The market did not collapse. It rotated. Financials caught a bid, tech lost momentum, crypto weakened, and the AI trade faced another reminder that earnings bubbles are still bubbles.

Thursday was not a disaster.

But it was not clean either.

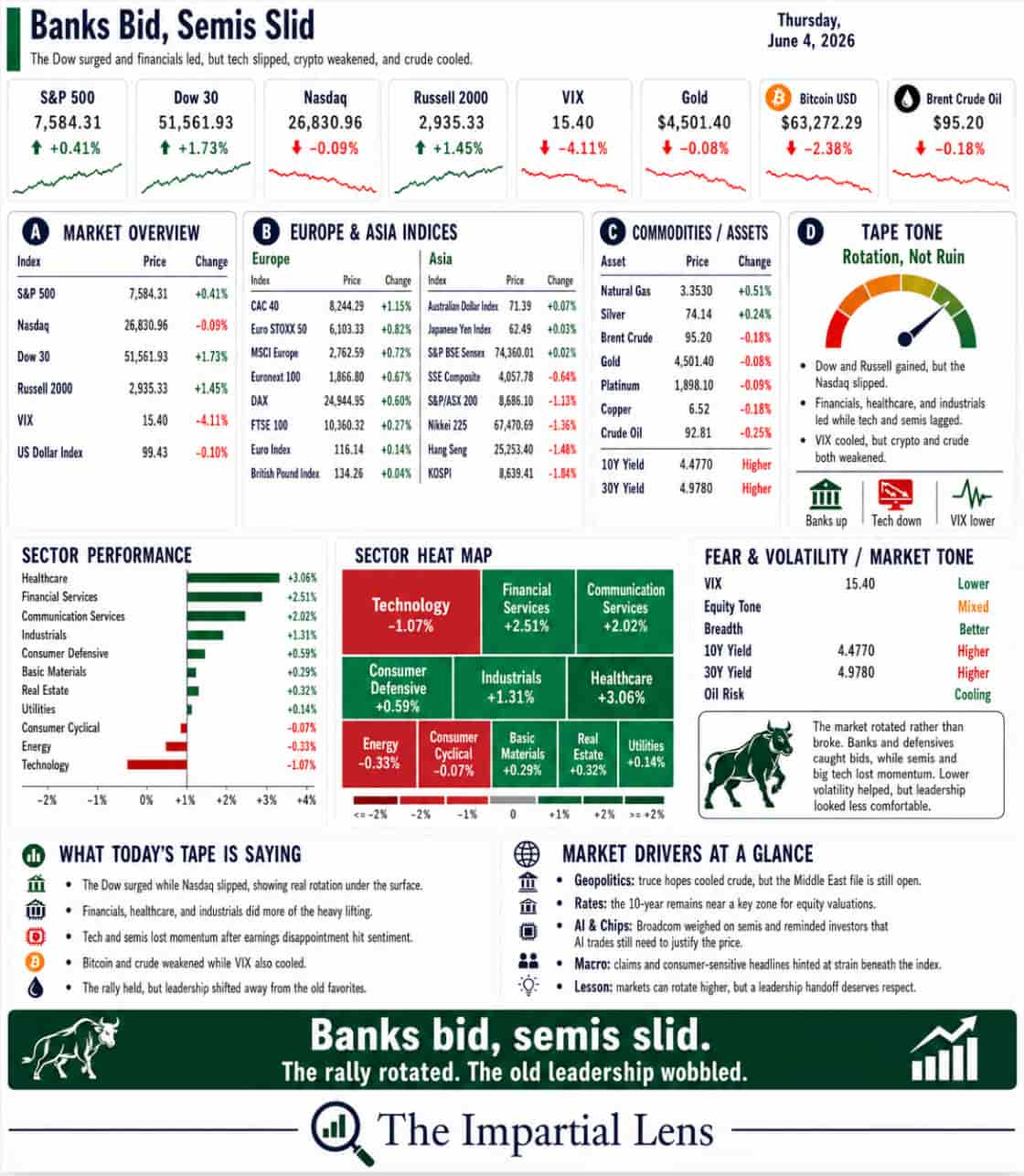

The Dow rose sharply. Financials were strong. Healthcare and industrials helped. The S&P finished higher. Small caps gained. Volatility fell.

But the Nasdaq slipped. Technology fell. Semis were hit. Crypto weakened again. Crude pulled back. And beneath the surface, the market looked less like a smooth rally and more like a rotation away from crowded winners.

That matters.

When everything is going up together, investors call it confidence.

When some sectors rise while the old leaders start slipping, investors call it “healthy rotation.”

Sometimes that is true.

Sometimes it is the market quietly admitting that yesterday’s favorite trade has become too crowded.

Thursday looked like a little of both.

The Dashboard Says: Rotation, Not Celebration

The headline numbers were mixed.

The Dow gained about 1.73%.

The S&P 500 rose 0.41%.

The Russell 2000 added 1.45%.

The Nasdaq slipped 0.09%.

The VIX fell more than 4%.

Gold was roughly flat.

Bitcoin fell more than 2%.

Brent crude slipped about 0.18% to $92:20 a Barrell

So, the tape was not risk-off.

But it was not the usual AI-led party either.

The sector board tells the real story.

Financial Services gained 2.51%. Healthcare rose 3.06%. Industrials added 1.31%. Communication Services rose 2.02%. Consumer Defensive gained 0.59%.

Technology fell 1.07%.

That is the key.

The market went up without tech leading.

That is useful.

A market that can rise without tech is broader than a market that needs Nvidia, Broadcom, and semis to do all the work. But it also tells us something else: the leadership trade is starting to wobble.

Semis Finally Got Hit

Broadcom weighed on tech after its AI semiconductor revenue forecast disappointed. That followed the same theme we have been tracking all week: AI is still powerful, but the market is starting to care about the numbers.

For months, investors treated AI like a magic word.

Say “AI,” stocks go up.

Now the market is becoming more selective.

Broadcom can still be a great business and still disappoint a market that had already priced in perfection. That is the problem with momentum trades. They do not merely need good news. They need better-than-impossible news.

The AI trade is not dead.

But the easy phase may be ending.

The story is shifting from:

“AI will change everything.”

To:

“How much revenue, how much margin, how much capex, how much power, how much debt, and how soon?”

That is a very different conversation.

The Bond Market Still Holds the Key

The 10-year Treasury yield remains near the key zone investors are watching. The market has become very sensitive to the idea that yields above roughly 4.5% become a valuation problem.

This is the part equity investors do not like.

Higher yields make expensive stocks harder to justify. They also make cash and bonds more competitive. They pressure housing, private credit, corporate borrowing, government deficits, and the long-duration growth trade.

That includes AI.

Especially AI.

AI is capital intensive. It needs chips, data centers, electricity, cooling, water, financing, and political permission. The more physical the AI buildout becomes, the more interest rates matter.

A software dream can ignore rates for a while.

An infrastructure boom cannot.

The Consumer Is Still Sending Warnings

Several headlines pointed to consumer strain.

Beer demand is weakening. Sleep Number is facing bankruptcy concerns. Five Below warned that the tax-refund boost is fading. Home sellers are pulling listings as buyers balk at high prices. Ford sales fell sharply. Jobless claims jumped, and tech firms announced the most job cuts in two years.

That does not mean the consumer is dead.

But it does mean the market should stop pretending the consumer is bulletproof.

The stock market can make new highs while households quietly tighten spending. That happens more often than people think.

The index is not the economy.

The index is a collection of large companies, many of which can still protect margins, cut costs, raise prices, automate labor, and borrow at scale.

Ordinary households do not have that menu.

They get higher insurance, higher food, higher energy, higher rent, higher rates, and then a cheerful economist explaining that the aggregate data looks fine.

Geopolitics Cooled, But Did Not Disappear

Trump softened the Iran red line, saying there was “no reason” to retrieve Iran’s nuclear “dust” if it was effectively entombed. He also downplayed Iranian attacks on U.S. bases, saying they were “slightly provoked.”

That helped the market avoid a larger geopolitical panic.

But this is not resolution.

The Middle East file is still open. Hormuz risk is still open. Iran-China coordination is still a factor. Gulf states are discussing bypass pipelines. The U.S. military is helping ships cross Hormuz. Ukraine aid is moving through Congress. Europe is worrying about energy costs and industrial strain.

This is why geopolitics remains part of the market structure.

It affects energy.

Energy affects inflation.

Inflation affects bonds.

Bonds affect valuations.

Valuations affect tech.

Tech affects the index.

The market may want the story to go away.

It has not gone away.

Private Credit Smoke Keeps Building

Blackstone’s private credit fund joined peers in gating redemptions after a surge in withdrawal requests.

That matters.

Private credit has been one of the great hiding places of the cycle. It smooths volatility. It avoids daily pricing. It makes investors feel calmer than they might feel if everything were marked in public markets every day.

But when investors start asking for their money back and funds begin limiting withdrawals, the calm starts to look less calm.

This is not a crisis call.

But it is another reminder that the glossy surface of the market may be hiding stress beneath.

The public market says: look at the index.

Private credit says: please form an orderly line.

The Real Read

Thursday was mixed, not broken.

The Dow rallied.

Financials surged.

Healthcare led.

Small caps participated.

Volatility fell.

Crude cooled.

But technology slipped.

Semis were pressured.

Bitcoin weakened.

Consumer warnings grew louder.

Private credit stress kept building.

And the AI trade looked less invincible.

The lesson is clear:

A market can rotate higher and still become more fragile underneath.

Rotation is healthy when new leadership broadens the rally.

Rotation is less healthy when it happens because the old leadership is finally too crowded, too expensive, or too exposed to disappointment.

Thursday gave us both possibilities.

For now, the tape is still holding.

But the market is becoming more selective.

That is the important change.

The rally is no longer just “buy AI and relax.”

It is becoming a test of who has real earnings, real cash flow, real balance-sheet strength, and real pricing power.

That is a healthier question.

But it is also a harder one.