The market finally remembered that strong data is not always bullish. When inflation is still hanging around, good economic news can mean higher yields, fewer cuts, and less room for mistakes.

Wednesday broke the spell.

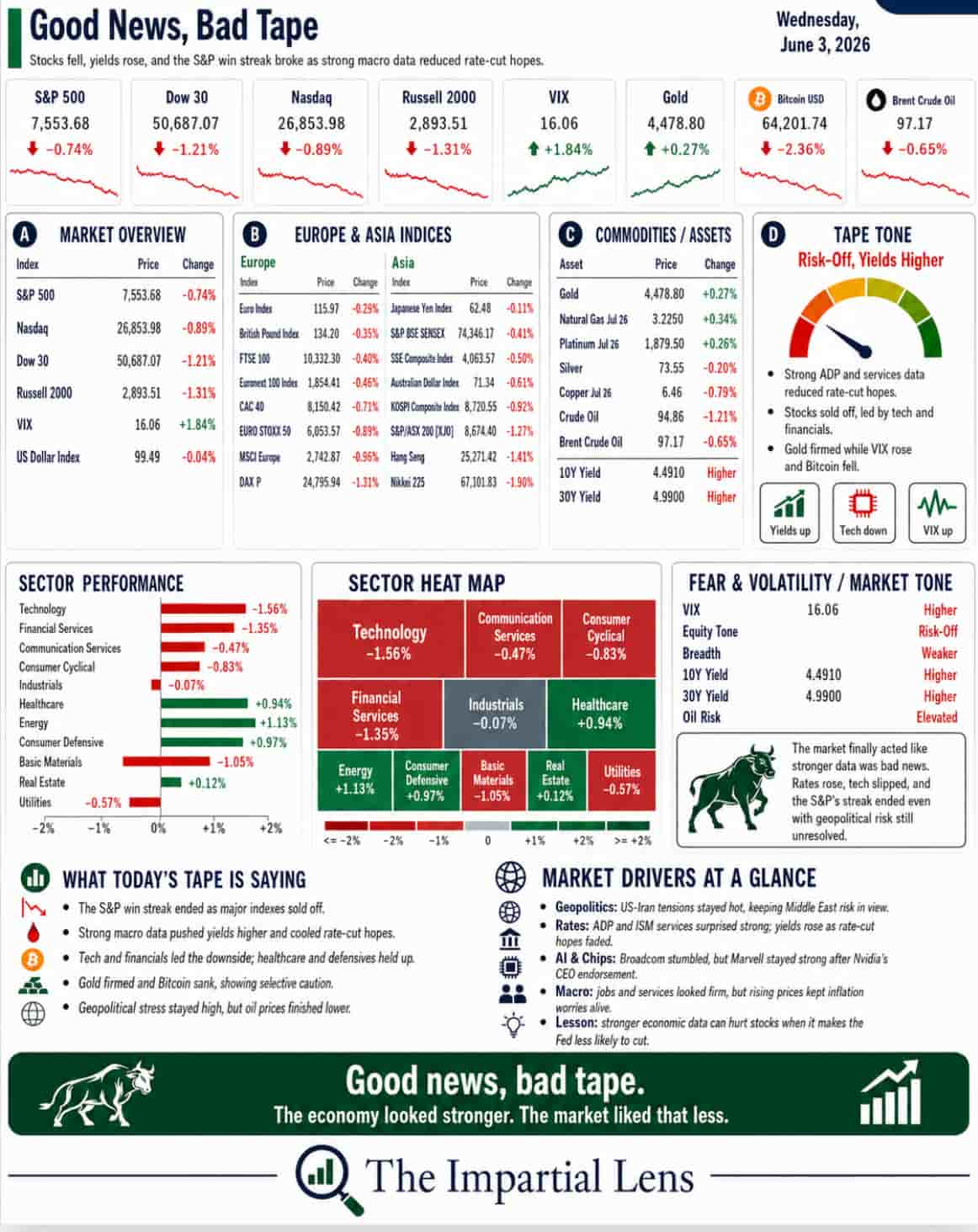

After a historic run, stocks finally went down. The S&P’s winning streak ended. Bonds sold off. Oil rose. Bitcoin stayed weak. And the Middle East moved from background risk back into the center of the tape.

This was not a panic.

But it was a warning.

The market has spent the last few weeks acting as if every problem could be managed: Iran, oil, inflation, bonds, AI spending, the consumer, private credit, and geopolitics.

On Wednesday, several of those problems showed up at the same time.

That is why the tape felt different.

The market did not fall because the economy looked terrible.

It fell because the economy looked strong enough to keep inflation alive.

And in this environment, that is not always good news.

The Dashboard Says: The Win Streak Finally Broke

The headline was simple: stocks went down.

But the more important detail is that bonds went down too (yields up)

That matters.

When stocks fall, and bonds rally, investors can tell themselves the old playbook still works. Risk comes off, safety catches a bid, and the system absorbs the shock.

But when stocks and bonds fall together, the message is different.

That usually means the market is worried about inflation, supply shocks, or policy pressure.

Wednesday had all three.

Oil climbed after another round of U.S.-Iran escalation. Yields moved higher after stronger macro data. Stocks finally gave back ground after a run that had become too comfortable.

The market was not broken.

But the cushion looked thinner.

Good News Became Bad News Again

The macro data was not weak.

That was the problem.

ADP reported the strongest job gains in 16 months. ISM Services beat expectations. The services side of the economy still had momentum. But prices remained elevated.

That is the uncomfortable mix.

Growth looked better.

Inflation pressure did not disappear.

For investors, that means the Fed has less room to ride in with rate cuts. The economy may still be moving, but if prices are still sticky, central banks cannot simply declare victory and start easing.

This is the simple lesson:

Good news is good news when inflation is falling.

Good news becomes bad news when inflation is still too high.

That is where the market is now.

Strong data keeps the economy alive.

But it also keeps the Fed cautious.

And a cautious Fed is not what an expensive, AI-heavy, momentum-driven market wants to hear.

Geopolitics Is Not a Side Story

The Middle East headlines got worse.

The U.S. struck Iran’s Qeshm Island. Iran responded with missiles and drones targeting U.S. bases across the Gulf. Kuwait International Airport was reportedly hit, with casualties. Explosions and sirens were reported across the region.

Then Iran issued a four-stage proposal for a deal with the U.S.

That is the world we are in now.

Missiles in the morning.

Peace proposal by lunch.

Markets are expected to price both with a straight face.

This is why geopolitics matters to the tape. It is not just noise. It is a direct transmission channel into inflation, oil, shipping, defense spending, and rates.

Hormuz affects oil.

Oil affects inflation.

Inflation affects bonds.

Bonds affect valuations.

Valuations affect tech.

Tech affects the index.

That chain is still intact.

And Wednesday reminded investors that it can tighten quickly.

Oil Is Back in the Conversation

Oil rose as geopolitical risk increased.

That makes sense.

When U.S. and Iranian forces are exchanging strikes, energy traders do not need much imagination. The Gulf is too important. Hormuz is too important. Supply routes are too important.

But oil matters for more than oil companies.

Oil is a tax on consumers.

It raises transport costs. It pressures margins. It feeds inflation expectations. It makes central banks more cautious. It makes politicians more nervous.

That is why rising oil can turn into a market problem even if the stock market wants to ignore it.

The market can tolerate expensive oil for a while.

It has a harder time tolerating expensive oil, rising yields, sticky inflation, and geopolitical uncertainty at the same time.

That was the issue on Wednesday.

AI Is Still the Engine, But the Bill Is Arriving

AI did not disappear.

But the story got more complicated.

Broadcom fell after its AI chip revenue forecast missed expectations. Uber introduced a cap on AI coding-tool spending after a budget blowout. Bain warned that AI cost savings are falling short of expectations. Private-market questions around AI funding and credit exposure are growing.

This does not mean AI is fake.

It means the market is moving from the dream phase to the invoice phase.

The dream phase was easy:

AI will change everything.

The invoice phase is harder:

Who pays for the chips?

Who pays for the power?

Who pays for the data centers?

Who pays for the software subscriptions?

Who pays for the debt?

And when does the productivity show up?

That is the real AI question now.

The market still loves the story.

But it is starting to ask what the story costs.

And higher yields make that question more important.

Private Markets Are No Longer Invisible

There was another quiet warning under the surface: private markets.

Reports said prosecutors are looking into valuation issues in private credit. A major private equity fund gated investors. That matters because private markets have been one of the great “smoothers” of this cycle.

Public markets move every day.

Private markets often pretend not to.

That works until liquidity matters.

If private credit and private equity valuations start getting questioned, then one of the hidden pressure points in the system becomes more visible.

It does not mean a crisis is here.

But it does mean the list of things the market has to ignore is getting longer.

The Real Read

Wednesday was not a collapse.

It was a reality check.

Stocks fell.

Bonds fell.

Oil rose.

Yields rose.

The S&P win streak ended.

Middle East risk escalated.

Strong macro data reduced the case for cuts.

AI showed more cost pressure.

Private markets started looking less invisible.

The market has been pricing a friendly world.

AI keeps working.

Oil stays contained.

The Fed eventually cuts.

Consumers keep spending.

Bonds behave.

Geopolitics stays manageable.

Private credit stays quiet.

And every dip gets bought.

Wednesday questioned that story.

Not completely.

But enough.

The lesson is clear:

Strong data is only bullish when inflation is under control.

If strong data pushes yields higher, keeps the Fed cautious, and arrives at the same time oil is rising, then the market has a problem.

For now, this looks like a pause, not a break.

But the air changed.

The market finally remembered that stocks can go down.

And when bonds fall with them, there is less cushion than people think.