Friday brought relief. The weekend turned that relief into a full-blown risk-on frenzy. By Monday, the market wasn’t just recovering — it was partying like the geopolitical storm had vanished.

Stocks surged.

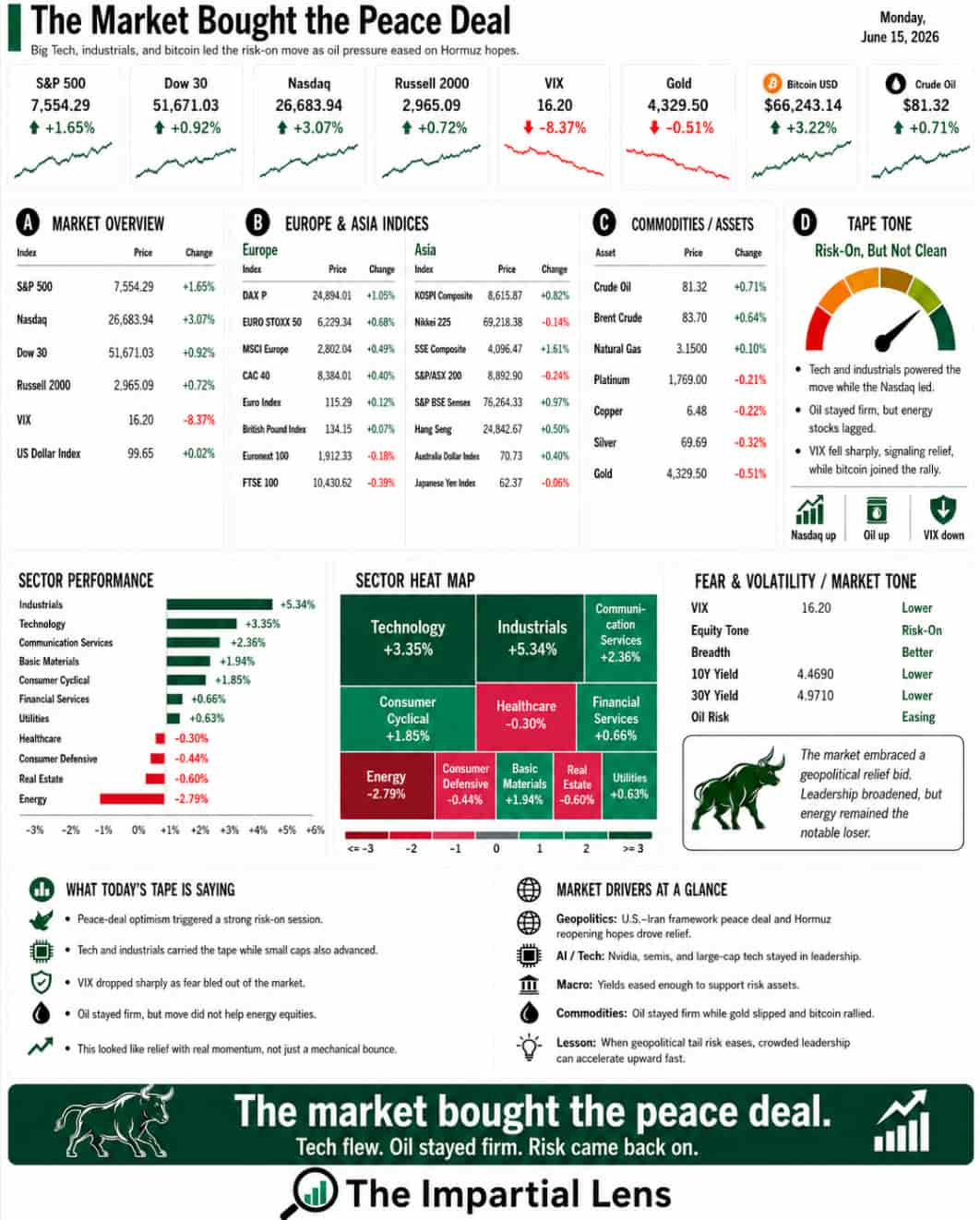

- S&P 500 climbed 1.65%

- Dow added 0.92%

- Nasdaq exploded 3.07%

- Russell 2000 gained 0.72%

Volatility cratered — the VIX plunged 8.37% to 16.20. Oil kept sliding, with Crude dropping to $81.32 (another 0.71% lower), as traders bet hard that a U.S.-Iran framework would reopen the Strait of Hormuz and banish energy-shock nightmares. Bitcoin rose, tech ripped higher, small caps joined in, industrials caught fire, SpaceX mania rolled on, and Nvidia prepped a massive bond sale. The AI trade shifted into an even higher gear.

On the surface, it was everything the market craved:

- Peace hopes

- Lower oil

- Crushed volatility

- Soaring tech and Bitcoin

- Broad gains across equities

A perfect Monday.

Except… it came with some very large asterisks.

The Deal Isn’t the Same as Delivery

The rally ignited because the U.S. and Iran suddenly looked closer to an agreement. Trump outlined the framework at the G7: no nuclear weapons, conditional sanctions relief, verification mechanisms, and a path to reopening Hormuz. Reports pointed to a two-step verification process. Markets heard “framework” and immediately repriced away the worst-case energy risks.

That logic tracks:

If Hormuz reopens → oil falls

If oil falls → inflation eases

If inflation eases → the Fed gains breathing room

If the Fed gains room → risk assets can run

The market bought that entire chain reaction.

But here’s the reality check: a framework is not peace. A memorandum of understanding is not implementation. A promise to reopen Hormuz isn’t months of safe tanker traffic. Lower headline risk isn’t the end of geopolitical tension. The market is pricing in the best-case outcome — which is possible, but far from guaranteed. It’s paying upfront for a headline that still has to survive the real world.

Oil Bulls Vanished Overnight

Oil traders didn’t just relax — they flipped completely. Headlines shifted from “Hormuz crisis” to “oil bulls have disappeared” in record time. Crude and gas prices dropped, inflation fears cooled, and risk appetite roared back.

That speed is both a gift and a warning. If the deal sticks, oil stays under pressure. If it wobbles, the violent unwind could sting. Oil isn’t just another commodity — it touches shipping, food, airlines, diesel, fertilizer, household budgets, and central bank policy. Monday’s drop helped stocks, but it also tied the market’s fortunes even more tightly to the deal actually delivering.

AI Remains the Main Character

While geopolitics grabbed the headlines, AI stayed the emotional engine of the market. Tech led the charge, semis stayed hot, and speculative names flew. SpaceX reportedly soared above $210 billion, briefly eclipsing Apple’s market cap in after-hours.

This isn’t a calm market — it’s speculative appetite with rockets attached. Yet beneath the hype, the AI story is getting more complex. The big question is no longer “Is AI real?” (It is.) It’s whether the economics can match the enormous spending.

Nvidia is raising major debt. Hyperscalers continue pouring in capital. Power transformers have record lead times. Grid infrastructure is bottlenecking. Morgan Stanley flagged power as potentially the biggest threat to the AI revolution. This is no longer just a software boom — it’s an industrial mobilization requiring massive capital, electricity, data centers, water, land, financing, and political will.

The AI Trade Is Starting to Split

The market is no longer a simple “buy everything AI” story. Dispersion is growing: top winners keep exploding while weaker names get punished. Positioning is crowded, funding rates are rising, leverage is building, and total return swaps are in demand.

The VIX may look calm, but leverage is anything but. A market can appear peaceful on the surface while growing fragile underneath. When everyone chases the same winners with borrowed money, the next reversal doesn’t need a massive catalyst — just a crowded exit.

Gold Sat This One Out

Notably, gold slipped 0.51% to $4,329.50. After quietly rallying alongside stocks last week (a hedge against lingering risks), it softened as the market went full risk-on. That’s consistent with relief — but also signals that, for now, investors are favoring growth and leverage over safe-haven protection. Classic behavior near peaks of confidence.

The Real Read

Monday delivered a powerful risk-on session. The market bought the Iran deal, the Hormuz reopening narrative, lower oil, easier inflation, more tech, more AI, and SpaceX as if the future just went public.

And maybe the bulls are right. Maybe the deal holds, oil stays soft, inflation cools, AI spending converts to real cash flows, bottlenecks get solved, and leverage doesn’t bite. Maybe we climb the wall of worry once again.

But the rally didn’t erase the risks — it simply repriced them. The deal still needs proof. Hormuz needs to reopen and stay open. AI needs more capital and infrastructure. Leverage keeps building. Tech positioning remains crowded. And this market stays headline-sensitive.

The weekend changed the setup. It didn’t end the story.

The market bought the peace deal. Now the peace deal has to deliver.