.

The market can digest higher rates if growth is strong and inflation is cooling.

But it struggles when yields rise because supply, inflation, oil, deficits, and global bond volatility are all pushing together.

That is the setup now.

Oil Is Still in the Background — But Not Gone

Oil did not explode higher Tuesday, but it stayed elevated.

Crude traded around $104, while Brent sat around $111.

That keeps inflation risk alive.

The market wants to believe the Iran situation can be contained. But the headline stack kept pointing to unresolved stress: Pakistan deploying troops to Saudi Arabia, Iranian shadow-fleet tankers seized, floating Iranian oil stockpiles rising, and talks making little progress.

This is still headline roulette.

The market may get relief headlines.

But the energy market is still pricing risk.

And as long as oil remains elevated, bonds have a reason to stay nervous.

Bitcoin and Crypto Did Not Help

Bitcoin stayed weak, trading around $76,595, down about 0.56%.

That matters because Bitcoin has been one of the cleaner liquidity gauges in this tape.

When Bitcoin rises with tech and falling volatility, investors are embracing risk.

When Bitcoin stays weak while rates rise and tech slips, it tells us speculative appetite is still under pressure.

Crypto did not confirm a recovery.

It confirmed caution.

Today’s Dashboard Translation

Here is what Tuesday’s tape was actually saying:

Rates are now the main story.

The 10-year and 30-year yields remain too high for equity investors to ignore.

AI leadership is wobbling.

Technology fell, Nasdaq lagged, and crowded semiconductor exposure remains a major risk.

Small caps remain vulnerable.

The Russell 2000 fell more than 1%, showing financing pressure beneath the surface.

Energy is still resilient.

Oil remains elevated, and energy was one of the stronger sectors.

Defensives are catching a bid.

Healthcare and energy held up while higher-beta areas weakened.

Crypto remains soft.

Bitcoin weakness suggests speculative liquidity is not fully repaired.

Investor Translation

This is still not a market to panic in.

But it is also not a market to chase blindly.

The market is telling us that the easy AI melt-up phase is being tested by something more powerful: the cost of money.

That means the model portfolio should stay disciplined.

Cash still matters.

Short-duration Treasurys still make sense.

Energy remains relevant.

Power and nuclear infrastructure remain important.

Hedges still matter.

Position sizes should stay modest.

This is not the moment to pretend the AI trade is dead.

But it is also not the moment to pretend it is bulletproof.

The market can still bounce.

But if rates keep rising, oil stays elevated, and tech keeps leaking, every rally becomes harder to trust.

The Impartial Lens View

Tuesday’s market was not a crash.

It was a warning.

The market is shifting from a simple AI-led melt-up to a more complicated environment where rates, oil, and geopolitics are pushing back.

That is the real change.

AI is still powerful.

But the bond market is more powerful.

And right now, the bond market is saying:

The price of money matters again.

That is why Tuesday matters.

The market is no longer asking only:

“Who wins from AI?”

It is now asking:

“Can the AI trade survive higher rates, higher oil, and weaker liquidity?”

That is a much harder question.

The AI story is still alive.

But the bond market is now driving the tape.

And until yields calm down, every bounce deserves skepticism.