The market closed green, volatility stayed calm, and investors again acted as if oil, rates, consumer stress, and geopolitics could all be pushed safely into next week.

The market ended the week with another green tape.

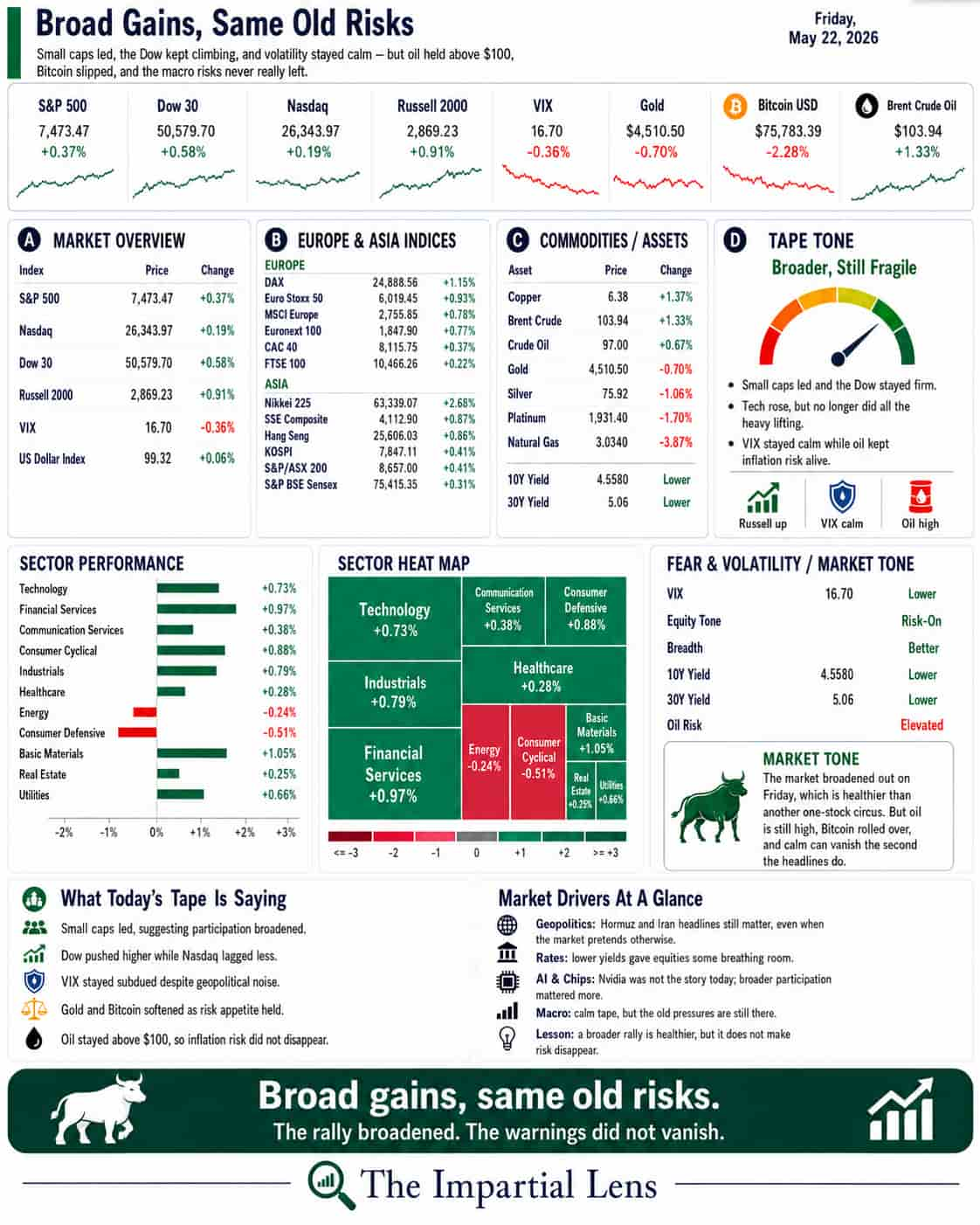

The S&P 500 rose 0.37%.

The Dow gained 0.58%.

The Nasdaq added 0.19%.

The Russell 2000 climbed 0.91%.

The VIX slipped to 16.70.

Brent crude rose to about $103.94.

Gold fell.

Bitcoin dropped more than 2%.

So yes, stocks finished higher.

But the message was not as clean as the color suggested.

This was not a broad statement of confidence. It was a market still willing to buy risk while assuming the major problems remain contained.

That may be enough for a holiday-weekend tape.

It is not the same as stability.

The Dashboard Says: Risk-On, But Selective

The headline numbers looked constructive.

All four major U.S. indices closed green, and the Russell 2000 led with a gain of nearly 1%. That helped the market look broader than a simple mega-cap tech rally.

Technology gained about 0.73%.

Financial Services rose about 0.97%.

Industrials added about 0.79%.

Healthcare rose about 0.88%.

Energy was slightly positive.

That is decent participation.

But the Nasdaq only gained 0.19%, while Bitcoin sold off and gold weakened. So this was not a full speculative surge. It was more selective.

That is the first lesson:

A green close does not always mean broad confidence.

Sometimes it means leadership.

Sometimes it means rotation.

Sometimes it means positioning.

And sometimes it means investors are choosing not to price the risks yet.

Today looked like a mix of all four.

Volatility Is Calm — Maybe Too Calm

The VIX fell to 16.70, which tells us investors are not paying much for protection.

That matters.

The VIX is often called the market’s fear gauge. A low VIX means investors are not expecting much trouble. A rising VIX means investors are paying more for insurance against market swings. When investors are less fearful and put money into the market, the VIX tends to fall while stocks rise.

That is exactly what happened on Friday.

But low fear is not the same as low risk.

It just means investors are not worried about risk right now.

There is a difference.

The headline stack was not exactly calm. We had warnings about collapsing consumer confidence, oil workarounds losing time, Treasury dumping, China refinery weakness, and the Fed losing control of rates while stocks still refuse to care.

That is the market mood in one sentence:

The risks are visible.

The market is choosing not to price them.

For now.

Oil Still Matters

Brent crude rose to about $103.94.

That is not panic pricing, but it is still high enough to matter.

Oil feeds into shipping, food, travel, freight, chemicals, and consumer behavior. When oil stays elevated, inflation pressure does not disappear. It moves through the system slowly.

The Hormuz story also remains unresolved.

Iran says ships are moving. Rubio is condemning tolls. UBS is warning about much higher oil-price scenarios if inventory buffers run dry. Workarounds are being described as temporary fixes, not real solutions.

That is the point.

Oil does not need to explode higher every day to pressure the market.

It only needs to stay high long enough to keep inflation sticky, consumers squeezed, and bond markets alert.

Bonds Are Still the Adult in the Room

The bond market remains the part of the story that equity investors would rather ignore.

Stocks can keep rising while investors chase upside, but rates still matter.

Mortgage rates are high enough to freeze out homebuyers. Treasury selling is becoming a concern. Foreign demand for U.S. assets looks less reliable. And the Fed is now under new leadership, with markets watching whether “regime change” means tougher inflation discipline.

The simple educational point:

When bond yields rise, money gets more expensive.

That affects mortgages, credit cards, corporate debt, government borrowing, AI infrastructure, and stock valuations.

So when stocks hit highs while rates remain stubborn, that is not a free lunch.

It is a bill being left on the table for later.

Investor Translation

This was a constructive close.

But not a clean one.

The good news: stocks held up, small caps led, the VIX stayed calm, and sector participation improved.

The bad news: oil is still elevated, Bitcoin weakened, gold did not act like a safe haven, consumers look stressed, and bond-market pressure has not gone away.

For the model portfolio, the message stays consistent:

Do not chase every green candle.

Keep cash useful.

Keep short-duration Treasurys.

Keep selective energy and power infrastructure exposure.

Keep some equity exposure while breadth holds.

Do not confuse low volatility with safety.

Low volatility can support markets.

But it can also encourage complacency.

That is where discipline matters.

The Impartial Lens View

Friday’s tape was green.

But the market is still walking past several warning signs.

Stocks are rising.

Volatility is falling.

Oil is still high.

Rates still matter.

Consumers are under pressure.

Geopolitics are unresolved.

AI infrastructure is getting more expensive.

And investors are again chasing upside while protection gets cheaper.

That can work.

For a while.

Markets can ignore risk longer than reasonable people expect. But ignoring risk is not the same as removing it.

The lesson of the week is simple:

The market is not pricing certainty.

It is pricing the hope that oil, rates, geopolitics, and consumer stress can all stay contained at the same time.

That may be enough for now.

Just don’t mistake it for stability.