Monday was the party. Tuesday brought the bill.

The markets charged into Tuesday riding a wave of euphoria. A U.S.-Iran framework deal, the story went, would reopen the Strait of Hormuz, slash the oil risk premium, tame inflation, and hand investors the green light to pile back into tech.

For one glorious day, it all worked perfectly.

Then reality hit.

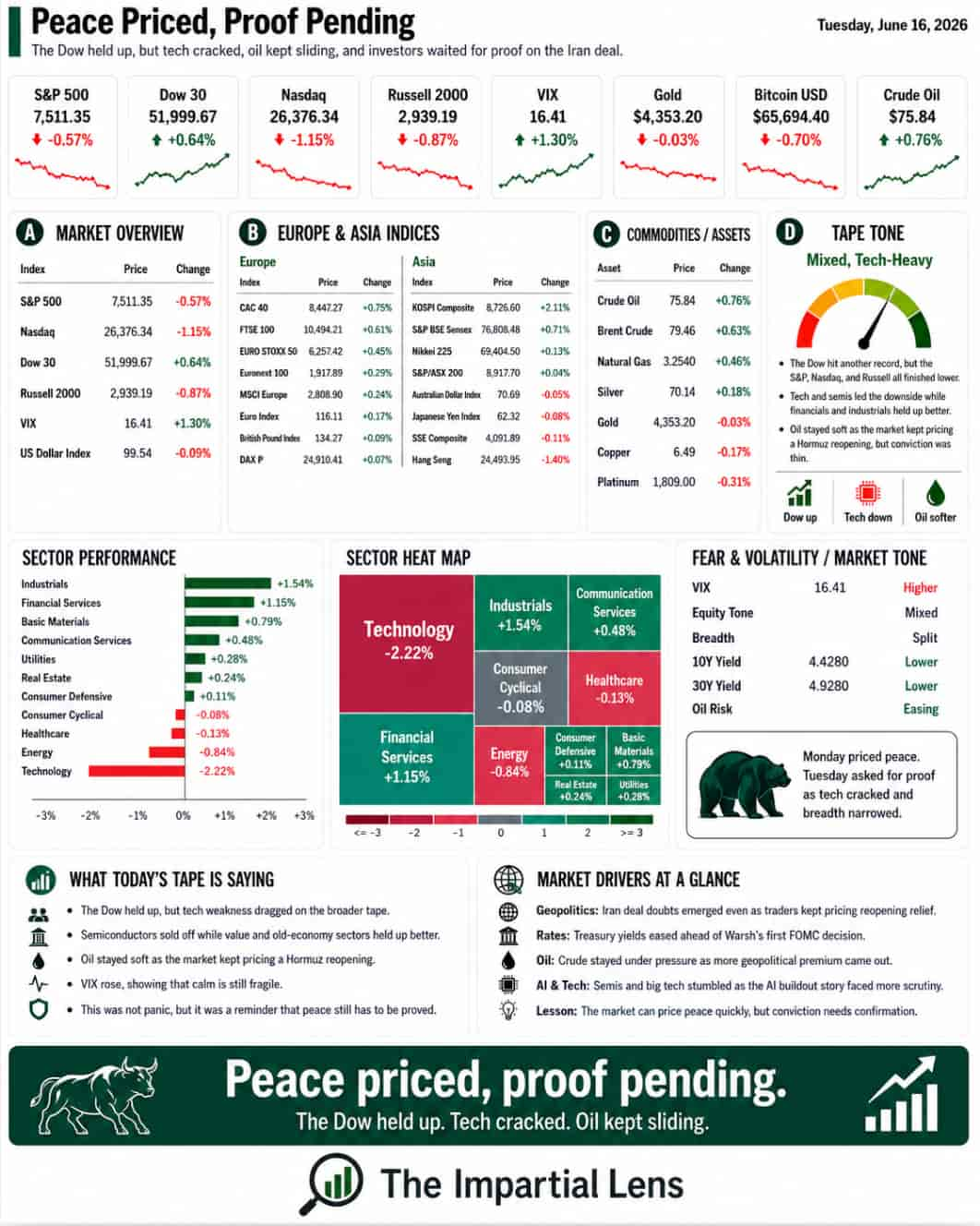

The major indices finished mixed. The Dow managed a respectable +0.64%, but the S&P 500 slipped 0.57%, the Nasdaq dropped 1.15%, and the Russell 2000 fell 0.87%. Not a bloodbath, but hardly the ringing endorsement the bulls were hoping for.

The VIX ticked up 1.30% to 16.41, signaling that fear is low but no longer shrinking. Crude oil stayed soft around $75.84, gold barely budged (-0.03% to $4,353.20), and Bitcoin eased as well.

The headline lesson? The “peace trade” is still alive — but it’s no longer getting a free ride.

The Deal Still Has to Become Real

Geopolitics remains the market’s biggest driver. Monday’s rally was built on hope. Tuesday introduced inconvenient questions:

- Lebanese and Iranian officials demanding the U.S. rein in Israel

- Israeli hardliners reportedly furious

- Doubts about whether Tehran will deliver real nuclear concessions

- Reports that Trump believes the deal can survive an Israeli strike on Lebanon

That’s not exactly the clean “peace” narrative Wall Street prefers.

Markets love simple stories: Deal signed → Hormuz reopens → Oil crashes → Inflation cools → Risk-on rally.

Reality is messier. Tanker traffic, insurance, sanctions relief, verification, mines, Qatar’s LNG output, Iranian politics, Israeli politics, and U.S. credibility all still matter.

Peace has been priced. Proof is still pending.

Oil May Be Getting Too Comfortable

Oil’s continued slump was the central theme of the session. Lower crude means easier inflation pressure and more room for central banks to maneuver — exactly what the risk-on crowd wants to hear.

But there’s danger in the calm. Traders are positioning as if the Hormuz crisis is ancient history. If the deal falters, a violent short squeeze could follow.

Oil is no longer just an energy price — it’s the market’s live confidence meter for the entire geopolitical story. Right now it’s flashing “trust is rising.” History shows that trust in this region can vanish overnight.

Tech Lost the Leadership Baton

The most telling shift? Tech’s sudden weakness.

The technology sector fell 2.22%, dragging the Nasdaq lower. After leading Monday’s charge, the engine sputtered the very next day.

Semiconductor stocks took a hit after reports that Microsoft balked at a major Oracle cloud deal. The AI narrative is shifting from “Who benefits?” to tougher questions:

- Who actually pays for these massive data centers?

- Who funds the power infrastructure?

- Who takes the margin pain when compute gets cheaper?

- What happens to stranded assets if demand doesn’t keep up?

The “compute is scarce” story is showing cracks. Cheaper intelligence could explode demand — or destroy pricing power. That trillion-dollar question remains unanswered, and the market is starting to punish the uncertainty.

Not Everything Was Weak

This wasn’t a broad selloff. There was clear rotation underway:

- Industrials +1.54%

- Financials +1.15%

- Communication Services +0.48%

Basic materials, utilities, and real estate also posted gains.

The market isn’t dumping everything — it’s trying to broaden the rally. But the handoff is messy. Consumer cyclicals, healthcare, and energy weakened. Tech got hammered.

Will financials and industrials carry the load if tech continues to fade? That’s the critical test ahead.

The Fed Is Back in Focus

Meanwhile, central banks are reclaiming center stage. The Bank of Japan hiked rates to 1% — its first move in 31 years. Attention now turns to Kevin Warsh’s first FOMC meeting.

Housing starts just hit their lowest level since May 2020. The real economy remains uneven, consumers are stretched, and valuations are stretched. The Fed faces a tightrope:

- Too hawkish → risk assets wobble

- Too dovish → inflation fears return

- Too vague → back to headline-chasing

The Real Read

Tuesday wasn’t a crash. It was a meaningful pause.

The market bought peace on Monday. On Tuesday it started asking for receipts.

Oil is pricing relief. Tech is pricing doubt. Financials and industrials are trying to broaden the base. Volatility is low but stopped falling.

The easy part was buying the headline. The hard part is living with the details.

A deal still has to become a real deal. Hormuz still has to reopen and stay open. Iran still has to comply. Israel still has to be contained. AI capex still has to prove its worth. The Fed still has to thread the needle.

Monday was risk-on. Tuesday was the market asking for proof.

Peace has been priced. Proof remains pending.