Cheap money is ending. Cheap energy is ending. And the market is beginning to price the consequences.

For the last decade and a half, investors were trained to believe in a simple world.

Money would stay cheap.

Energy would stay manageable.

Inflation would eventually calm down.

The Federal Reserve would always arrive with a rescue plan.

And every market problem could be solved with lower rates, more liquidity, and another wave of asset inflation.

That world is starting to crack.

Not all at once. Not in a dramatic, cinematic collapse. But slowly, then suddenly, through the places investors often ignore until it is too late:

Oil.

Inflation.

Long-term interest rates.

Fiscal credibility.

The bond market.

The important signal this week was not just another move in Nvidia. It was not just another AI headline. It was not just another debate over whether the stock market is overbought.

The important signal was this:

The 30-year Treasury yield is back above 5%.

That is not just a number.

That is the market speaking.

And what it is saying is uncomfortable.

The Fed controls the short end. The market controls the long end.

The Federal Reserve can influence short-term interest rates.

It can set the federal funds rate.

It can guide expectations.

It can talk tough or talk soft.

It can inject liquidity or drain it.

But long-term rates are different.

A much larger force shapes the 10-year and 30-year Treasury yields: the global bond market.

That market includes pension funds, foreign governments, banks, insurers, hedge funds, sovereign wealth funds, and individual investors. It is not one person. It is not one committee. It is not one press conference.

It is the collective judgment of capital.

And right now, the long end of the bond market is saying something very different from the soft-landing story.

Source: Yahoo Finance

A 30-year Treasury yield above 5% is a warning that investors want more compensation to lend money to the U.S. government for a generation.

That compensation reflects inflation risk, debt risk, geopolitical risk, and the fear that today’s fiscal promises may be much harder to honor tomorrow.

This is why the bond market matters.

Stocks can tell a story.

AI can tell a story.

Politicians can tell a story.

The Fed can tell a story.

But the long bond asks one simple question:

What is the real price of money for the next 30 years?

Right now, that answer is getting more expensive.

Interest rates are prices, too.

We usually think of prices as the cost of food, gasoline, rent, insurance, or groceries.

But interest rates are also prices.

They are the price of money.

They tell us what it costs to borrow capital today and pay it back tomorrow.

When interest rates are pushed too low for too long, risk does not disappear. It hides.

Cheap money encourages debt.

Cheap money inflates asset prices.

Cheap money rewards leverage.

Cheap money makes weak businesses look stronger than they really are.

Then, when inflation returns and rates rise, the hidden risk comes back into view.

That is where we are now.

The Fed may still influence the short end of the curve, but the bond market is beginning to reprice the long end.

And the long end is where the consequences live.

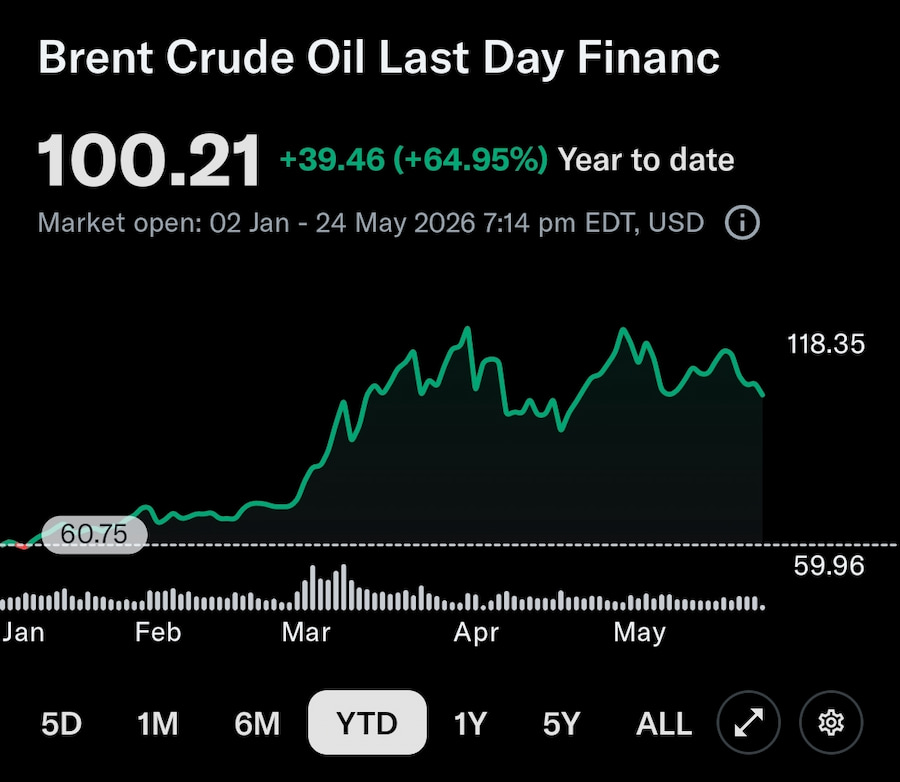

Oil is no longer background noise.

For years, markets treated oil as a temporary input to inflation.

Oil goes up.

Inflation rises.

Oil comes down.

Inflation cools.

The Fed cuts.

Risk assets recover.

That was the playbook.

But this time, the oil story may be more structural.

Source: Yahoo Finance

The war in the Middle East has created a serious disruption in global energy markets. Oil production, shipping routes, and supply chains are all being repriced. This is not just about the daily price of crude. It is about the cost structure of the entire physical economy.

If oil stays higher for longer, inflation becomes harder to kill.

And if inflation becomes harder to kill, the bond market will demand higher yields.

That is the chain investors need to understand:

War → oil disruption → higher energy prices → sticky inflation → higher long-term yields → pressure on stocks, housing, consumers, and debt.

This is not just an energy story.

It is a cost-of-civilization story.

Modern life does not run on software alone. It runs on oil, natural gas, fertilizer, steel, cement, plastics, ships, trucks, refineries, pipelines, and power grids.

AI may be the market’s favorite story.

But the physical economy is still the floor beneath it.

The four ingredients of modern life

Four basic ingredients sit underneath modern civilization:

Ammonia.

Steel.

Cement.

Plastics.

Ammonia is essential for fertilizer.

Steel is essential for infrastructure, machinery, defense, and transportation.

Cement is essential for buildings, roads, bridges, and cities.

Plastics are essential for packaging, medicine, electronics, vehicles, and industrial production.

All four are energy-intensive.

Some require fossil fuels as raw material. Others require enormous amounts of heat. All are tied to oil, natural gas, electricity, shipping, and industrial capacity.

This is where the scarcity theme becomes unavoidable.

If energy prices stay high, the cost of producing the physical ingredients of civilization rises too.

That affects food.

That affects buildings.

That affects infrastructure.

That affects manufacturing.

That affects shipping.

That affects national security.

This part of the market does not fit neatly into the AI narrative.

AI promises abundance.

Energy shocks price scarcity.

And right now, both stories are happening at the same time.

The stock market is still trading the dream.

The equity market is still being pulled upward by powerful narratives.

AI remains real.

Nvidia remains exceptional.

Hyperscaler spending remains enormous.

Data centers are being built at an extraordinary speed.

Capital is still flowing toward the idea that artificial intelligence will reshape productivity, business models, and the global economy.

That may all be true.

But it does not cancel the bond market.

It does not cancel oil.

It does not cancel inflation.

It does not cancel deficits.

It does not cancel the fact that long-term money now costs more.

This is the central tension in markets today:

The stock market is still trading the future.

The bond market is repricing the present.

Investors who only watch the Nasdaq may miss the message.

Investors who only watch Nvidia may miss the message.

Investors who only watch earnings beats may miss the message.

The message is coming from the long bond, and it is simple:

The era of free money is over.

Why a 5% 30-year yield changes everything

A 5% yield on the 30-year Treasury affects almost every asset class.

It pressures housing because mortgage rates remain elevated.

It pressures stocks because future earnings are discounted at a higher rate.

It pressures private equity because leverage is more expensive.

It pressures commercial real estate because refinancing becomes harder.

It pressures the federal government because interest expense rises.

It pressures consumers because credit costs stay high.

It pressures speculative growth because distant future profits are worth less when risk-free yields are higher.

This is why the 30-year yield matters more than most headlines.

A single AI stock can rally.

A single earnings season can look strong.

A single economic report can create optimism.

But if the long end of the bond market keeps moving higher, the foundation under risk assets becomes more fragile.

The Fed may not be coming to save the market.

The market spent much of the past few years waiting for rate cuts.

But that assumption is becoming harder to defend.

Inflation remains above the Fed’s target.

Energy prices are rising again.

Long-term yields are moving higher.

Deficits remain large.

And geopolitical risk is no longer theoretical.

That means investors may need to rethink the old reflex.

The next Fed move may not be a rescue.

It may be a warning.

If oil remains high, inflation stays sticky, and long yields rise, the Fed has less room to ease.

That is very different from the post-2008 playbook.

For years, weak markets created easier policy.

Now, sticky inflation may limit the rescue.

That changes the risk equation.

But this is not only a warning.

This environment is not simply bearish.

It is selective.

Rising energy prices, commodity disruptions, and higher inflation can hurt many parts of the market. But they can also create powerful winners.

In the 1970s, inflation and oil shocks were painful for the broad economy, but they created major opportunities in energy, mining, and hard-asset businesses.

The same may be true again.

If the physical economy is being repriced, investors should look at the companies tied to the physical economy.

Energy producers.

Pipelines.

LNG.

Fertilizer.

Steel.

Cement.

Chemicals.

Mining.

Defense.

Infrastructure.

Commodity logistics.

Businesses with pricing power.

The opportunity is not in chasing every commodity stock blindly.

The opportunity is in recognizing that a world of expensive energy and expensive money rewards different assets than a world of cheap energy and cheap money.

The old winners may not be the only winners.

For most of the last decade, the winning formula was simple:

Own long-duration growth.

Own tech.

Own software.

Own companies that benefit from falling rates and expanding multiples.

That trade may not be dead.

But it is no longer the only trade.

A different group of companies may now matter more:

Companies that produce essential materials.

Companies that own scarce assets.

Companies with low debt.

Companies with pricing power.

Companies that benefit from inflation rather than being crushed by it.

Companies that sell what civilization cannot function without.

This is the shift.

Not from growth to value in the old textbook sense.

But from paper abundance to physical scarcity.

The Impartial Lens view

The market is not sending one clean signal.

It is sending several conflicting signals at once.

AI says growth is alive.

Oil says inflation is not dead.

The Fed says cuts are not guaranteed.

The 30-year Treasury says fiscal trust is weakening.

Commodities say the physical economy is being repriced.

Stocks say liquidity still matters.

That is why this is such a difficult market.

The surface looks strong.

But the underlying message is more complicated.

Investors should not panic.

But they should stop pretending this is the same market as 2021.

It is not.

In 2021, the market was built on cheap money, stimulus, low inflation assumptions, and faith in the Fed.

In 2026, the market is dealing with expensive money, war-driven energy risk, sticky inflation, rising long-term yields, and massive fiscal deficits.

That is a very different backdrop.

The bottom line

The bond market is starting to talk back.

The 30-year Treasury above 5% is not just a yield. It is a message about inflation, debt, oil, war, and trust.

The Fed can still influence the short end.

But the long end is where the market votes.

And right now, that vote says the world is becoming more expensive to finance.

For investors, the lesson is clear:

Do not only follow the stories that are working.

Follow the prices that are warning.

AI may still be real.

Nvidia may still be extraordinary.

Markets may still move higher.

But if oil remains high, inflation stays sticky, and the long bond keeps selling off, the next phase of this market may belong less to the dream economy and more to the physical one.

Energy.

Materials.

Infrastructure.

Defense.

Scarcity.

Pricing power.

That is where the real repricing may be just beginning.