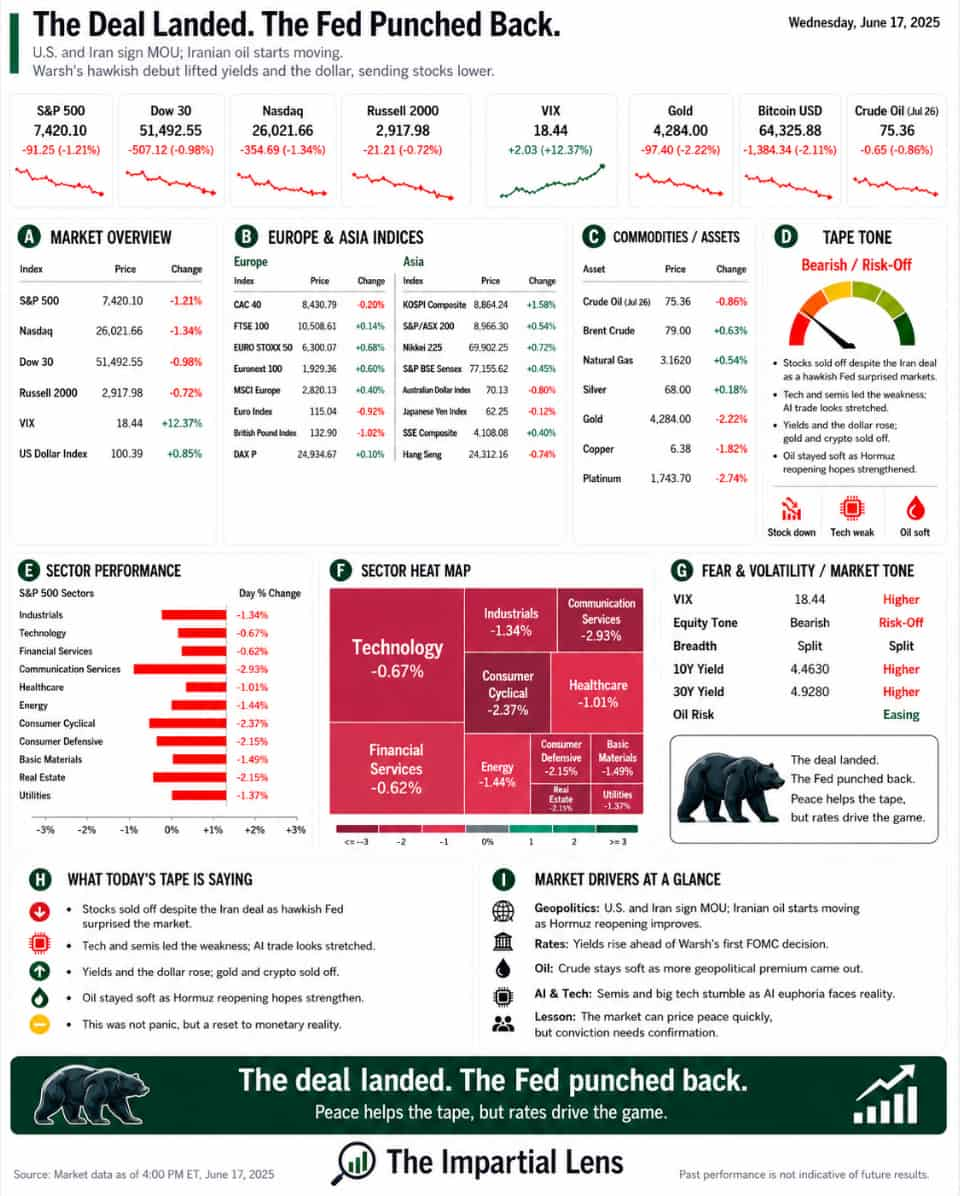

The market got exactly what it said it wanted.

The U.S. and Iran signed the memorandum of understanding ahead of schedule. The agreement is now in effect. Hopes for reopening the Strait of Hormuz shifted from speculation to reality. Iranian oil began flowing again. Tankers reversed course. Oil prices stayed under pressure, and the geopolitical nightmare that had gripped markets for days suddenly felt a lot less scary.

That should have sparked another relief rally.

It didn’t.

By the close, the tape had flipped negative. The S&P 500 dropped -1.21%, the Dow fell -0.98%, the Nasdaq slid -1.34%, and the Russell 2000 eased -0.72%. Volatility spiked, with the VIX surging 12.37% to 18.44. Gold plunged 2.22% to $4,284, Bitcoin lost over 2%, and crude held soft around $75.36 (-0.86%).

The strange part? Markets got the peace headline they craved—and sold off anyway.

Peace Was Priced In—And It Wasn’t Enough

Lesson one from Wednesday: Markets move fast on hope, but reality bites harder.

Investors had already bought the narrative for days—that a deal would reopen Hormuz, ease oil-driven inflation, and unleash risk assets. That trade worked… until verification day arrived.

A signed MOU is progress, but it’s not months of safe tanker traffic. It’s not full regional stability or guaranteed compliance across Washington, Tehran, Israel, Lebanon, and the Gulf states. It’s not permanent calm in insurance markets. Even the UAE is racing toward “zero Hormuz dependency”—a clear signal that major players see this as a warning, not a solved problem.

Markets price relief in minutes. Rebuilding energy security takes years.

Then Warsh Changed Everything

The real gut punch came from the Fed.

In Kevin Warsh’s first FOMC meeting as Chair, policymakers held rates steady as expected—but the statement, dot plot, and tone came in hawkish. Forward guidance was stripped away. The emphasis stayed firmly on hitting the inflation target. Wall Street called it the hawkish end of expectations.

Yields climbed. The dollar strengthened. Stocks reversed.

Suddenly, the market confronted an uncomfortable truth: Even if oil falls, the Fed isn’t rushing to ease. The easy backdoor rate-cut narrative tied to lower energy prices just got challenged. Warsh delivered discipline, not the soft-landing lullaby many wanted.

The AI Trade Showed Its Cracks

Tech and semis were weak again. The AI rally—real revenues, real infrastructure buildout, real strategic importance in the U.S.-China race—looked increasingly crowded and twitchy. One headline nailed it: “The Bubble Nobody Calls a Bubble.”

Underlying fundamentals matter, but so does positioning. Everyone can be right on the long-term story and still overpay in the short term. Add in soaring memory costs (Apple execs calling it a “hundred-year flood”), grid constraints, power demands, and capital intensity, and the “clean disinflationary tech story” starts looking messy.

Rotation Reality Check

The sector picture was messy: Tech and comms weak, consumer names soft, energy lagging despite the macro spotlight, financials and healthcare lower. Pockets of strength existed, but this wasn’t a clean broadening move. It felt like a market trying to rotate while the old leaders wobble and new ones aren’t ready to carry the load.

Narrow leadership is great on the way up. On the way down? Everyone suddenly discovers “breadth.”

The Real Read

Wednesday wasn’t about the Iran deal failing. It was about realizing the deal isn’t enough.

Yes, the MOU matters. Lower oil matters. Reduced tail risk matters. But markets still face the Fed, stubborn inflation, rising yields, stretched valuations, crowded AI bets, hardware cost pressures, and the simple fact that peace headlines don’t magically create earnings.

The market got its peace. Then Warsh took away the easy-money fantasy.

Bottom line: Geopolitical relief helps risk assets—but it doesn’t replace liquidity or override monetary reality.

The deal landed.

The Fed punched back.

And the tape delivered a sharp reminder.