Stocks eked out gains, volatility fell, and everyone pretended the Iran headlines made sense. They did not.

The market had one of those days where the dashboard looked calm, but the headlines looked like they were written during a pub fight.

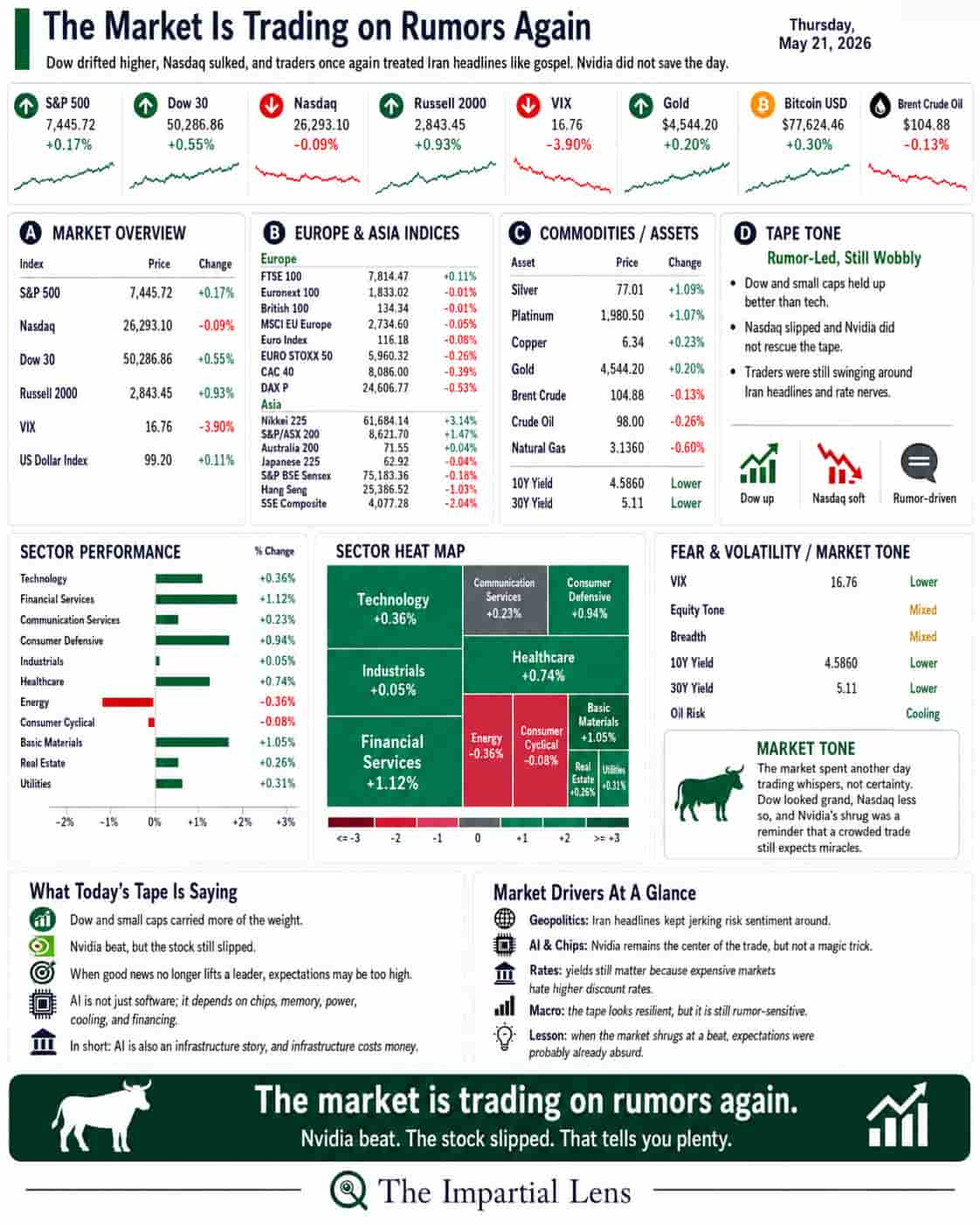

The S&P 500 rose 0.17%.

The Dow gained 0.55%.

The Nasdaq added just 0.09%.

The Russell 2000 climbed 0.93%.

The VIX dropped 3.90%.

Gold rose slightly.

Bitcoin gained modestly.

Brent crude slipped a touch.

So yes, stocks were green.

But let’s not get carried away and start handing out medals.

This was not a powerful rally. It was a market doing its best impression of confidence while waiting for the next geopolitical rumor to land.

The headline stack told the real story: reports claimed a final U.S.-Iran draft had been reached through Pakistani mediation, then those reports were denied. Trump said the U.S. would get Iran’s uranium. Iran said no, thank you very much. Rubio said some progress had been made. Nvidia slipped despite beating earnings and guidance.

In other words, the market spent the day trying to trade a peace deal that may or may not exist.

Very normal.

Nothing to see here.

The Dashboard Says: Green, But Not Convincing

The day looked fine on the surface.

Small caps did well. The Russell 2000 rose nearly 1%, which helped the tape feel healthier than the headline noise suggested. The Dow also had a decent session, up more than half a percent.

But the Nasdaq barely moved, and that matters.

For weeks, the market has been leaning on AI and tech like a man leaning on a bar at closing time. Still upright, technically. But nobody is calling it graceful.

Technology gained only 0.36%. Communication Services rose 0.23%. Industrials were basically flat at 0.05%. Financial Services did better, rising 1.12%, while Consumer Defensive and Healthcare helped hold the tape together.

A green market is not always a strong market.

Sometimes it is leadership.

Sometimes it is rotation.

Sometimes it is just everyone deciding not to panic before lunch.

Today looked more like rotation than conviction.

Nvidia Did Not Save the Day

Nvidia did well.

But the stock still slipped.

That matters because it tells us expectations are now extremely high. The market was not asking Nvidia to be good. It was asking Nvidia to be perfect.

That is the problem with crowded trades. When everyone already believes the story, good news may not be enough.

And there is another lesson here.

AI sounds like software, but it is not just software.

To run AI, companies need chips, memory, electricity, cooling systems, data centers, water, land, and billions of dollars in financing.

So AI is not only a technology story.

It is an infrastructure story.

And infrastructure is expensive.

That means rising rates, higher energy costs, or more expensive memory can all pressure the AI trade. The dream may still be real, but the bill is getting bigger.

That is why Nvidia matters.

If even Nvidia can beat earnings and the market still shrugs, it tells us the AI trade is becoming harder to impress.

Oil Is Quiet, But Not Gone

Oil slipped a little today.

Brent crude was around $104.88, which helped the market calm down.

But the oil problem has not gone away.

The market keeps reacting to every Iran headline. One minute there is talk of a deal. The next minute the deal is denied. Then oil moves. Then stocks move. Then everyone pretends this is a normal way to price risk.

It is not.

Here is the simple point:

Oil does not need to spike every day to matter.

If oil stays high, it keeps pressure on inflation. If inflation stays sticky, bond yields can stay high. And if bond yields stay high, expensive growth stocks — especially AI and tech — become harder to justify.

So yes, oil was quieter today.

But quiet is not the same as solved.

The market got a break.

It did not get an all-clear.

Bonds Are Still Watching

The 10-year yield sat around 4.58%, and the 30-year remained above 5%.

This is still the boring bit that matters most.

Equity traders want to talk Nvidia, quantum stocks, AI racks, and peace rumors.

Bond traders are asking a less glamorous question:

Who pays for all this?

Wars cost money.

AI infrastructure costs money.

Grid upgrades cost money.

Energy security costs money.

Deficits cost money.

And when everything costs money, yields tend to get a vote.

A brutal, joyless vote.

Very bond market.

Very Presbyterian.

Investor Translation

This was not a bad day.

But it was not an all-clear either.

The good news: stocks held up, small caps bounced, volatility fell, and oil did not spike.

The bad news: Nasdaq leadership was weak, Nvidia did not inspire much joy, Iran headlines remain a circus, and yields are still too high to ignore.

For the model portfolio, the message stays the same:

Stay balanced.

Do not chase every green day.

Do not abandon hedges because the VIX fell.

Keep cash useful.

Keep short-duration Treasurys.

Keep selective energy and power infrastructure exposure.

Let AI prove it can keep leading without needing perfect headlines and religious levels of belief.

The Impartial Lens View

Thursday’s market was green.

But it was not clean.

The market is still running on three things:

AI belief.

Iran rumors.

Bond-market tolerance.

That is not exactly the Holy Trinity.

More like three lads holding up a tent in bad weather and insisting the wedding can continue.

Maybe they’re right.

Maybe the tent holds.

But if oil turns higher, if yields push up again, or if Nvidia keeps fading after good news, the market may remember that hope is not a hedge.

Today was not resolution.

It was rumor management with green numbers attached.

And that is fine.

Just don’t confuse it with stability.