Friday gave the market exactly what it wanted.

Not certainty.

Not clean macro.

Not cheaper AI.

Not a solved oil market.

Not a healthy bond market.

Just enough hope to buy the close.

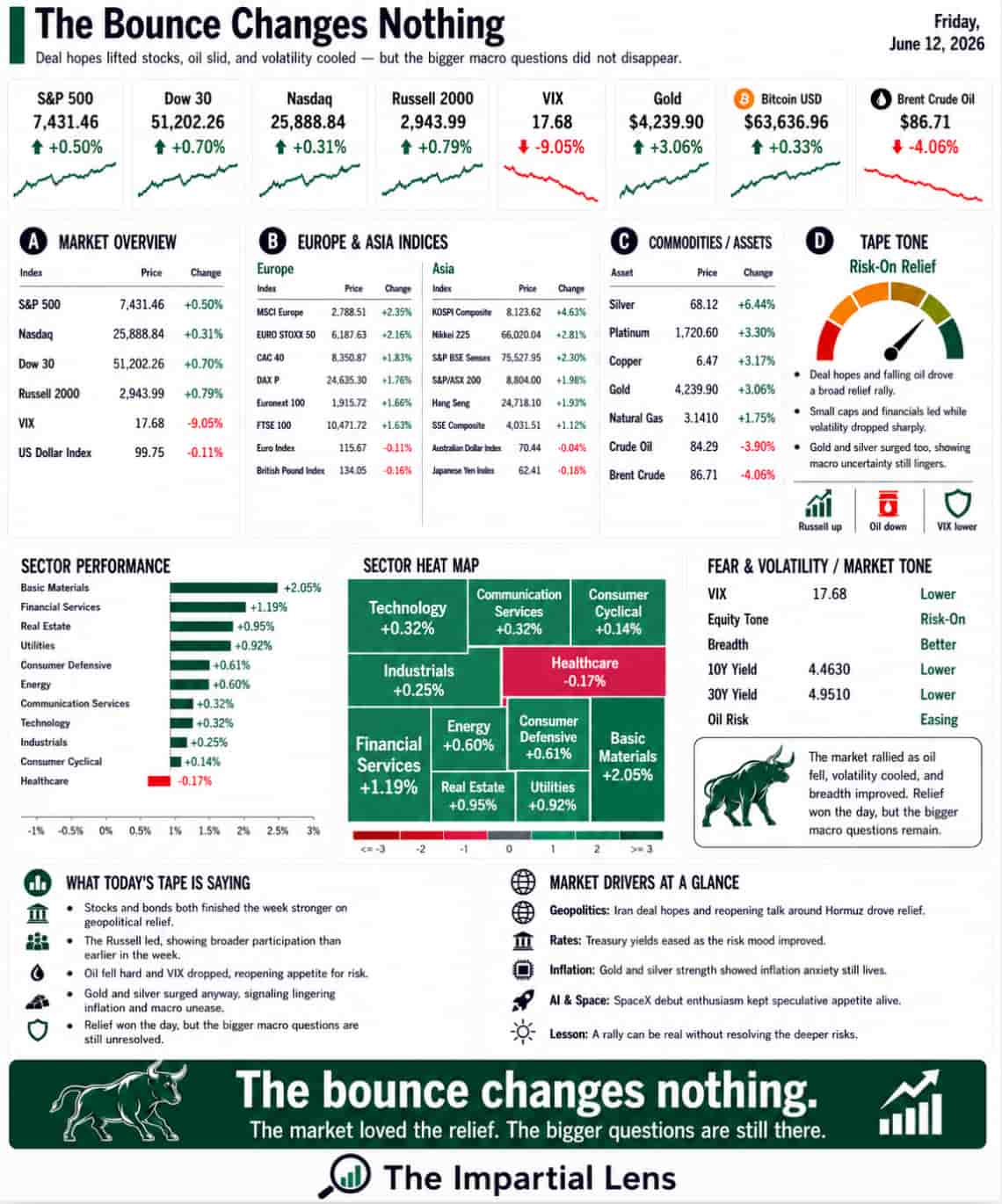

The major indices finished higher. The S&P 500 rose 0.50% to 7,431.46. The Dow gained 0.70% to 51,202.26. The Nasdaq added 0.31% to 25,888.84. The Russell 2000 climbed 0.79% to 2,943.99.

Volatility cooled fast. The VIX fell 9.05% to 17.68.

That is the market saying the panic button got pushed back under the glass.

But the most important move was oil.

Crude oil fell 3.90% to $84.29. Brent dropped 4.06% to $86.71. That was the relief valve. Iran deal hopes, talk of Hormuz reopening, and reports of an agreed text gave investors a reason to believe the worst oil-shock scenario might be avoided.

That was enough for risk assets.

The problem is that “enough for one trading day” is not the same thing as “fixed.”

The Market Bought The Deal Hope

The market did not rally because the world suddenly became calm.

It rallied because the Iran story moved from missiles to memorandum.

Officials claimed a deal could deliver peace, inspections, and the reopening of the Strait of Hormuz. Iran said an agreement was close. Reports suggested a final text had been reached. UAE funds may be unlocked. Oil sanctions could be lifted. The market heard all of that and did what markets do when a tail risk shrinks:

It bought first and asked questions later.

That is why oil fell so hard.

And once oil fell, the rest of the tape breathed easier.

Lower oil means less immediate inflation pressure. Less inflation pressure means central banks have more room. More room means bonds stabilize. Bonds stabilizing permits stocks to move higher.

That is the chain.

But the chain depends on the deal actually holding.

Hormuz is not just a line on a map. It is the pressure valve for global energy. If ships move, markets calm down. If ships stop, inflation returns through the side door.

Friday’s market priced hope.

It did not price proof.

The AI Party Got Its SpaceX Moment

Then came SpaceX.

SpaceX closed 19% higher on its trading debut after pricing the biggest IPO ever at $135 per share. The headlines were enormous. Musk’s wealth reportedly joined the “four commas club.” SpaceX blasted past the kind of valuation that makes normal finance people reach for a chair.

The market loved it.

And of course it did.

SpaceX is the perfect story for this market: frontier technology, national security, space, rockets, satellites, government contracts, private ambition, and the faint smell of inevitability.

That kind of story does not need earnings on day one.

It needs belief.

And belief was in full supply Friday.

But there is another AI-and-tech story underneath the SpaceX celebration, and it is less glamorous.

The AI buildout is starting to look like one of the largest capital-spending cycles in history. Hyperscalers are reportedly using special-purpose vehicles and creative financing structures to keep parts of the commitment away from the headline capex numbers. One estimate put the off-balance-sheet AI commitment around $1.8 trillion.

That is not a rounding error.

That is the invoice hiding behind the magic show.

The AI Supercycle Needs Money

This is where the story gets uncomfortable.

AI may be real. SpaceX may be extraordinary. Compute may become the new oil. But none of this is free.

Data centers need chips, land, water, cooling, grid capacity, power contracts, gas turbines, backup systems, debt markets, equity markets, and political permission.

That is why the AI trade is becoming a volatility story.

The dream is software-like.

The cost curve is industrial.

Markets love the dream. They are only beginning to wrestle with the cost.

Goldman’s compute desk says investors need to focus on the market price of compute. That is another way of saying the bottleneck may not be intelligence. It may be economics.

Token costs can fall. Open-source models can improve. Local inference can spread. But if the infrastructure spend keeps rising faster than monetization, investors will eventually ask the obvious question:

Who earns the return?

That question is not bearish by itself.

It is just not free.

Gold Was Quietly Loud

One of the strongest moves on Friday was gold.

Gold rose 3.06% to $4,239.90. Silver jumped 6.44% to $68.12. Platinum gained 3.30%. Copper rose 3.17%.

That is not nothing.

If the market were fully relaxed, you would not expect precious metals to rip alongside stocks. Gold and silver were saying something different from the equity rally.

Stocks said: deal hope.

Gold said: don’t get too comfortable.

This is the split personality of the tape.

Risk assets rallied because oil fell. Precious metals rallied because the deeper anxiety did not vanish. Inflation risk, currency risk, geopolitical risk, and central-bank credibility are still sitting underneath the surface.

The market wanted to celebrate.

Gold kept one eye on the exit.

The Real Economy Is Still Uneven

There were other warning lights.

Initial jobless claims have moved higher recently. America’s hiring map has become more uneven. Gas prices fell for the third straight week, which helps consumers, but several states still sit above $5 per gallon. A Southeast grid emergency was declared as heat boosted air-conditioning demand. Private credit redemption gates appeared again. Net equity supply turned positive for the first time since the pandemic.

None of those are immediate crash signals.

But they are reminders that liquidity is not unlimited, infrastructure is stressed, and the real economy is not moving in one clean direction.

The market can rally through that.

It just should not pretend it is gone.

The Real Read

Friday was a relief rally.

But relief is not repair.

Stocks rose. Oil fell. Volatility cooled. SpaceX exploded higher. Gold and silver ripped. Bitcoin firmed. The market got a softer geopolitical headline and immediately leaned into risk.

That makes sense.

But it does not settle the bigger debate.

The Iran deal still needs proof.

Hormuz still needs to actually reopen and stay open.

Oil traders may now be shorting crude as if the crisis is over.

AI capex is still huge.

Off-balance-sheet commitments are still growing.

Private credit is still showing stress.

Equity supply is coming back.

And the market remains dangerously sensitive to headlines.

That is the real story.

The bounce changes nothing.

It tells us investors still want to buy relief.

It does not tell us the world is fixed.

The market ended the week with hope in one hand and a very large bill in the other.

Oil said the war risk cooled.

Gold said the fear did not disappear.

SpaceX said speculation is alive.

AI said the invoice is getting bigger.

And the market, for one more day, decided that was good enough.

The Lens:

This was a bounce.

Not a verdict.