Monday gave the market a cleaner message.

After the long weekend, buyers came back to growth.

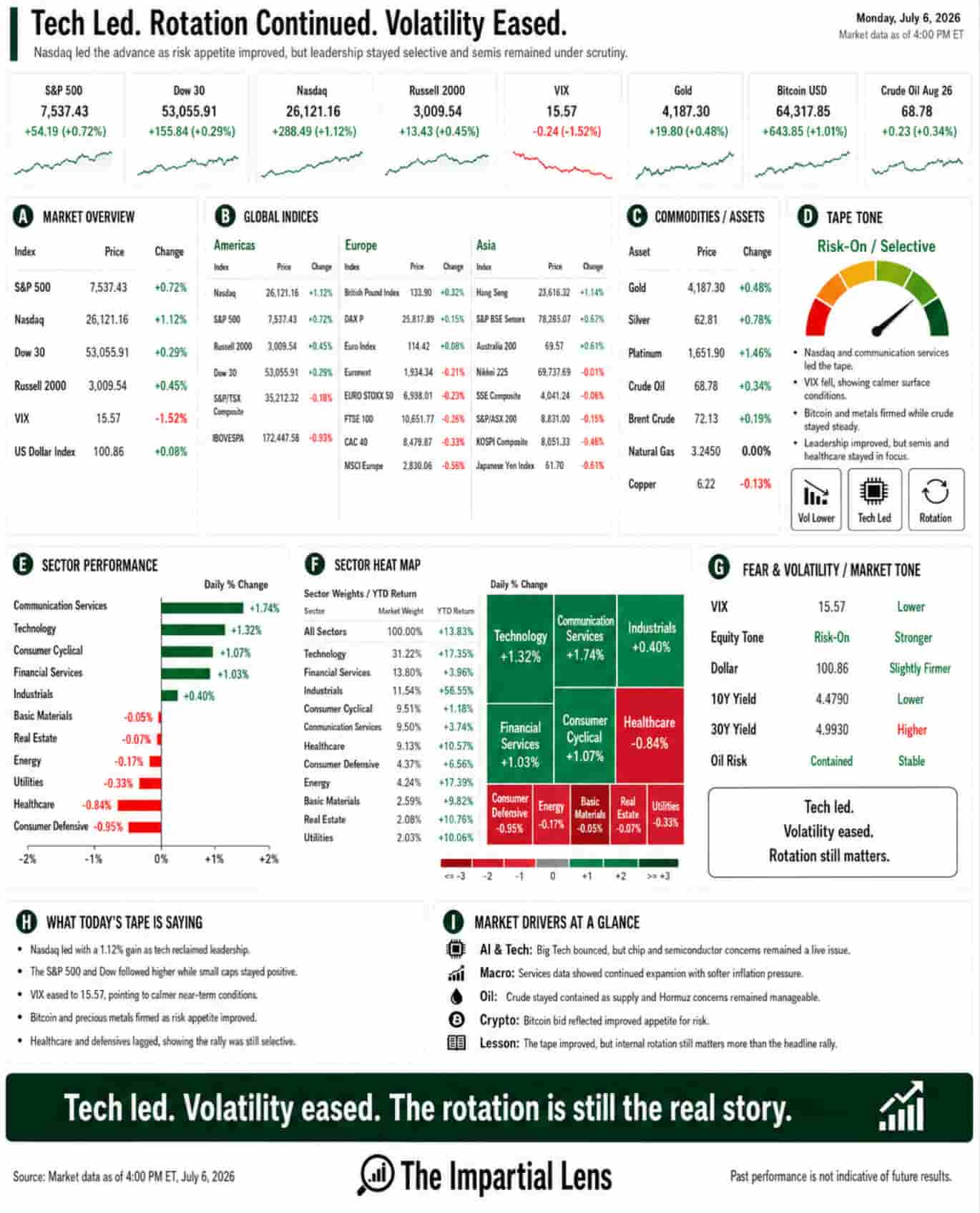

The Nasdaq rose 1.12%. The S&P 500 gained 0.72%. The Dow added 0.29%. The Russell 2000 climbed 0.45%.

Volatility cooled, with the VIX down 1.52%.

That is a risk-on setup.

But it was not just a blind rally.

Technology led. Communication services led. Consumer cyclicals and financials joined. Bitcoin caught a bid. Gold rose. Oil moved slightly higher. Defensives lagged.

So the market was not hiding.

It was reaching again.

The question is whether it was reaching for durable growth or simply chasing the familiar AI trade after another round of doubt.

Tech Led The Tape

The sector map was clear.

Technology rose 1.32%. Communication services gained 1.74%. Consumer cyclical rose 1.07%. Financial services added 1.03%.

That is the type of leadership bulls want.

When tech, communication services, and consumer cyclicals are leading together, the market is usually telling you investors are willing to take risk. That was Monday’s tape.

But there is a difference between leadership and certainty.

The AI trade has been under pressure for a reason. Investors are starting to separate the story into pieces. Nvidia denied reports of delays. Broadcom and Apple chip headlines helped sentiment. Hyperscalers still look important. But the chip supply chain, memory cycle, data centers, and power infrastructure are all being inspected more closely.

The old version of the AI trade was simple:

Buy everything connected to AI.

The new version is harder:

Figure out who captures the economics.

That is where the market is now.

AI Is Still Powerful. It Is Also Getting More Complicated.

AI is still the market’s center of gravity.

That did not change on Monday.

What did change is the level of scrutiny.

Morgan Stanley reportedly told clients to prefer hyperscalers over chip stocks. That is important because it suggests Wall Street is no longer treating the AI supply chain as one giant winning trade.

The market is asking harder questions.

Who benefits if AI inference gets cheaper?

Who gets squeezed if capex expectations slow?

Who owns the customer relationship?

Who owns the power?

Who owns the data center?

Who is just selling into a temporary spending wave?

That is the more mature phase of a market theme.

The story does not disappear.

It fragments.

And once a theme fragments, stock picking matters more. Positioning matters more. Valuation matters more. Margins matter more.

The market can still rally on AI.

But it is no longer enough to simply say “AI” and expect everything attached to it to go up.

Semis Are Still Being Watched

The semiconductor story remains unresolved.

Monday’s tape was helped by Nvidia pushing back on delay concerns and by optimism ahead of Samsung’s numbers. But the broader headlines are still full of warning signs.

China’s CXMT is reportedly closing the memory gap faster than expected. Samsung’s preliminary numbers matter. The memory cycle is being questioned. Some chip names remain under pressure. And the market is trying to decide whether the AI hardware boom is still accelerating, or whether it is entering a more selective phase.

That is why semis matter so much.

They are no longer just another sector.

They are the physical layer of the AI trade.

If semis stabilize, the market can keep believing the AI buildout has legs. If semis keep leaking, the broader AI narrative gets harder to defend.

Monday was encouraging.

It was not conclusive.

Oil Is No Longer The Main Fear

Oil was slightly higher, with crude up 0.34%.

But the bigger message from the energy tape is that Hormuz is no longer dominating the market the way it was a few weeks ago.

That does not mean the geopolitical risk is gone.

It means the market has moved on, at least for now.

Hormuz traffic appears to be normalizing. Citi reportedly sees Brent falling toward the $60 to $65 range by year-end. Saudi Arabia is discounting oil. OPEC lifted output. Container shipping is now being driven by rates, network reshuffling, and freight volatility more than the immediate Middle East shock.

That matters because oil was the market’s inflation trigger.

When oil is falling or stable, the Fed has more room to breathe. Consumers have more room to breathe. Equities get more room to focus on earnings.

But oil is still not a dead issue.

Geopolitical pricing can come back quickly. And if the oil market begins splitting into different political lanes, where access and pricing depend on which camp a country sits in, then the old globalized oil market becomes more complicated.

For Monday, though, the market treated oil as manageable.

That helped risk appetite.

Gold And Bitcoin Both Rose

Gold rose 0.48%. Bitcoin gained 1.01%.

That gives the tape an interesting flavor.

Usually, a clean risk-on day would see growth stocks higher, volatility lower, and gold softer. But gold also caught a bid. Bitcoin rose too.

That suggests investors are not only chasing risk. They are also keeping some protection on the table.

Bitcoin’s move fits with renewed appetite for speculative assets. Gold’s move fits with a market that still sees macro uncertainty, Fed questions, geopolitics, and currency concerns in the background.

So this was not a “everything is solved” rally.

It was more like:

Risk appetite returned, but nobody is fully relaxed.

That is an important distinction.

The Fed Is Still In The Room

The economic data did not remove the Fed from the conversation.

The services surveys showed continued expansion. Jobs improved. Inflation readings in some areas softened. Waller spoke about forward guidance. The market is still trying to understand how Warsh’s Fed will communicate in the next phase.

That matters because the AI trade depends heavily on the cost of capital.

If rates stay manageable, expensive growth stories are easier to hold. If inflation returns or the Fed turns more hawkish, long-duration assets get harder to justify.

The market wants the best version of the story:

Growth strong enough to support earnings.

Inflation soft enough to keep the Fed calm.

Oil stable enough to avoid another shock.

AI strong enough to justify spending.

Rates low enough to support valuations.

That is a narrow path.

Monday stayed on it.

But the path is still narrow.

The Real Read

Monday was a good day for risk.

Tech led. Communication services led. Consumer cyclicals and financials joined. VIX fell. Bitcoin rose. Gold rose. Oil stayed manageable. The Nasdaq outperformed.

That is constructive.

But the deeper questions remain.

AI is still the engine.

Semis are still being watched.

Hyperscalers are still carrying the story.

Data centers are still running into power, cost, and political constraints.

Oil is calmer, but not irrelevant.

The Fed is quieter, but not gone.

The market is acting like growth took the wheel again.

That may be right.

But the wheel is attached to a vehicle carrying a lot of weight.

The AI trade is still powerful. It is also becoming more complicated. Investors are no longer just asking whether AI matters. They are asking who gets paid, who gets squeezed, and who is spending too much to stay in the race.

That is the real read.

Growth took the wheel again.

Tech led.

Volatility cooled.

But the market is still built around one question:

Can AI keep delivering enough to justify everything riding on it?