Thursday was not a market crash.

It was more interesting than that.

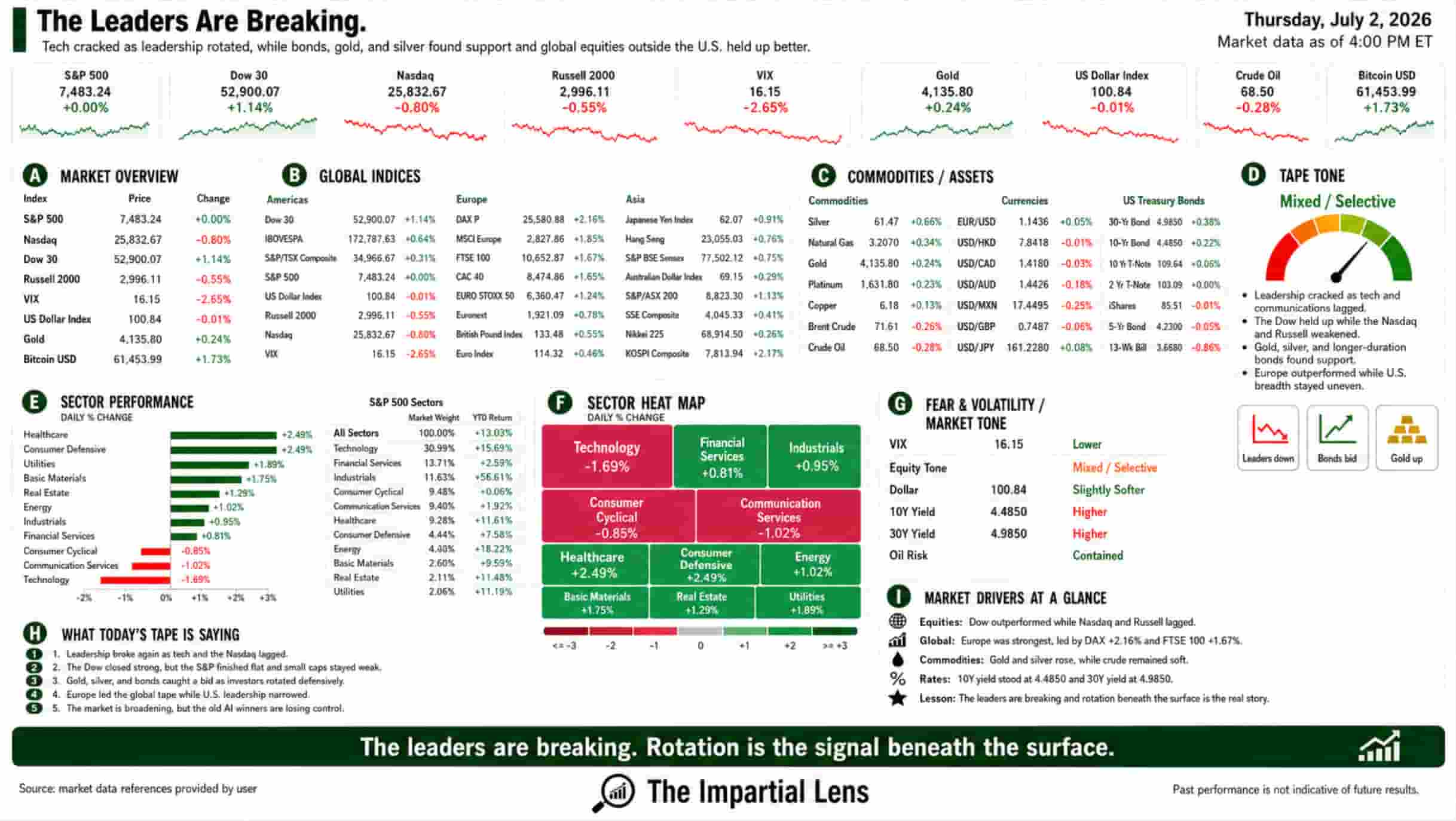

The S&P 500 slipped 0.08%. The Nasdaq fell 0.80%. The Russell 2000 lost 0.55%. But the Dow gained 1.14%, showing that money did not leave the market completely.

It moved.

The VIX fell 2.65% to 16.15, so volatility actually eased. Gold rose 0.24% to $4,135.80. Bitcoin gained 1.73% to $61,453. Crude oil slipped 0.28% to $68.50.

So the surface message was mixed.

Stocks were not broadly weak. Volatility was not screaming. Bitcoin and gold both caught a bid. Oil stayed soft.

But underneath, something important happened:

The leaders kept breaking.

Tech Lost Control Again

The Nasdaq was the weak spot.

That matters because the Nasdaq has been the market’s engine. When technology leads, the broader market can ignore a lot. It can ignore oil noise. It can ignore geopolitical headlines. It can even ignore weak macro data for a while.

But when tech starts leaking, the whole structure looks different.

Technology fell 1.69%. Communication services dropped 1.02%. Consumer cyclical slipped 0.85%. The high-beta growth trade was not in control.

That is the opposite of what bulls wanted after Tuesday’s tech-led bounce.

The market has been trying to decide whether last week’s AI wobble was just a shakeout or the beginning of a larger leadership problem. Thursday gave us another warning that this is not fully repaired.

The AI trade is still alive.

But it is no longer moving as one clean force.

The Momentum Trade Is Cracking

The headlines keep saying the same thing in different ways.

Momentum is under pressure. The AI memory trade is unraveling. The leaders are breaking. Leveraged ETF stress is not just noise. Korea’s AI-linked trading mania is still flashing warning signs. Data-center economics are being questioned. Blackstone reportedly pulled out of a massive data-center project. OpenAI, Anthropic, Meta, memory, chips, private credit, and hyperscaler capex are all being dragged into the same conversation.

That conversation is simple:

The market is no longer willing to blindly buy every AI winner.

That is the shift.

For much of the year, investors treated AI as a single trade. If it touched compute, chips, memory, power, data centers, software, or cloud, it got a bid.

Now the market is asking harder questions.

Who owns the economics?

Who is overbuilding?

Who is spending too much?

Who is exposed to lower inference costs?

Who benefits if compute becomes abundant instead of scarce?

Who is just riding the theme without real pricing power?

This is not the end of AI.

It is the end of the easy version.

Weak Jobs Changed The Rate Story

The macro data added another layer.

The jobs report missed expectations, with downward revisions. The unemployment rate moved lower, but that came alongside a drop in labor force participation. Initial and continuing claims were little changed.

That is not a clean “strong labor market” signal.

It is also not a clean recession signal.

It is messy.

And messy matters because the Fed is already operating without much forward guidance. Markets are trying to guess whether weak data signals rate relief or sticky inflation, and AI-related cost pressures keep the Fed cautious.

Front-end yields declined after the jobs miss. That helped bonds. It also helped explain why the VIX cooled rather than spiked.

But weaker jobs do not automatically save equities.

If labor weakens slowly, bulls can call it a soft landing.

If it weakens faster, earnings become the next problem.

That is the narrow path.

The market wants data weak enough to help rates, but not weak enough to hurt profits.

That is a very specific wish.

Bonds, Bitcoin, And Bullion Caught A Bid

One of the more interesting parts of Thursday was the cross-asset message.

Bonds were bid. Gold rose. Bitcoin rose.

That tells us investors were not just hiding in cash.

They were rotating into assets that benefit from a different story: softer growth, softer yields, and a market that is no longer fully confident in the old leadership.

Bitcoin’s strength was especially notable because tech was weak. That suggests crypto is trading more independently than it did earlier in the year. It may be picking up flows from investors looking for alternative risk exposure while the AI trade wobbles.

Gold’s strength also mattered. It did not explode, but it caught a bid while oil stayed soft and tech sold off. That fits the idea of a market that is not panicking, but is hedging.

Not fear.

Preparation.

Oil Stayed Soft Despite Geopolitical Noise

Crude fell again.

That should help the inflation backdrop. Lower oil reduces consumer pressure, shipping costs, and central-bank anxiety.

But the geopolitical story remains unstable.

Iran rejected direct Doha talks, while U.S. officials continued to talk about options. Vance warned that the U.S. still has choices if diplomacy fails. Europe appears increasingly resigned to some form of Hormuz fee arrangement. Iran’s oil is reportedly running into buyer problems. Tankers and energy transit remain part of the story.

So oil is calm, but the politics are not.

This has been a recurring theme:

Markets price relief faster than reality delivers it.

That does not mean the market is wrong.

It means the market is assuming the worst case stays contained.

The Real Read

Thursday’s tape was not about panic.

It was about leadership.

The Dow rallied. Bonds caught a bid. Gold rose. Bitcoin rose. Volatility fell. Oil stayed soft.

Those are not crash conditions.

But the Nasdaq fell, technology lagged, and the AI momentum trade continued to lose its clean shape.

That is the real story.

The market is shifting from one regime to another.

The first regime was simple:

Buy AI. Buy semis. Buy memory. Buy hyperscalers. Buy anything tied to compute scarcity.

The new regime is harder:

Buy only the companies that can prove they capture the economics.

That is a very different market.

It means leadership narrows, rotates, and gets questioned more often. It means rallies can still happen, but they may be sharper and less durable. It means dispersion matters more than index direction.

And it means the headline market can look calm while the structure underneath changes quickly.

The Dow held up.

Bonds, Bitcoin, and gold caught a bid.

Oil stayed soft.

But the Nasdaq slipped again.

The leaders are no longer carrying the market in the same way.

AI is still the story.

But now the market wants proof.