The AI Trade Finally Flinched.

Retail spending held up, jobless claims stayed low, and TSMC delivered. The Nasdaq still fell 1.47%. When good news stops working, positioning—not the story—becomes the risk.

July 16, 2026

The market did not collapse on Thursday. It did something more revealing: it was handed several reasons to rally and refused.

Retail sales met expectations. Jobless claims fell. TSMC beat earnings and raised capital spending. Japan announced a substantial Nvidia Rubin-chip order.

Yet the Nasdaq dropped 1.47%, technology fell 1.81%, communication services lost 2.79%, and volatility climbed.

That is not a verdict on artificial intelligence. It is a warning about what happens when a powerful investment story becomes overcrowded, overleveraged, and priced for near-perfect execution.

The Tape: Observable Market Data

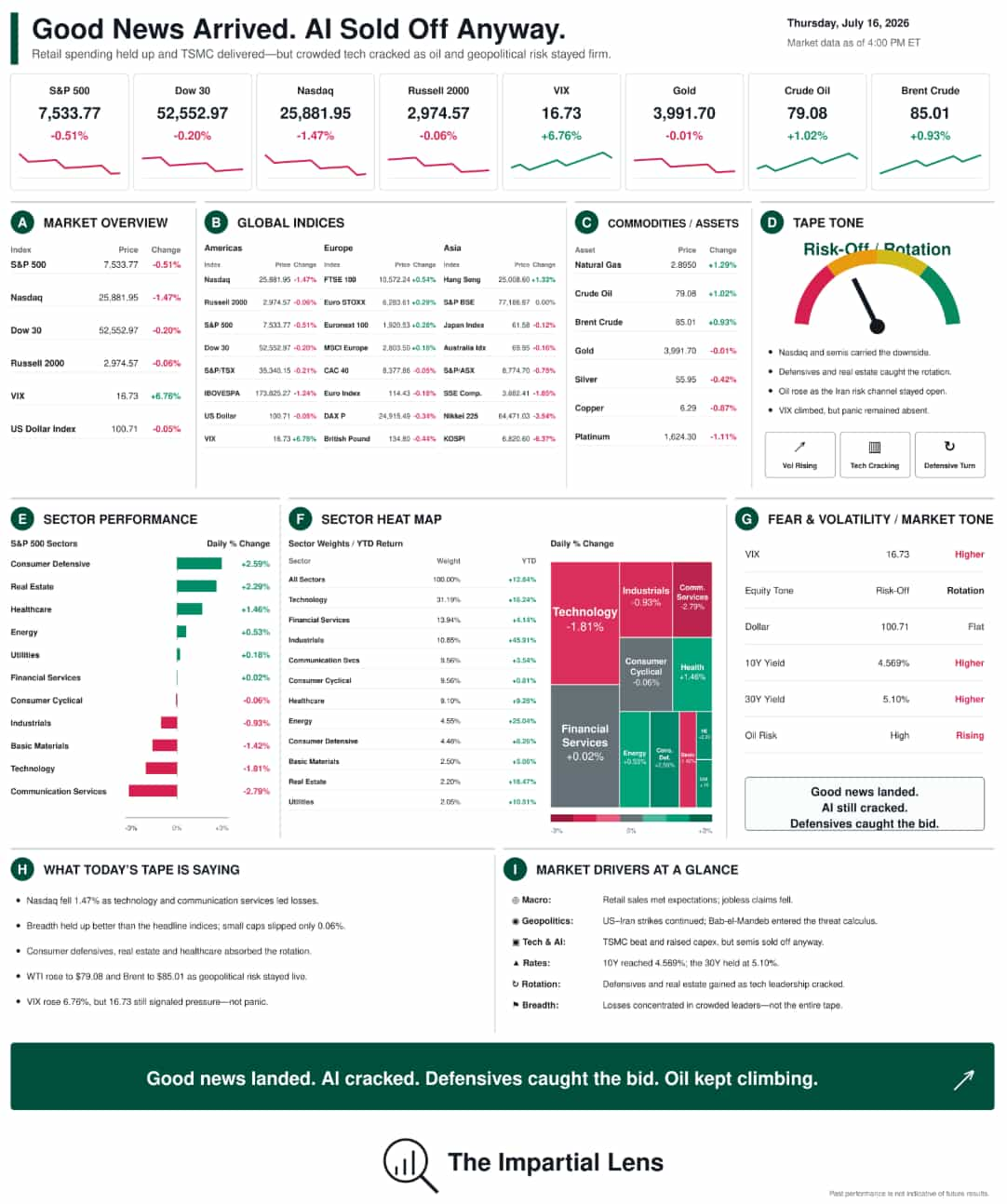

The Nasdaq was the clear underperformer, falling 1.47%. The S&P 500 declined 0.51%, while the Dow lost 0.20% and the Russell 2000 slipped just 0.06%.

That gap matters. This was not indiscriminate selling across the entire market. It was concentrated pressure in the areas carrying the largest expectations.

The VIX rose 6.76% to 16.73—higher, but still nowhere near panic territory.

Sector performance showed a defensive rotation:

- Communication services: -2.79%

- Technology: -1.81%

- Basic materials: -1.42%

- Industrials: -0.93%

- Consumer defensive: +2.59%

- Real estate: +2.29%

- Healthcare: +1.46%

- Energy: +0.53%

Crude oil gained 1.02% to $79.08, while Brent rose 0.93% to $85.01. Gold was virtually unchanged at $3,991.70, and the US Dollar Index slipped 0.05% to 100.71.

Treasury yields remained elevated, with the 10-year around 4.57% and the 30-year at 5.10%.

The Macro Picture: Resilient, Not Comfortable

The economic data did not provide an obvious recession signal.

Retail sales held up, real spending growth reportedly remained firm, and jobless claims moved back toward historically low levels. This continues to resemble a “slow hire, no fire” labor market: businesses may not be hiring aggressively, but they are not firing aggressively either.

That resilience is good for the economy. It is less convenient for markets hoping the Federal Reserve will rush to provide easier money.

Strong consumption, low layoffs, and elevated long-term yields leave the Fed with limited incentive to ride to Wall Street’s rescue. The economy is holding together, but the cost of capital remains high enough to expose weak balance sheets, leveraged positions, and unrealistic growth assumptions.

AI’s Golden Child Meets the Expectations Problem

TSMC delivered the kind of results that should have reassured the AI trade: an earnings beat, higher capital expenditure, and constructive demand commentary.

It did not work.

That may be the most important market signal of the day.

When excellent company news cannot lift the surrounding trade, the problem is rarely the latest earnings report. The problem is what investors have already paid for it.

The Korean market fell 6.37%, with reports of widespread margin calls and tighter restrictions on leveraged products. Semiconductor weakness persisted even as Japan reportedly committed to buying 27,500 Nvidia Rubin chips for robotics infrastructure.

Demand has not disappeared. Expectations have simply outrun the market’s ability to absorb disappointment.

The AI boom does not need to be fraudulent to become a bubble. It only needs investors to overestimate the speed of monetisation, underestimate infrastructure costs, and apply valuations requiring almost flawless execution.

AI may still transform the economy. That does not mean every AI-linked asset deserves every price.

Geopolitics: Two Chokepoints, One Escalating War

Reports indicated that the United States launched a sixth consecutive night of strikes against Iran, targeting infrastructure, including an airport, railway station, and bridges. Iran reportedly retaliated against facilities in Kuwait.

The more dangerous development was Tehran’s alleged instruction to the Houthis: if the United States attacks Iran’s power network, threaten the Bab-el-Mandeb gateway to the Red Sea.

That would put two critical energy arteries in play—the Strait of Hormuz and Bab-el-Mandeb.

Oil rose, but not violently. Gold was flat, and the dollar barely moved. For now, markets are pricing disruption risk rather than an uncontrollable regional shock.

That restraint should not be confused with safety.

Iran’s reported release of a detained American woman provides a small diplomatic opening. But goodwill gestures and infrastructure strikes can coexist when both sides are searching for leverage. De-escalation remains possible; accidental escalation remains easier.

What to Watch

Watch whether semiconductor weakness spreads beyond the crowded leaders. Positive market breadth would suggest rotation; deteriorating breadth would signal broader deleveraging.

Watch the 10-year yield. A move toward 5% would tighten financial conditions without the Fed doing anything.

Watch oil alongside shipping disruption. A sustained energy surge would push inflation risk back into the center of the market.

Finally, watch whether good AI news continues to produce bad price action. Markets often reveal changing conditions by refusing to respond as expected.

The Bottom Line

Thursday was not a macro disaster. It was an expectations problem.

The consumer held up. Employment held up. TSMC delivered. AI investment continued.

And the Nasdaq sold off anyway.

The market is not saying that AI is finished. It is saying that even a genuine revolution can become a dangerous trade when everyone is already leaning in the same direction.

That rubber band can stretch further—but it no longer looks indestructible.

For educational and informational purposes only. Not investment advice.

— The Impartial Lens