Tuesday should have been an easy risk-on day.

Inflation came in softer than expected. Treasury yields fell. The dollar weakened. The VIX dropped. Big banks delivered solid earnings.

And stocks rose.

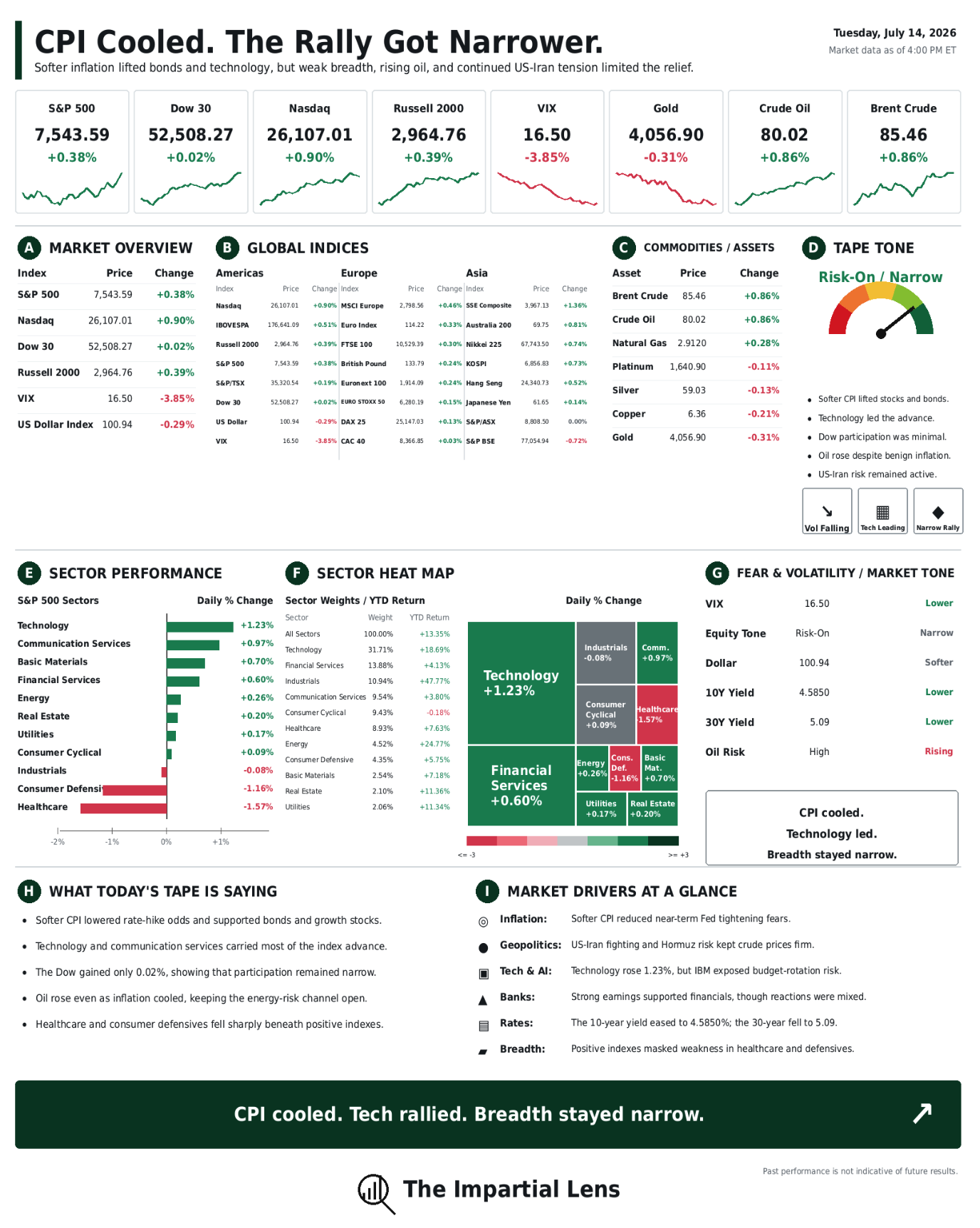

The S&P 500 gained 0.38%. The Nasdaq climbed 0.90%. The Russell 2000 added 0.39%.

But the Dow rose just 0.02%.

That tiny gain told the real story.

The market got a friendlier inflation print, but not a broad rally.

It got another technology-led rescue.

The Rally Had One Engine

Technology rose 1.23%. Communication services gained 0.97%. Financials added 0.60%.

That was enough to lift the indexes.

But beneath the surface, the tape was uneven.

Industrials fell 0.08%. Consumer defensives dropped 1.16%. Healthcare sank 1.57%. Consumer cyclicals managed only a 0.09% gain.

This was not investors buying the economy.

It was investors buying the parts of the market that benefit most when yields fall.

The Nasdaq led because the bond market gave growth stocks breathing room.

The rest of the market mostly watched.

CPI Bought Time, Not Victory

The softer June CPI report reduced fears that the Federal Reserve would need to tighten again soon.

The reaction was immediate.

The 10-year Treasury yield fell to 4.585%. The 30-year eased to 5.09%. The dollar index slipped 0.29% to 100.94. The VIX fell 3.85% to 16.50.

That is exactly the combination growth stocks wanted.

But Fed Chair Kevin Warsh refused to declare victory.

One benign report does not erase the inflation problem.

Markets trimmed rate-hike odds, while the Fed still has to consider oil, tariffs, wages, and financial conditions.

Tuesday’s CPI print bought the market time.

It did not remove the next inflation shock.

War Stayed Hot. Oil Stayed Bid.

That shock could still come from energy.

US-Iran strikes continued. The IRGC threatened that not a drop of oil or gas would leave the region. The Trump administration returned to the idea of a full blockade of Iranian ports and dropped the proposed 20% Hormuz transit fee.

Oil kept rising.

West Texas Intermediate gained 0.86% to $80.02. Brent rose 0.86% to $85.46.

That created the day’s central contradiction.

Backward-looking inflation cooled.

Forward-looking energy risk did not.

Hormuz does not need to be fully closed to matter. Tanker attacks, higher insurance costs, military escorts, and disrupted shipping schedules can all push costs higher.

The market chose to focus on CPI.

Oil kept reminding it that the story is not finished.

Banks Passed. IBM Failed.

The big banks broadly delivered.

Trading revenue, investment banking, and consumer activity held up better than feared. Financials rose 0.60%.

But the stock reactions were mixed, suggesting expectations were already high.

IBM provided the sharper signal.

Its preliminary results disappointed as investors focused on capital-spending pressure and the possibility that corporate technology budgets are being redirected toward AI infrastructure.

That is the uncomfortable side of the AI boom.

AI spending is not all new money.

Some of it is being pulled away from traditional software, consulting, and enterprise systems.

The market is beginning to separate the companies receiving the AI budget from those losing it.

Breadth Is The Tell

A healthy rally usually expands.

More sectors participate. Cyclicals strengthen. Small caps confirm the move. The average stock keeps pace with the index.

Tuesday did not deliver that.

The S&P rose.

The Nasdaq led.

But the Dow barely moved, defensives sold off, healthcare fell hard and industrials slipped.

The index can keep rising while fewer stocks do the work.

But the more concentrated leadership becomes, the more damage one earnings miss, AI disappointment or rates shock can cause.

Tuesday was positive.

It was not robust.

AI Still Needs Money And Power

The AI trade recovered, but the infrastructure problem is getting larger.

Hyperscalers need enormous amounts of debt to fund data centres, networking, chips and power. Credit investors are already questioning how easily another wave of issuance can be absorbed.

At the same time, PJM warned that its power system is 6.8 gigawatts short of what may be needed to ensure reliability in 2028 as data-centre demand surges.

AI still has momentum.

But momentum now depends on affordable financing, available electricity and proof that future profits justify today’s spending.

Lower yields helped for one day.

They did not solve the funding equation.

The Real Read

Tuesday gave investors almost everything they asked for.

Softer CPI.

Lower yields.

A weaker dollar.

Falling volatility.

Solid bank earnings.

And yet the rally still narrowed around technology.

That is the message.

Inflation relief remains powerful enough to lift the indexes.

But not powerful enough to make the whole market participate.

Meanwhile, oil is rising, war risk is active, and AI is becoming more dependent on debt and power.

CPI cooled.

Tech rallied.

The indexes rose.

But the market did not broaden.

It concentrated.

The Impartial Lens provides market and geopolitical commentary for educational purposes. It is not investment advice.