China’s Kimi K3 rattled the AI trade, Asian markets convulsed, and the widening Gulf war sent crude up more than 4%. Friday was not one isolated selloff. It was several crowded assumptions breaking at once.

Friday, July 17, 2026

The market ended the week with two uncomfortable questions.

What if America’s AI lead is less secure than investors assumed?

And what if the war with Iran is moving from controlled military exchanges toward a broader assault on regional infrastructure?

Friday did not provide definitive answers. Markets rarely wait for those.

Technology sold off, Asian equities buckled, volatility jumped, and oil posted its largest gain since the war began.

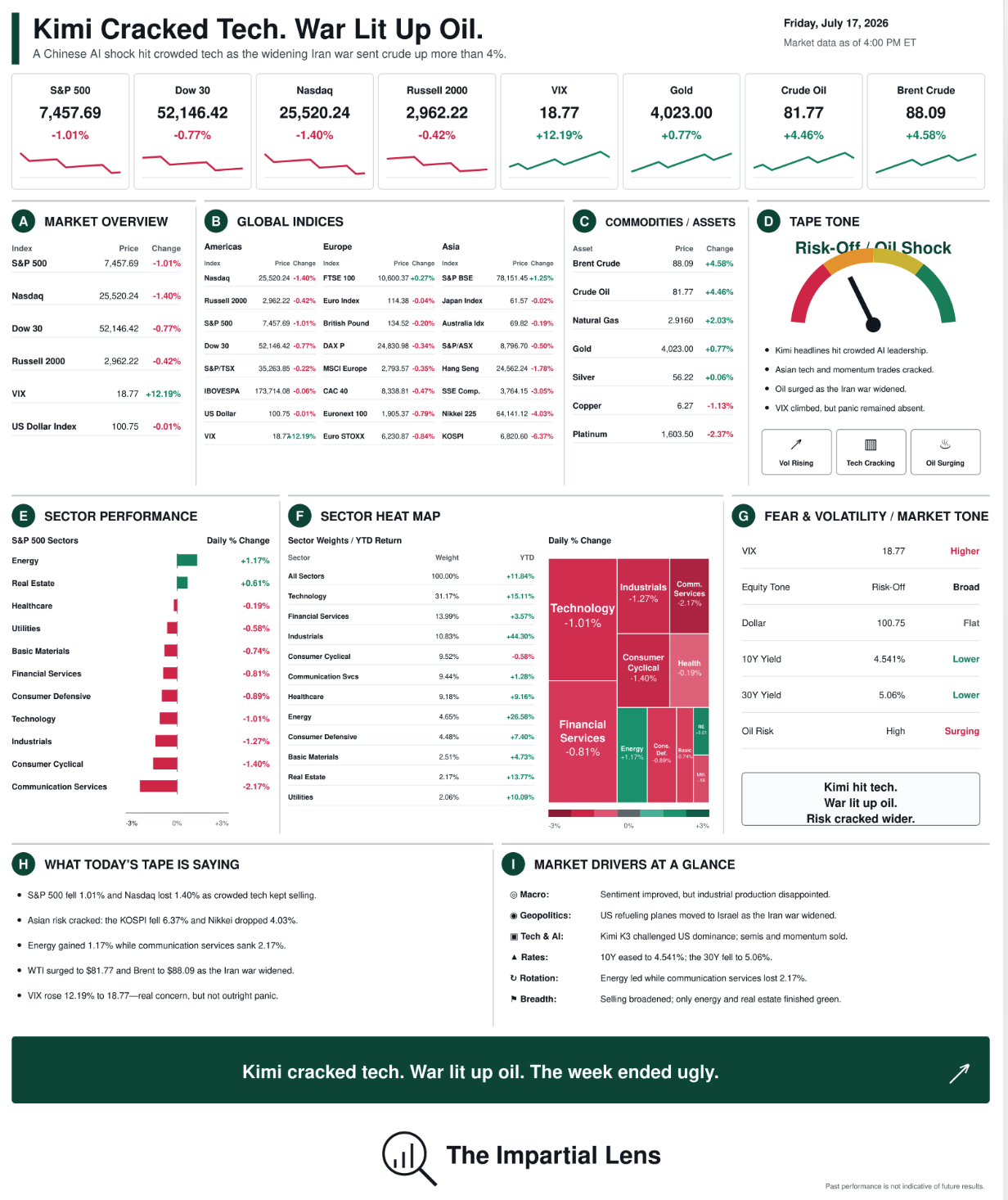

The Tape: Observable Market Data

The Nasdaq fell 1.40%, while the S&P 500 declined 1.01%. The Dow dropped 0.77%, and the Russell 2000 lost 0.42%.

The VIX jumped 12.19% to 18.77—elevated enough to show genuine concern, but still below outright panic territory.

The sector map was almost entirely red:

- Communication services: -2.17%

- Consumer cyclical: -1.40%

- Industrials: -1.27%

- Technology: -1.01%

- Consumer defensive: -0.89%

- Financial services: -0.81%

- Energy: +1.17%

- Real estate: +0.61%

Crude oil surged 4.46% to $81.77, while Brent climbed 4.58% to $88.09. Gold gained 0.77% to $4,023, and Bitcoin edged 0.18% higher.

The Dollar Index was virtually unchanged at 100.75. Treasury yields eased, with the 10-year at approximately 4.54% and the 30-year at 5.06%.

Asia took the heaviest damage. The Nikkei fell 4.03%, the Shanghai Composite lost 3.05%, and South Korea’s KOSPI plunged 6.37%.

The Macro Picture: Mixed, Not Reassuring

US consumer sentiment improved and exceeded expectations, while the available labor data continued to show limited stress.

Industrial production disappointed again. Homebuilder confidence weakened as high borrowing, material, and land costs continued to bite, even as multifamily construction reportedly increased.

This was not a clean recessionary signal. It was another picture of an economy still functioning beneath increasingly expensive capital.

Lower Treasury yields offered little comfort because oil was simultaneously surging. Growth concerns and renewed inflation risk were moving in opposite directions—exactly the combination central banks do not want.

Kimi Cracked the Mirror

China’s Kimi K3 reportedly reached the top of a prominent frontend coding benchmark and scored near the frontier across other tests.

That does not prove China has “won” the AI race. Benchmarks are not business models, durable moats, or audited cash flows.

But markets did not need proof. They needed an excuse.

The AI trade was already crowded, semiconductor momentum had already turned, and investors had already begun questioning whether enormous infrastructure spending would produce equally enormous profits.

Kimi was the match. Positioning was the gasoline.

The more serious threat is not that Chinese models must be clearly superior. They may only need to become good enough, cheaper, and faster to deploy. That would pressure the scarcity premium embedded in US AI valuations.

Meanwhile, the infrastructure bill keeps growing. Meta is reportedly considering a $10 billion computing agreement with Anthropic. Virginia regulators are questioning whether ordinary utility customers are subsidizing data-center costs. PJM officials are again warning about inadequate power capacity.

The AI race is becoming less about glamorous models and more about electricity, cooling, financing, and who ultimately pays for it.

That is a far less romantic story—and a much more expensive one.

Geopolitics: Oil Finally Paid Attention

The United States reportedly sent dozens of additional refueling aircraft to Israel as military operations against Iran appeared poised to widen.

US strikes continued against Iranian bridges, airports, and other infrastructure. Iran and its allies reportedly targeted Gulf facilities and a US command position in Syria. Elsewhere, assailants boarded a tanker in the Gulf of Aden, while another vessel was attacked near the Black Sea’s CPC terminal.

No single incident explains a 4.5% oil move. Together, they tell markets that energy infrastructure, shipping routes, and regional allies are moving closer to the center of the conflict.

Gold rose, but the dollar remained flat, and the VIX stayed below 20. The market was pricing an inflationary supply threat—not yet a full systemic crisis.

That distinction can disappear quickly.

What to Watch

Watch whether semiconductor and AI leaders can rally on good news. If they cannot, the momentum unwind has further to run.

Watch Brent near $90. A sustained move higher would revive the inflation problem just as growth data becomes less convincing.

Watch Asia. The KOSPI and Nikkei are no longer experiencing ordinary profit-taking. Forced deleveraging can create its own momentum.

Finally, watch the gap between falling bond yields and rising oil. One reflects economic anxiety; the other reflects geopolitical danger.

The Bottom Line

China does not need to prove that America has lost the AI race. It only needs to weaken the assumption that US dominance is untouchable.

Iran does not need to close the Strait of Hormuz. It only needs to keep regional infrastructure and shipping under credible threat.

Friday cracked both assumptions simultaneously.

Tech discovered that “good” is no longer good enough. Oil discovered that the war is not safely contained.

That is how an ugly Friday caps an ugly week.

For educational and informational purposes only. Not investment advice.

— The Impartial Lens