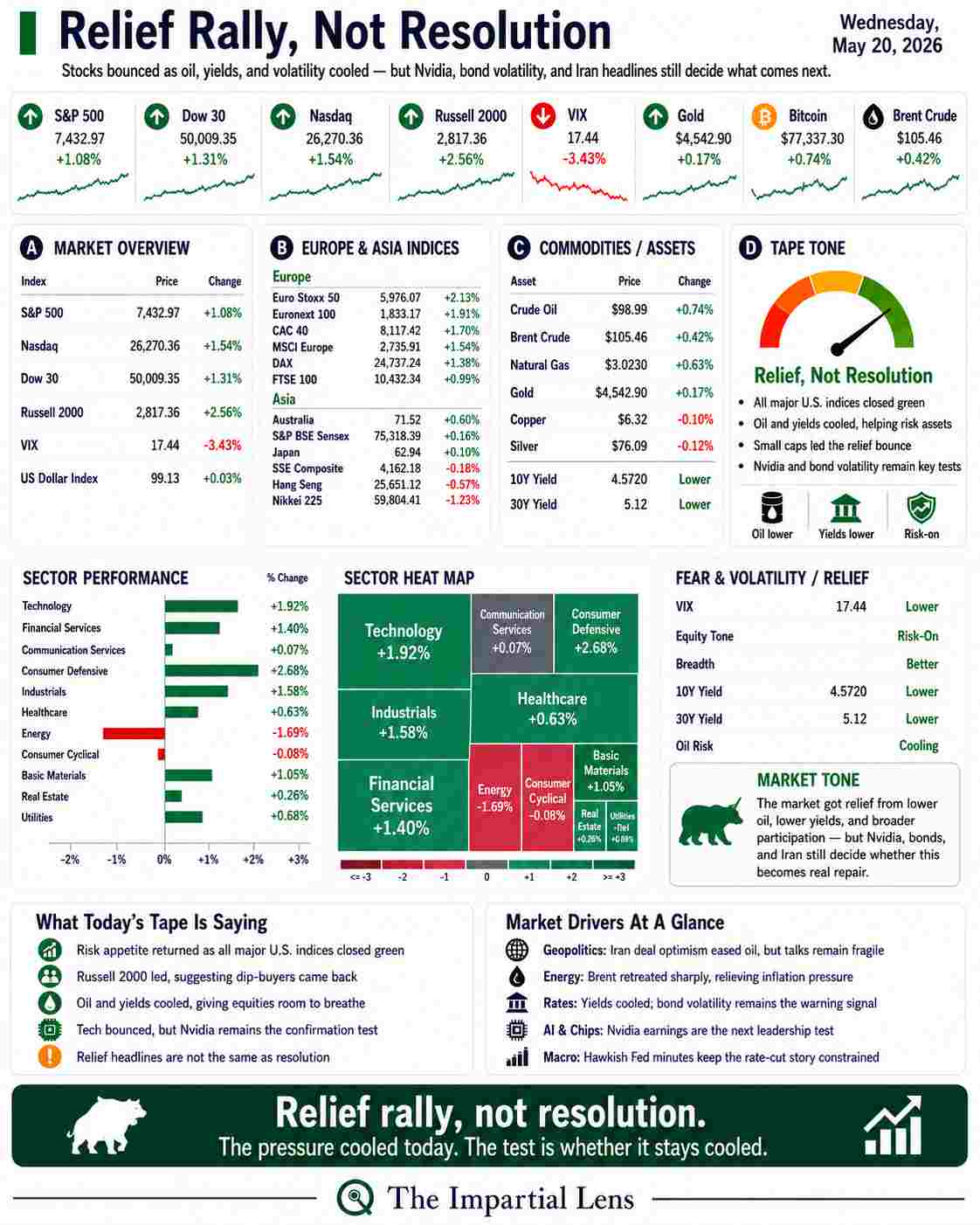

Stocks bounced because oil, yields, and volatility cooled. That is useful. But let’s not confuse a better tape with a fixed market.

The market finally got the day it wanted.

After several sessions of oil shocks, bond stress, Iran headlines, and AI nerves, Wednesday delivered the kind of dashboard that makes everyone feel a little smarter for buying the dip.

The S&P 500 gained about 0.79%.

The Dow rose about 1.31%.

The Nasdaq jumped about 1.54%.

The Russell 2000 added roughly 2.56%.

The VIX fell 3.43%.

Gold gained.

Bitcoin bounced.

Brent crude slipped.

On the surface, this looked like relief.

But relief is not the same as repair.

The market rose because the pressure points backed off for a day. Oil fell. Bond Yields eased. War headlines improved. Nvidia earnings loomed. Dip buyers came back. Risk appetite returned.

That is fine.

But nothing structural was solved.

The market did not wake up healthier.

It just woke up with fewer symptoms.

The Dashboard Says: Risk-On Returns

Wednesday was clearly stronger than Tuesday.

The Russell 2000 led with a gain of roughly 2.56%, which matters because small caps had been one of the weakest parts of the tape. When the Russell suddenly leads, it usually means investors are willing to touch risk again.

The Nasdaq gained 1.54%, showing tech regained some momentum after several weaker sessions. The Dow climbed back above 50,000, and the **S&P 500 moved higher as well.

The VIX fell to around 17.44, down more than 3%, confirming that immediate fear cooled.

So yes, this was a better tape.

Technology rose about 1.92%.

Financial Services gained roughly 1.40%.

Consumer Defensive jumped about 2.68%.

Industrials gained about 1.58%.

Healthcare added about 0.63%.

Communication Services was barely positive.

Energy lagged, falling about 1.98%, which makes sense because crude dropped.

That is a cleaner market than what we had on Monday or Tuesday.

But let’s be honest about why it happened.

Oil backed off.

That was the whole trick.

Oil Gave the Market Permission to Pretend

The biggest relief came from energy.

Brent crude fell toward the $105 area, down sharply from the stress levels that had been pressuring the entire market.

That mattered because oil had become the macro tripwire.

Oil up meant inflation pressure.

Inflation pressure meant higher yields.

Higher yields meant valuation pressure.

Valuation pressure meant trouble for tech.

Trouble for tech meant trouble for the index.

On Wednesday, that chain reversed.

Oil down.

Yields down.

Volatility down.

Stocks up.

Simple enough.

The headline stack framed it directly: renewed peace-deal optimism sparked a plunge in oil, the dollar, and bond yields while stocks and gold rallied. It also noted that stocks gained as crude fell on hopes for an end to the war, with Trump saying the U.S. was in the final stages of talks with Iran. It’s hard to keep up with Trump these days.

That is exactly the kind of headline market participants wanted.

De-escalation.

Lower oil.

Lower yields.

Higher equities.

But the market is doing what it always does after a stressful week:

It is pricing the headline as if it already became reality.

That is the problem.

Peace optimism is not peace.

It is just cheaper gasoline for investor psychology.

Iran Still Controls the Tape

The market rallied because it believed a deal was closer.

But the headlines still show tension.

There was a tense Trump-Netanyahu call as the U.S. pressed Iran to “sign the document,” while Israel reportedly wanted a military greenlight. At the same time, Pakistan was referenced as potentially announcing a final agreement formula within hours.

That is not exactly a stable backdrop.

That is a market putting on a party hat because the fire alarm stopped ringing.

A peace headline can lift stocks.

A breakdown headline can reverse the move.

This is still headline roulette.

The only difference Wednesday is that the roulette wheel landed on green.

For now.

Nvidia Is the Other Casino Wheel

Wednesday was also about Nvidia.

The market rallied into Nvidia earnings, and the upload notes that Nvidia beat expectations and issued solid guidance, yet the stock was roughly unchanged after an initial dip and recovery.

That matters.

Nvidia is not just a stock anymore.

It is the emotional support animal for the entire AI trade.

If Nvidia rallies, the market tells itself the future is still intact.

If Nvidia fades despite strong numbers, investors start asking the uncomfortable question:

How much good news is already in the price?

That was the concern going into the print. One headline asked whether all the good news was already priced in and whether Nvidia would fade again after earnings.

This is the distinction that matters:

AI can be real.

The trade can still be crowded.

The market has already priced a lot of perfection into AI, semiconductors, data centers, power infrastructure, and anything remotely adjacent to the phrase “compute demand.”

A good earnings report may not be enough if positioning is stretched.

That is where we are.

The market does not need Nvidia to be good.

It needs Nvidia to be perfect.

Bonds Still Get the Final Word

Even with yields easing, the bond market remains the referee.

One of the sharper headlines in the stack was that bond volatility remains the best leading indicator, with the durable theme being the battle between the Nvidia/AI capex trade and the bond market.

That is the whole market in one sentence.

Stocks want relief.

Bonds want discipline.

The Fed wants inflation controlled.

AI wants cheap capital.

Politicians want lower energy prices.

Investors want all the above at once.

Good luck with that.

The rally can celebrate lower oil and lower yields for a day. But if bond volatility returns, equities are right back under pressure.

That is especially true because the Fed backdrop is not exactly a warm blanket. The hawkish FOMC minutes and a divided Fed, with inflation still too high and rate cuts dependent on inflation being controlled.

So yes, yields cooled.

But the bond market has not surrendered.

It just stopped punching for a session.

AI Power Demand Is Becoming the Joke Nobody Can Ignore

Another important thread is power.

Data centers are no longer just a tech-sector footnote. They are becoming an electricity, grid, water, and infrastructure problem.

Data centers could become 33% of commercial building electricity use by 2050, and that commercial electricity use may surpass residential use in 2027 as prices continue rising.

That is not small.

It supports the case for power infrastructure, nuclear, utilities, grid upgrades, and energy security.

But it also creates a wonderfully awkward problem for the AI bulls:

What if the AI boom is inflationary?

What if the technology that is supposed to deliver abundance also drives electricity demand, grid stress, water usage, utility bills, and capital spending through the roof?

That is not a reason to dismiss AI.

It is a reason to stop treating it like magic.

Compute is not free.

Power is not free.

Water is not free.

Capital is not free.

And when all of those things get repriced, the bond market notices.

Again, all roads lead back to rates.

Today’s Dashboard Translation

Here is what Wednesday’s tape was really saying:

Risk appetite returned.

All major U.S. indices were green, and small caps led.

Oil gave the market a permission slip.

Brent fell sharply, easing the inflation panic for now.

Volatility cooled.

The VIX fell more than 3%, giving traders room to pretend the bad stuff can wait.

Tech bounced.

The Nasdaq recovered, and Technology was one of the stronger sectors.

Energy lagged.

That was less about recession and more about crude falling.

Nvidia remains the test.

The AI trade needs confirmation, not vibes.

Bonds are still the adult in the room.

Lower yields helped today, but bond volatility remains the warning signal.

Investor Translation

This was a good day for risk.

It was not an all-clear.

The rally was built on relief: lower oil, lower yields, lower volatility, and better Iran headlines.

That can absolutely carry stocks higher in the short term.

But the market still needs proof.

Oil has to stay lower.

Yields have to remain contained.

Nvidia has to hold up.

Bond volatility has to stay calm.

The Iran deal has to become real, not just rumored.

Small caps need to keep participating.

For the model portfolio, this does not mean chase everything that turned green today.

It means stay balanced.

Keep cash.

Keep short-duration Treasurys.

Keep selective energy and power infrastructure exposure.

Keep some equity exposure if breadth improves.

Do not abandon hedges just because the market had one good hair day.

Relief rallies are useful. They remind us to be cautious.