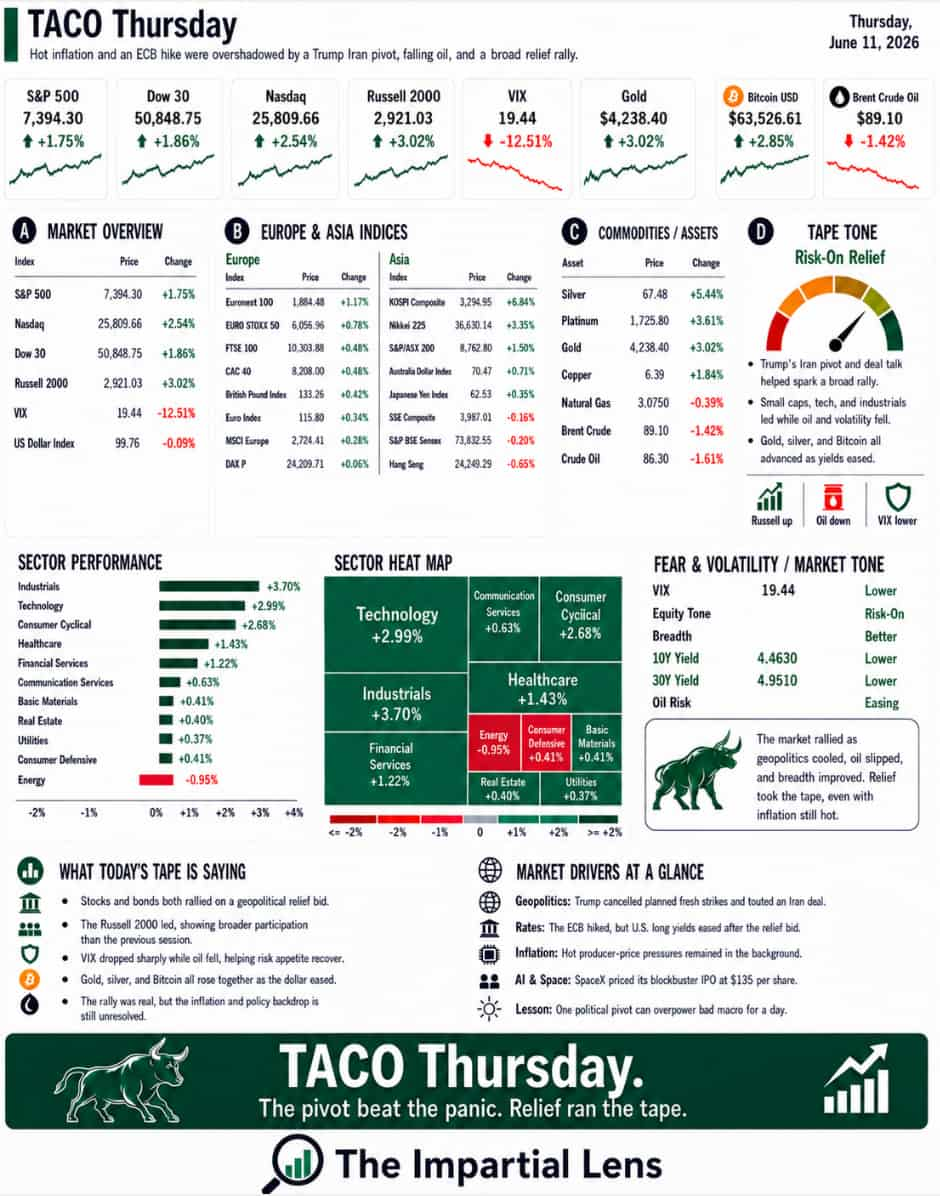

Thursday should have been a rough day.

The inflation news was not friendly. Producer prices stayed hot in the places that matter. Energy costs were surging. The ECB hiked rates for the first time since 2023 and even raised its inflation outlook, blaming the war in the Middle East for renewed price pressure. The U.S. 30-year bond auction was ugly, with weak foreign demand and dealers forced to take down more supply. Oracle disappointed investors with heavy capex guidance and talk of another large capital raise.

Normally, that mix would be enough to put risk assets on the back foot.

Hot inflation.

Higher rates.

Weak bond demand.

Expensive AI spending.

Oil risk.

War risk.

Not exactly a spa day for the market.

And yet stocks rallied.

Why?

Because Thursday became another version of the market’s favorite modern trade: TACO — Trump Always Chickens Out.

Crude fell, stocks rallied, and bonds caught a bid after Trump cancelled planned fresh strikes on Iran and started talking up a deal. He said an Iran agreement should be done “pretty quickly,” that a signing could happen soon, and that the Strait of Hormuz would reopen once a deal is signed.

That was enough.

The market did not need certainty.

It just needed a pivot.

Politics Moved The Tape Again

This is the key lesson from Thursday: the market is trading politics as much as economics.

One day, the headline is Tomahawks. The next day, it is settlement. One day, Hormuz looks like a global oil chokepoint. The next day, investors are pricing a path toward reopening. One day, Iran escalation is the inflation shock. The next day, Trump hints at a deal and oil backs off.

That is not a normal macro environment.

That is a headline-driven market where diplomacy, military threats, oil flows, and presidential language can overpower traditional data.

Markets can pretend to be rational machines.

But on Thursday, they were not trading a spreadsheet.

They were trading a Trump pivot.

And for one day, that pivot mattered more than the inflation data.

Oil Was The Release Valve

Oil has become the pressure gauge for this whole story.

When Iran risk rises, oil rises.

When Hormuz looks threatened, inflation fears rise.

When inflation fears rise, the Fed gets boxed in.

When the Fed gets boxed in, valuations get squeezed.

But when Trump cancelled strikes and talked up a deal, oil fell. That gave the market permission to breathe.

This is why oil is not just a commodity story anymore. It is the bridge between geopolitics and the Fed.

If oil spikes, inflation becomes harder to control. If oil falls, the market can pretend the inflation problem is manageable again.

Thursday was one of those days where oil gave stocks just enough oxygen.

But let’s not confuse oxygen with health.

The Middle East is still unstable. Iran still needs internal approval, according to reports. Hormuz remains the central pressure point. Tanker flows, insurance costs, Gulf allies, U.S. military posture, and Iranian retaliation risk are still part of the tape.

The market rallied because the fire alarm got quieter.

That does not mean the building is fireproof.

The Inflation Problem Did Not Disappear

The uncomfortable part is that the inflation backdrop did not magically improve.

The ECB hiked rates and cut growth while raising its inflation outlook. That is a nasty combination. It says policymakers are worried about prices even as the economy slows.

In the U.S., PPI sent a mixed but uncomfortable message. Core producer prices were cooler than expected, but goods costs jumped, and energy costs remain a problem. That matters because producer prices can work their way through supply chains and eventually show up for consumers.

So, the market’s celebration was not really about inflation improving.

It was about oil falling enough to make investors hope inflation will not get worse.

That is a much thinner story.

Inflation is still sticky. Energy is still political. Rates are still elevated. And the bond market is still making governments pay for borrowing.

That ugly 30-year auction was not a side note. It was a warning.

Foreign demand weakened. Dealers had to take down more supply. That is the bond market’s way of saying: if governments want to borrow this much, somebody has to be paid to absorb it.

Stocks can rally on a headline.

Debt has to be financed every day.

AI Is Becoming A Volatility Story

The other major theme was AI.

SpaceX priced the biggest IPO ever at $135 per share, and the market treated it like a new frontier moment. The hype was enormous. Some called it the most hopeful IPO. Goldman reassured investors that fundamentals, valuations, speculation, supply, and IPO conditions were all fine.

That is usually when adults should start checking the exits.

At the same time, the AI buildout is becoming more expensive and more complicated. Goldman sees 2027 hyperscaler capex potentially rising as high as $1.4 trillion. Oracle slid on capex guidance and capital-raise concerns. AI price wars are beginning, with OpenAI reportedly considering drastic price cuts to win Anthropic customers. Token spending is under pressure. Power grids are becoming a constraint. Industrial gas, data centers, chips, memory, and electricity are all becoming part of the AI trade.

This is no longer just a software story.

It is an infrastructure story.

And infrastructure stories need capital.

Lots of it.

That is why AI is becoming a volatility story. The market still loves the dream. But it is starting to price the invoice.

Cash has low volatility. Massive capex cycles do not.

The Two-Way Panic Market

Thursday’s rally does not mean the market is calm.

It means the market is now panicking in both directions.

That sounds strange, but it fits the tape.

When positioning is crowded, leverage is high, liquidity is thin, and headlines are extreme, the market can move violently up or down. Negative gamma, leveraged ETFs, AI concentration, and geopolitical uncertainty create a setup where small changes in narrative can produce large moves in price.

That is why one presidential pivot can send stocks and bonds higher even when inflation data, rates, and AI capex all look uncomfortable.

This is not healthy confidence.

It is unstable relief.

The market is not saying everything is fine.

It is saying the worst-case scenario got delayed.

There is a difference.

The Real Read

Thursday was not a clean risk-on day.

It was a political relief rally.

Stocks and bonds rallied because Trump stepped back from fresh Iran strikes and talked up a deal. Oil fell because the market saw a path, however fragile, toward Hormuz reopening. Risk assets rallied because investors wanted to believe the inflation shock could be contained.

But the problems underneath did not disappear.

Inflation is still sticky.

The ECB is hiking again.

The 30-year auction was ugly.

Foreign demand for debt weakened.

AI capex is still exploding.

Oracle reminded investors that growth dreams come with financing needs.

SpaceX showed that speculative appetite is still alive.

And the Middle East is still one headline away from moving oil again.

That is the real read.

The market did not rally because the world got clean.

It rallied because the political headline got less bad.

This is why the tape feels so strange.

One day, Tomahawks.

Next day, settlement.

One day, oil shock.

Next day, oil relief.

One day, inflation panic.

Next day, TACO rally.

The market is not calm.

It is reactive.

And in a reactive market, the most dangerous assumption is that one good headline fixes the whole problem.

Thursday’s lesson was simple:

The market chose the pivot.

But the bill is still on the table.