Wednesday gave the market a green close.

But do not confuse green with healthy.

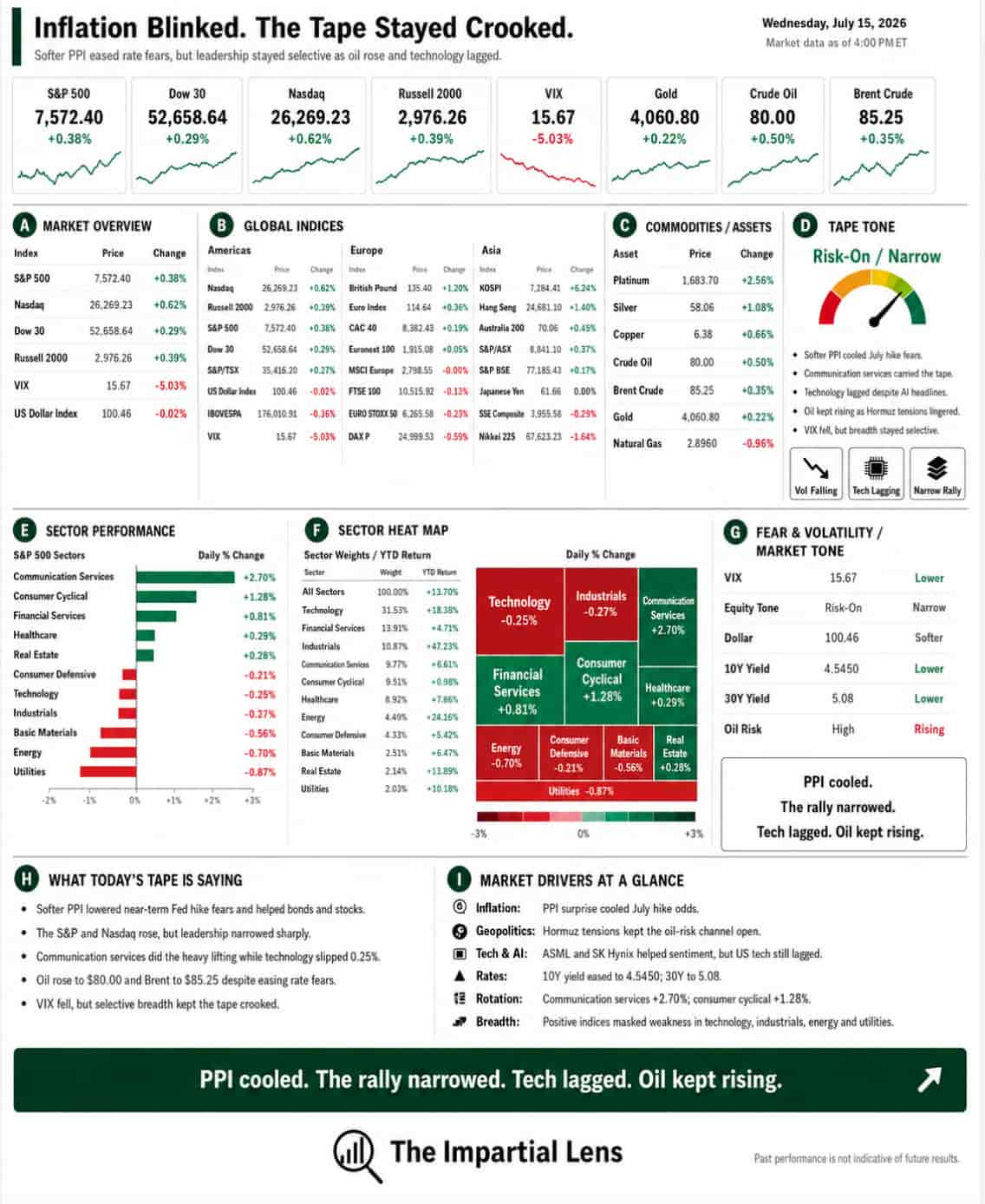

The S&P 500 rose 0.38%. The Dow gained 0.29%. The Nasdaq climbed 0.62%. The Russell 2000 added 0.39%.

The VIX fell 5.03% to 15.67.

Gold rose 0.22%. Silver gained 1.08%. Platinum jumped 2.56%. Copper added 0.66%.

Crude oil rose 0.50% to $80.00. Brent gained 0.35% to $85.25.

The dollar slipped 0.02% to 100.46. Treasury yields moved lower, with the 10-year near 4.545% and the 30-year around 5.08%.

Underneath, it looked like the market had put on a clean shirt over a bruised body.

Benign-Flation Bought The Market A Pass

The main relief came from producer prices.

Headline PPI reportedly fell 0.3% month over month, the sharpest drop since the COVID period. That was enough to knock a July rate hike off the table and revive the familiar reflex:

Softer inflation.

Lower yields.

Weaker dollar.

Higher risk assets.

The market did not hear “mission accomplished.”

Fed Chair Warsh warned against cherry-picking one friendly report and kept the higher-for-longer threat alive. But markets trade the next move before they debate the endgame.

For one session, inflation blinked.

That permitted stocks to rally.

War Screamed. Oil Barely Flinched.

The geopolitical tape was ugly.

US strikes continued. The IRGC vowed that not a drop of oil or gas would leave the region. Trump returned to the language of a full blockade. Maritime officials warned ships to avoid Hormuz.

And crude rose only 0.50%.

The headlines screamed shortage.

The oil market shrugged.

For now.

US crude production reportedly hit a record high. Russian refining weakness may now matter more to physical supply than the latest threat from Tehran. Ships are still moving, even if nervously.

The market has not stopped caring about war.

It has stopped pricing every threat as if the barrels are already gone.

That is not peace.

It is skepticism.

AI Got Better Headlines Than Price Action

ASML raised its outlook.

SK Hynix rebounded.

Alibaba’s Qwen is reportedly heading into Apple devices in China.

South Korea’s KOSPI surged 6.24%. The Hang Seng gained 1.40%.

That should have been rocket fuel for US technology.

Instead, the technology sector fell 0.25%.

The Nasdaq rose, but tech did not lead.

Communication services surged 2.70%. Consumer cyclicals gained 1.28%. Financials added 0.81%.

Meanwhile, industrials fell 0.27%. Energy lost 0.70%. Basic materials declined 0.56%. Utilities dropped 0.87%.

The index wore green.

The plumbing looked jaundiced.

The AI Trade Is Meeting The Electric Bill

The AI story is no longer just chips, models, and heroic capex slides.

It is now debt.

Power.

Permits.

Transmission lines.

And politicians are deciding where data centers are allowed to exist.

The largest US power grid is reportedly 6.8 gigawatts short of what it needs for future reliability. Pennsylvania is increasing oversight. New York has imposed a one-year ban on new data centers. SpaceX bonds are wobbling. Hyperscaler debt is becoming a conversation.

The market spent two years pricing AI as if electricity, credit, and political tolerance were infinite.

They are not.

The buildout may still accelerate.

But the bill is arriving before the profits have fully shown up.

That is why good semiconductor news can coexist with weak technology performance.

The story is alive.

The financing is getting heavier.

Breadth Was The Buzzkill

Wednesday was not a broad risk-on surge.

It was a selective rescue.

Communication services did the heavy lifting. Consumer cyclicals helped. Financials joined.

But technology, industrials, energy, materials, consumer defensives, and utilities all finished lower.

That is not a market firing on all cylinders.

That is a market limping forward because a few strong groups dragged the indexes across the line.

The VIX fell.

The indexes rose.

But the sector map looked like an argument, not a celebration.

The Real Read

Wednesday was a good day.

Just not a clean one.

Inflation cooled.

Yields eased.

The dollar softened.

Volatility fell.

Oil refused to panic.

Stocks finished higher.

That is the bullish case.

The bearish case is hiding in plain sight.

Technology fell despite strong AI headlines.

Breadth was poor.

The AI buildout is colliding with debt, power shortages, regulation, and the rising cost of making the dream physical.

The market’s message was blunt:

Inflation gave investors permission to buy.

War failed to take that permission away.

But AI no longer gets to wave a glossy slide deck and skip the invoice.

The boom is still real.

So is the bill.

And the tape is finally starting to read the fine print.

The Impartial Lens provides market and geopolitical commentary for educational purposes. It is not investment advice.