Thursday gave the market exactly what it wanted.

A relief bounce.

After two days of oil shocks, Iran headlines, rising volatility, and pressure under the surface, the tape finally found its footing again.

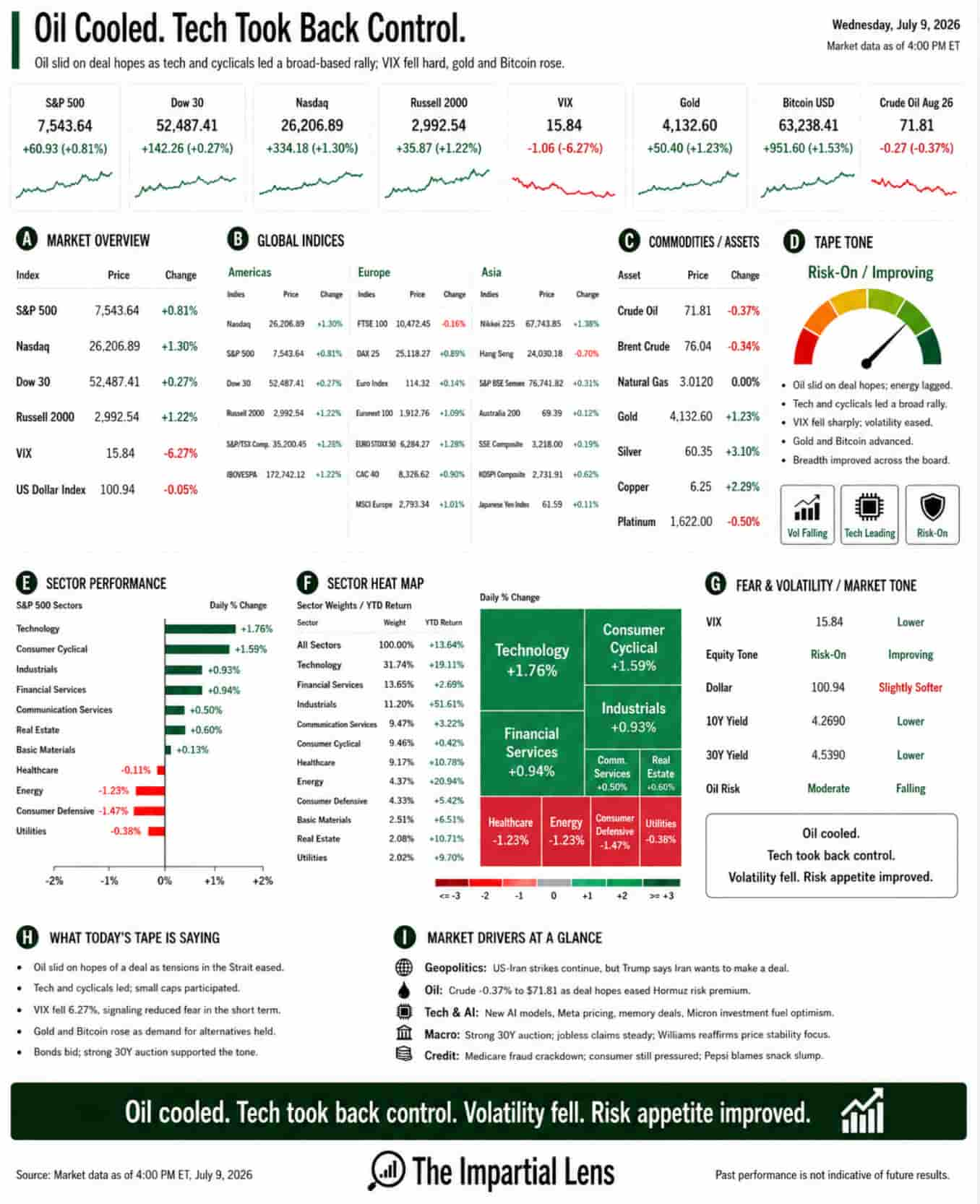

The S&P 500 rose 0.81%. The Dow gained 0.27%. The Nasdaq jumped 1.30%. The Russell 2000 climbed 1.22%.

Volatility cooled hard, with the VIX falling 6.27% to 15.84.

Gold rose 1.23%. Bitcoin gained 1.53%. Crude oil slipped 0.37% to $71.81.

That is a much cleaner tape.

But it was not clean because the world got calmer.

It was clean because markets decided to look through the chaos.

AI Beat The War Tape

The strangest part of Thursday was not that stocks rose.

It was why they rose.

The geopolitical headlines were still ugly. U.S. and Iranian strikes continued. Iran reportedly fired missiles toward Kuwait, Bahrain, Qatar, and Jordan after U.S. strikes on Iranian targets. There were reports of explosions in southern Iran. The region was not quiet.

And yet stocks rallied.

That tells us something important.

The market did not forget about the war risk.

It simply decided that, for now, the AI story mattered more.

That is why the headline of the day was not just “stocks up.”

It was:

AI anticipation trumped Hormuz fear.

Tech led. Momentum improved. Memory headlines helped. Meta reportedly signed long-term supply agreements for memory, networking gear, and flash storage. Micron is planning a huge investment through 2035. Meta unveiled a paid AI model with aggressive pricing. Starbucks is using AI to build software that could replace systems it currently buys from Microsoft and IBM.

The message was clear:

AI is no longer just a chip story.

It is becoming a cost story, a software story, a productivity story, a capex story, and a supply-chain story.

That is why the market keeps coming back to it.

Tech Reclaimed Leadership

The sector tape confirmed the move.

Technology rose 1.76%. Consumer cyclical gained 1.59%. Financial services added 0.94%. Industrials rose 0.93%. Communication services gained 0.50%.

That is the kind of leadership bulls wanted to see.

It was not just one sector carrying the tape. Growth led, cyclicals participated, small caps rose, and volatility fell.

That is a better setup than Wednesday.

The Nasdaq led, but the Russell also joined. That matters because a rally led only by mega-cap tech is useful, but fragile. A rally where small caps also participate has more breadth.

Thursday had some of that.

Not perfect breadth.

But better breadth.

Oil-cooled, And That Changed The Mood

The other important shift was oil.

Crude slipped 0.37% after jumping earlier in the week.

That mattered because oil has been the market’s fastest inflation signal. When crude rises because of Hormuz risk, the market immediately has to price shipping stress, insurance costs, energy inflation, and less room for the Fed to be friendly.

When crude cools, equities get oxygen.

That is what happened on Thursday.

The war headlines did not disappear. But oil stopped rising. That was enough for markets to breathe.

This is the key point:

Markets do not need the geopolitical problem solved every day.

Sometimes, they only need the worst-case scenario to stop getting worse.

Thursday was one of those days.

The Bond Market Helped Too

Bonds also mattered.

A strong 30-year auction showed solid demand, including strong foreign participation. That helped the tone because it suggested investors were still willing to buy duration even with geopolitical headlines active.

That is important.

If oil risk rises and bond yields rise at the same time, equities have a problem.

But if oil cools and bonds are bid, markets get room to focus on earnings and AI again.

That is exactly what happened.

The Fed is still there. Williams reaffirmed the commitment to price stability. Inflation is not solved. But the market did not see a fresh rates shock on Thursday.

No new rate shock.

Oil cooled.

Tech rallied.

That was enough.

The Rotation Was Not Perfect

The rally still had limits.

Healthcare fell 0.11%. Energy dropped 1.23%. Consumer defensive lost 1.47%. Utilities slipped 0.38%.

That tells us the move was not defensive.

It was risk appetite coming back.

Investors sold the groups that had held up during the stress and moved back toward technology, cyclicals, financials, and small caps.

That is constructive if it continues.

But it also means the market is still choosing growth over protection.

That can work while oil is calm.

It becomes harder if Hormuz heats up again.

AI Is Still Carrying A Lot Of Weight

The big question remains the same:

How much can AI carry?

Thursday showed that the market still wants to believe.

New models. Memory demand. Meta’s paid AI model. Micron investment. Supply agreements. Software replacement. Semiconductor positioning. Momentum repair.

All of it helped.

But the bigger issue has not gone away.

AI is carrying more than just earnings expectations. It is carrying sentiment, capex assumptions, power demand, productivity hopes, and index leadership.

That is a lot of weight.

If AI keeps delivering, the market can keep pushing through messy headlines.

If AI stumbles, the market loses its main excuse to ignore the rest of the world.

That is the tension.

The Real Read

Thursday was a relief rally.

A real one.

Stocks rose. Tech led. Small caps joined. VIX fell. Gold and Bitcoin rose. Oil cooled. Bonds helped.

That is a better tape.

But it was not an all-clear.

The geopolitical backdrop is still unstable. U.S. and Iran strikes continued. Hormuz risk has not disappeared. The Fed is still focused on inflation. Consumer data remains uneven. And AI is still doing a lot of the market’s heavy lifting.

The market’s message was not “everything is fine.”

It was more specific:

Oil stopped rising.

AI stayed strong.

So investors bought risk again.

That is different from safety.

Oil cooled.

Tech took back control.

Volatility fell.

But the market is still walking a narrow path:

AI has to keep working, and Hormuz has to stop getting worse.