Friday handed Wall Street exactly what it craved in that moment—not real solutions, not a clean macro picture, not cheaper AI power, not a permanently fixed oil market, and certainly not a rock-solid bond market. Just enough hope to spark a relief rally and let traders buy the close with a sigh of relief.

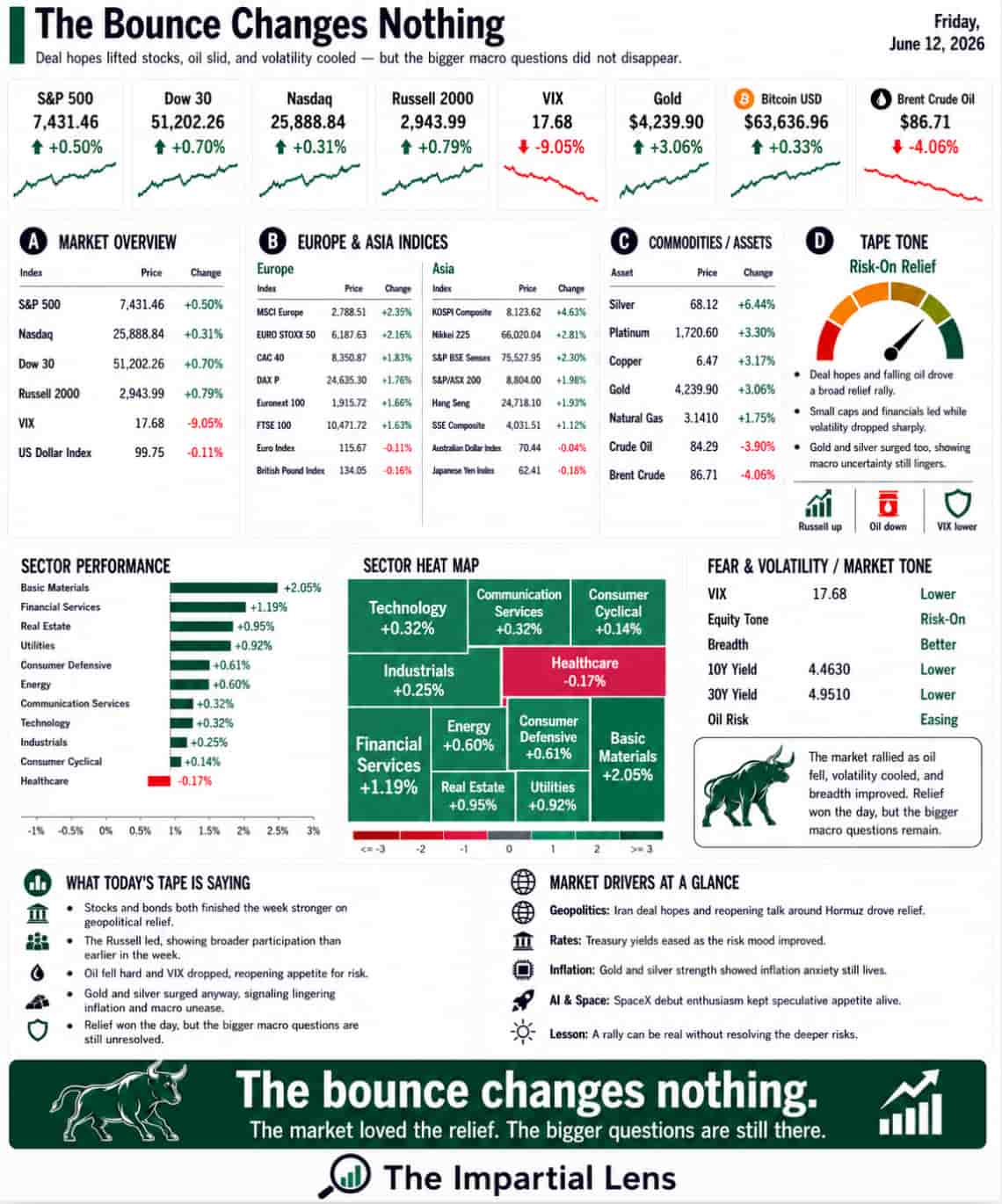

The major indices responded enthusiastically. The S&P 500 climbed 0.50% to close at 7,431.46, the Dow rose 0.70% to 51,202.26, the Nasdaq added 0.31% to 25,888.84, and the Russell 2000 gained 0.79% to 2,943.99. Volatility took a breather too—the VIX dropped a sharp 9.05% to 17.68. It felt like the panic button had been tucked safely back under the glass.

But the real star of the show? Oil. Crude fell 3.90% to $84.29, while Brent dropped 4.06% to $86.71. That plunge acted as the ultimate relief valve. Suddenly, whispers of an Iran deal—complete with peace prospects, inspections, a reopened Strait of Hormuz, unlocked UAE funds, and lifted sanctions—gave everyone permission to exhale. Tail risk? Shrinking fast. Risk assets? Time to party.

The Market Bought the Deal Hope—Not the Reality

Let’s be clear: the rally wasn’t fueled by a suddenly peaceful world. It was powered by the narrative shifting from missiles to memorandums. Officials floated visions of stability; reports suggested a final text was in hand. Markets, ever opportunistic, did what they do best: buy first, verify later.

Oil’s sharp decline cascaded through the tape. Lower energy prices ease near-term inflation fears, giving central banks breathing room. That stability buoys bonds, which in turn green-lights stocks. It’s a beautiful, logical chain—as long as the deal actually delivers.

The Strait of Hormuz isn’t just geography; it’s the world’s energy pressure valve. Ships flowing freely calm markets. Any disruption, and inflation sneaks back in through the side door. Friday priced in hope. It did not price in proof.

The AI Party Got Its SpaceX Moment

Right on cue, SpaceX delivered the perfect feel-good subplot. The company debuted trading 19% higher after pricing its massive IPO at $135 per share—the biggest ever. Headlines screamed. Elon Musk reportedly entered the “four commas club.” Valuations rocketed into the stratosphere.

SpaceX checks every box for this market’s dreams: frontier tech, national security, rockets, satellites, government contracts, bold ambition, and that irresistible aura of destiny. It didn’t need Day One earnings. It needed belief—and belief was abundant on Friday.

Yet beneath the celebration lurks a less glamorous truth about the broader AI supercycle. Hyperscalers are reportedly leaning on special-purpose vehicles and creative financing to mask parts of their commitments. One estimate pegs off-balance-sheet AI spending at around $1.8 trillion. That’s not pocket change—it’s the massive invoice hidden behind the magic.

The Uncomfortable Reality: AI Needs Real Money

AI may be transformative. Compute might become the new oil. SpaceX is undeniably extraordinary. But none of this is free.

Data centers demand chips, land, water, cooling systems, grid upgrades, power contracts, gas turbines, backup infrastructure, debt, equity, and political goodwill. The dream sells like sleek software; the reality is gritty industrial-scale spending. Markets adore the upside story but are only starting to grapple with the costs.

As one Goldman compute desk insight put it, investors should watch the market price of compute. The bottleneck may not be raw intelligence—it could be cold, hard economics. Token costs can drop, open-source models can advance, and local inference can expand, but if infrastructure spending outpaces monetization, the big question looms: Who actually earns the return?

That’s not inherently bearish. It’s just honest. Progress has a price tag.

Gold Was Quietly Loud

While stocks cheered the relief, precious metals sent a different message. Gold surged 3.06% to $4,239.90, silver jumped 6.44% to $68.12, platinum rose 3.30%, and copper gained 3.17%.

That’s a telling divergence. A fully relaxed market wouldn’t see gold and silver ripping higher alongside equities. Stocks toasted the deal hope. Gold kept one eye on the exits, whispering: Don’t get too comfortable.

Inflation risks, currency pressures, geopolitical tensions, and questions around central bank credibility haven’t vanished. The tape showed split personality—risk-on in equities, caution in safe havens.

The Real Economy Remains Uneven

Beyond the headlines, warning signs persisted. Initial jobless claims have ticked higher. Hiring is patchy across regions. Gas prices eased for a third week (a consumer win), but some states remain above $5 per gallon. Heat waves triggered grid emergencies in the Southeast due to surging air-conditioning demand. Private credit saw more redemption gates, and net equity supply turned positive for the first time since the pandemic.

None of these scream immediate disaster, but they underscore a key point: liquidity isn’t infinite, infrastructure is strained, and the real economy isn’t marching in perfect lockstep. Markets can rally through these frictions—they just shouldn’t pretend the frictions don’t exist.

The Real Read: Relief Is Not Repair

Friday delivered a classic relief rally. Stocks climbed, oil eased, volatility cooled, SpaceX soared, gold and silver shone, and Bitcoin held firm. A softer geopolitical headline was all it took for risk to roar back.

That makes perfect sense in the moment. But it doesn’t resolve the deeper tensions.

The Iran deal still requires real-world proof. Hormuz must actually reopen—and stay open. Oil traders might be piling into shorts as if the crisis evaporated. AI capital expenditure remains enormous. Off-balance-sheet commitments keep mounting. Private credit shows ongoing stress. Equity supply is returning. And the market stays headline-sensitive.

The bounce changes nothing.

It reveals that investors are eager to embrace relief. It does not prove the world is fixed. The week ended with hope in one hand and a very large bill in the other.

Oil signaled cooling war risks.

Gold warned that fear lingers.

SpaceX proved speculation thrives.

AI reminded everyone the invoice is growing.

For one more trading day, the market decided that was good enough.

The Lens: This was a bounce. Not a verdict.

Markets will keep dancing to the latest headline. Smart investors stay focused on the fundamentals underneath the noise. What do you think—will the hope hold, or is another reality check coming? Drop your thoughts below.