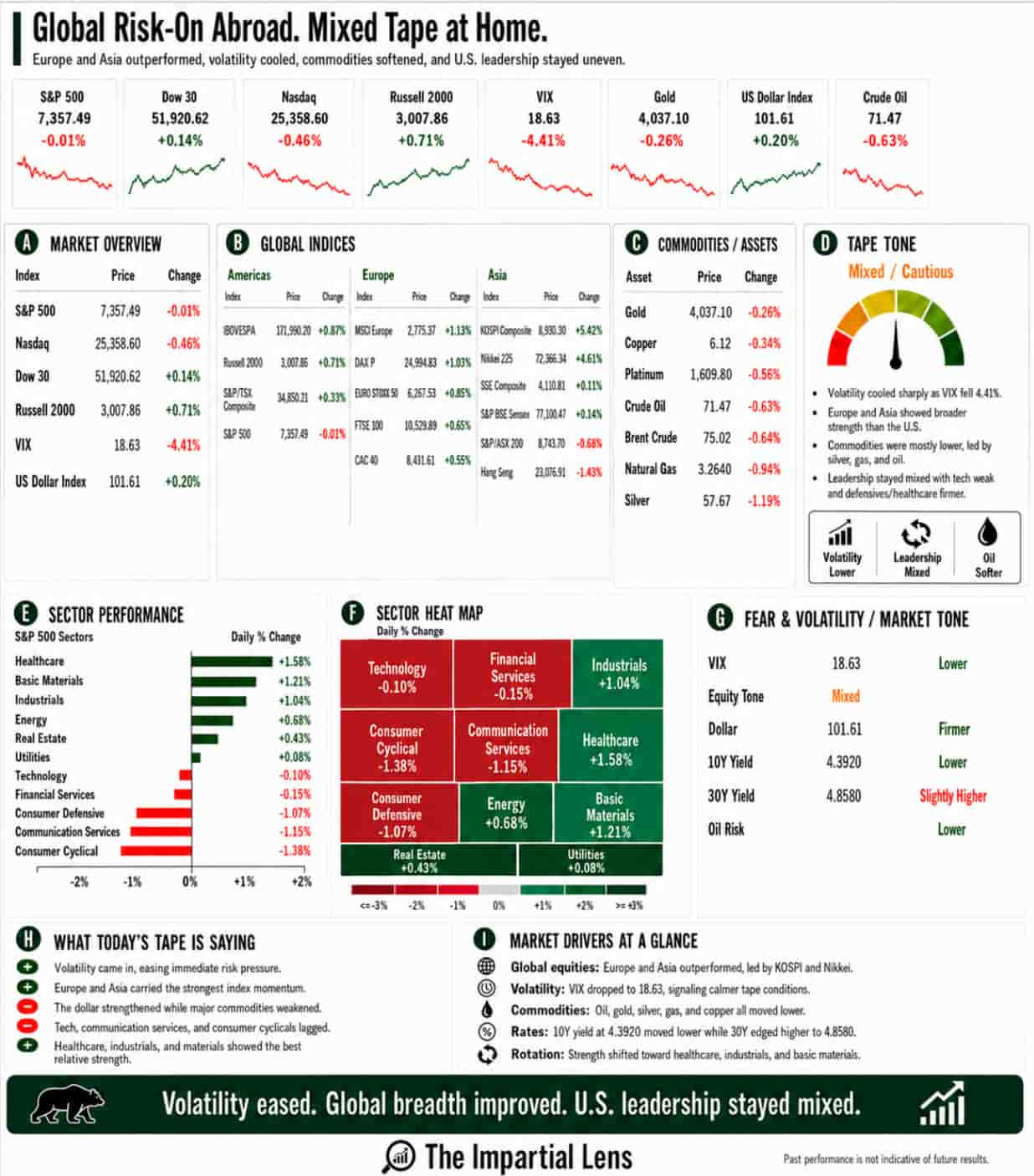

Thursday looked calm on the surface. Underneath, it was anything but clean.

The S&P 500 finished essentially flat, down just 0.01%. The Dow eked out a 0.14% gain. The Russell 2000 rose a more respectable 0.71%. But the Nasdaq slipped 0.46%, keeping pressure squarely on tech and AI leadership. Volatility ticked higher, with the VIX rising 1.40% to 18.89. Gold slipped 0.26% to $4,037.10. Bitcoin dropped 1.83% to $59,668. Crude oil fell 0.63% to $71.47 despite fresh headlines out of the Strait of Hormuz.

The headline numbers told one story. The tape told another.

Micron Delivered — But the Rally Didn’t Spread

Micron gave the market exactly what bulls had been hoping for: blowout earnings and stronger guidance, driven by surging AI-related memory demand. For a moment, it worked. The stock surged, AI sentiment got a short-term lift, and investors saw confirmation that the memory cycle remains very much alive.

Then reality set in.

The rally failed to broaden. Apple sold off sharply on concerns about memory-driven price hikes hitting its Mac and iPad lines. Microsoft weakened. Communication services dropped. Technology finished slightly negative. Bitcoin stayed under pressure. The Nasdaq couldn’t hold leadership.

That was the real tell.

Good news from one major AI beneficiary is no longer enough to lift the entire complex. The market is beginning to separate the companies benefiting from AI from the companies paying for it. For months, AI was treated as a rising tide that lifts all boats. Now it’s starting to look more Darwinian — and more expensive.

AI Is Quietly Becoming an Inflation Story

This may be the most important development of the day.

AI is no longer just a growth narrative. It is rapidly becoming a cost and inflation story. Data-center buildouts, memory shortages, chip demand, and surging power needs are all feeding into higher costs. Apple is already raising prices. Microsoft is feeling the pressure. Hardware and infrastructure costs are climbing.

The market is now forced to confront a harder question: What if AI boosts revenue and margins for a handful of winners while simultaneously raising costs for everyone else?

This isn’t bearish on AI as a technology. Demand is real. The productivity potential is real. But the buildout is capital-intensive, energy-hungry, and running into already-tight supply chains. That makes AI both a powerful growth engine and a new source of cost pressure. The market loves the first part. It’s far less comfortable with the second.

Hormuz Risk Isn’t Gone — It’s Just Quieter

Oil prices fell, but the underlying story remains messy. Reports of a cargo vessel coming under attack near Oman, continued Iranian signaling around the Strait of Hormuz, and the gap between U.S. messaging and Iranian rhetoric all point to unresolved tension.

Markets want to treat recent developments as an exit ramp. An exit ramp only works if both sides are actually walking down it. Tanker rates, insurance costs, and security risks haven’t disappeared. Lower crude helps the macro backdrop and eases one inflation worry — but it doesn’t mean the geopolitical risk has been neutralized.

PCE Data Kept the Fed in the Room

The latest inflation reading offered no clean victory for either side. Headline monthly PCE cooled, but year-over-year headline and core readings stayed hotter than the market wanted. Services costs remained sticky. Continuing jobless claims stayed elevated even as initial claims fell.

It’s a mixed picture that gives both bulls and bears ammunition. Bulls can point to cooling trends and oil relief. Bears can highlight sticky services, mixed labor data, and the new AI-related cost pressures entering the system.

This keeps the Fed focused on credibility. If AI-driven costs, sticky services inflation, and the potential for oil risk to return quickly are all in play, the Fed has little room to sound dovish. That’s why the dollar and yields matter so much right now. The market isn’t just pricing growth — it’s pricing policy credibility.

The Sector Tape Revealed a Defensive Rotation

The sector map made the day’s character clear:

- Healthcare led with a +1.58% gain

- Industrials rose +1.04%

- Energy gained +0.65%

- Utilities and real estate also finished positive

Meanwhile, the risk-sensitive areas struggled:

- Consumer Cyclical fell -1.38%

- Communication Services dropped -1.15%

- Financials slipped -0.15%

- Technology was down -0.10%

This wasn’t a strong risk-on tape. It was a defensive rotation with pockets of strength. The Dow and Russell held up. The S&P 500 barely moved. The Nasdaq lagged. Volatility rose. Bitcoin and gold both declined.

Not panic. But not confidence either.

The Real Read

Thursday was full of contradictions:

- Micron delivered, yet tech leadership cracked.

- Oil fell, yet Hormuz risk lingered.

- Inflation cooled in spots, yet services costs stayed sticky.

- The Dow and Russell rose while the Nasdaq fell.

- The S&P 500 held flat while the VIX climbed.

The market is not collapsing. It is negotiating.

It is negotiating between AI optimism and AI-related cost inflation. Between oil relief and lingering geopolitical instability. Between falling crude and sticky services prices. Between defensive rotation and stretched tech leadership. Between a Fed protecting credibility and investors still hoping for relief.

There are too many moving parts, and none of them are giving a clean answer.

The AI story remains alive — Micron proved that. But it is no longer being treated as a free lunch. The market is starting to ask the harder, healthier questions: Who truly benefits? Who pays? Who has pricing power? Who absorbs the costs? And who is simply crowded into the same trade?

That shift makes the tape choppier in the short term. It also makes the market more honest.

The market held. The risk trade cracked.