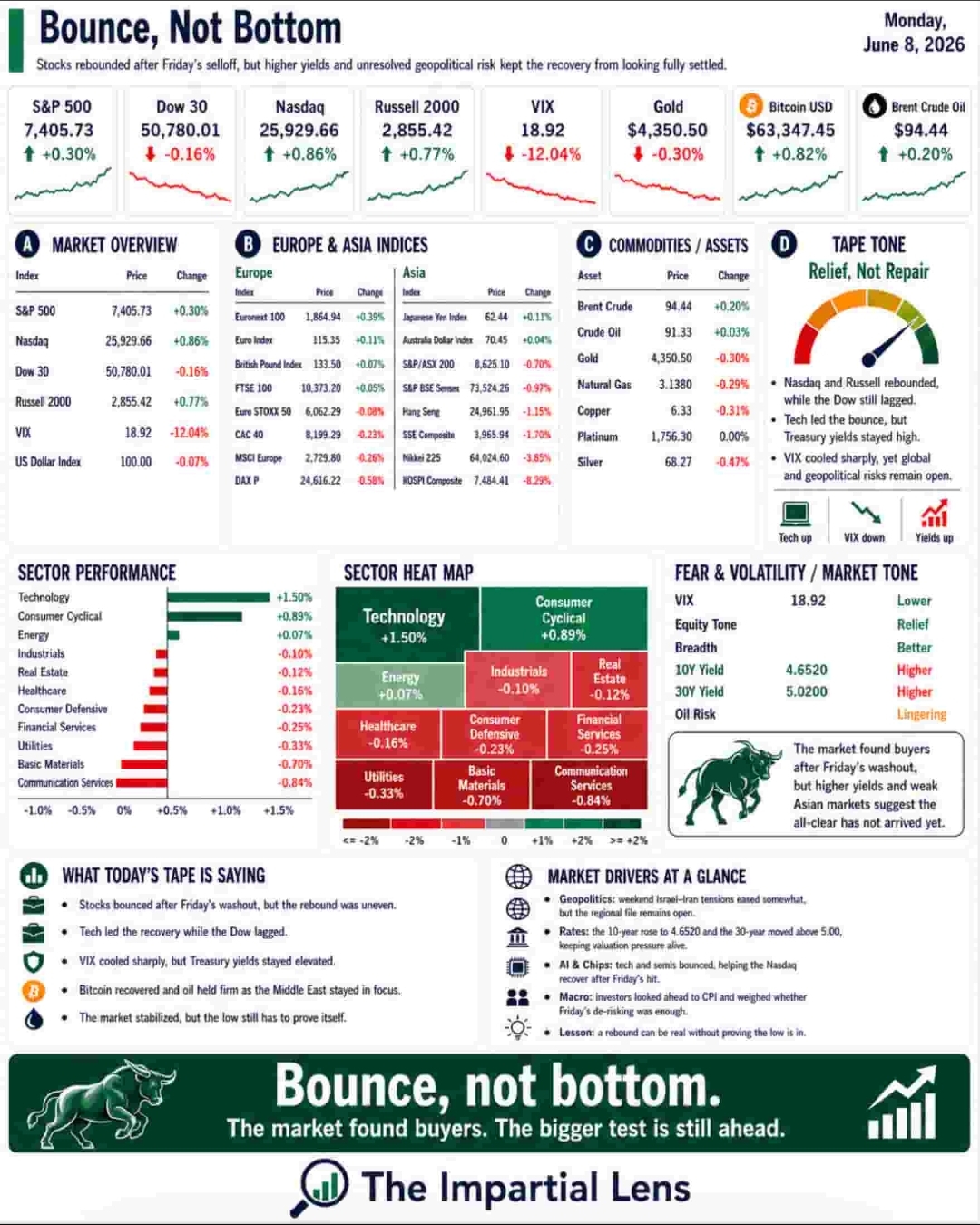

Stocks bounced on Monday after Friday’s sharp selloff. But was this a genuine repair—or just a reflex rally after a crowded trade got shaken out?

Monday delivered what investors crave after a rough Friday: green across the board. Stocks recovered. Bitcoin stabilized. Oil gave back some of its weekend spike. Tech clawed back ground. Even Israel and Iran signaled a temporary pause in direct strikes under U.S. pressure.

The tape looked calmer. But calmer isn’t fixed.

That’s the real takeaway. After Friday’s warning shot, the market had one job: show whether buyers were returning with conviction or simply buying the dip out of habit. So far, the verdict is mixed. The bounce was real. The repair remains unproven.

Friday Was a Warning, Not a Blip

Friday wasn’t just a bad day—it exposed underlying tensions.

A stronger-than-expected jobs report is great for the economy but troublesome for markets. It reduces the odds of near-term Fed rate cuts, pushes yields higher, and limits the central bank’s ability to cushion any slowdown.

The selling hit the most crowded trades hardest: semiconductors, tech, leveraged positions, and crypto. Volatility spiked. The dollar strengthened. Options positioning amplified the move.

Voluntary profit-taking can be contained. Forced unwinds from leverage and positioning often create aftershocks. Monday’s rebound didn’t erase that risk—it simply bought time for the market to prove the damage was temporary.

The Middle East Remains Unresolved

Geopolitics didn’t take the weekend off. Israel and Iran traded strikes, then both stepped back under pressure from Washington. Iran called off further direct attacks but kept its red line on Hezbollah in Lebanon. Netanyahu said Israel was holding fire “for now.”

This isn’t a ceasefire. It’s a fragile pause with strings attached. Markets love clean narratives—this isn’t one.

The region still matters because it flows directly into oil prices, inflation, shipping costs, defense budgets, and broader risk sentiment. Any disruption in the Strait of Hormuz keeps the entire chain alive.

Oil Is the Quiet Swing Factor

Oil pared gains on de-escalation talk, but the risk profile hasn’t disappeared. JPMorgan noted that prolonged disruption beyond June could meaningfully lift prices in the second half as inventories draw down.

Oil shocks rarely arrive all at once. They build gradually—through depleted stocks, stretched workarounds, higher shipping costs, and eventually higher consumer prices and inflation expectations. By the time most people feel it, markets have often been pricing it for weeks.

That’s why oil remains critical even on quiet days.

AI Rebounded, But Fragility Lingers

Tech stocks recovered on Monday, fueled by updates from Nvidia, SK Hynix, Intel, Google, and Apple on AI developments.

AI itself isn’t going away. The real question is whether the trade around it has become too crowded, too leveraged, and too dependent on nonstop good news. Friday highlighted exactly that vulnerability: forced selling in semis, ETF rebalancing, and rising correlations.

A powerful long-term theme can still become a dangerous short-term position when everyone owns the same version of the story. That’s the difference between a business narrative and a positioning narrative.

The Consumer Reality Check

Beneath the index bounce, the real economy showed continued strain. Restaurant traffic remains pressured as tax-refund boosts fade. Campbell’s highlighted persistent at-home cooking trends. Bankruptcy filings rose year-over-year in May. Mortgage burdens stay heavy, and consumer labor market expectations weakened.

The stock market can price a soft landing while many households grapple with food, rent, insurance, energy, and debt costs. Higher-income consumers keep spending; middle- and lower-income ones feel the pinch more acutely. The two don’t always move in sync.

Bottom Line

Monday was better than Friday. But it wasn’t a clean bill of health.

The bounce gave the market breathing room. Now it has to prove the selling pressure is truly behind us—not just paused. Until we see sustained conviction from buyers, higher conviction on rate cuts, and clearer geopolitical de-escalation, caution remains the smarter default.

Markets climb walls of worry, but only when the worries start to shrink. Right now, they’re still very much in play.