Monday gave the market the opposite of Friday.

Not relief.

Reversal.

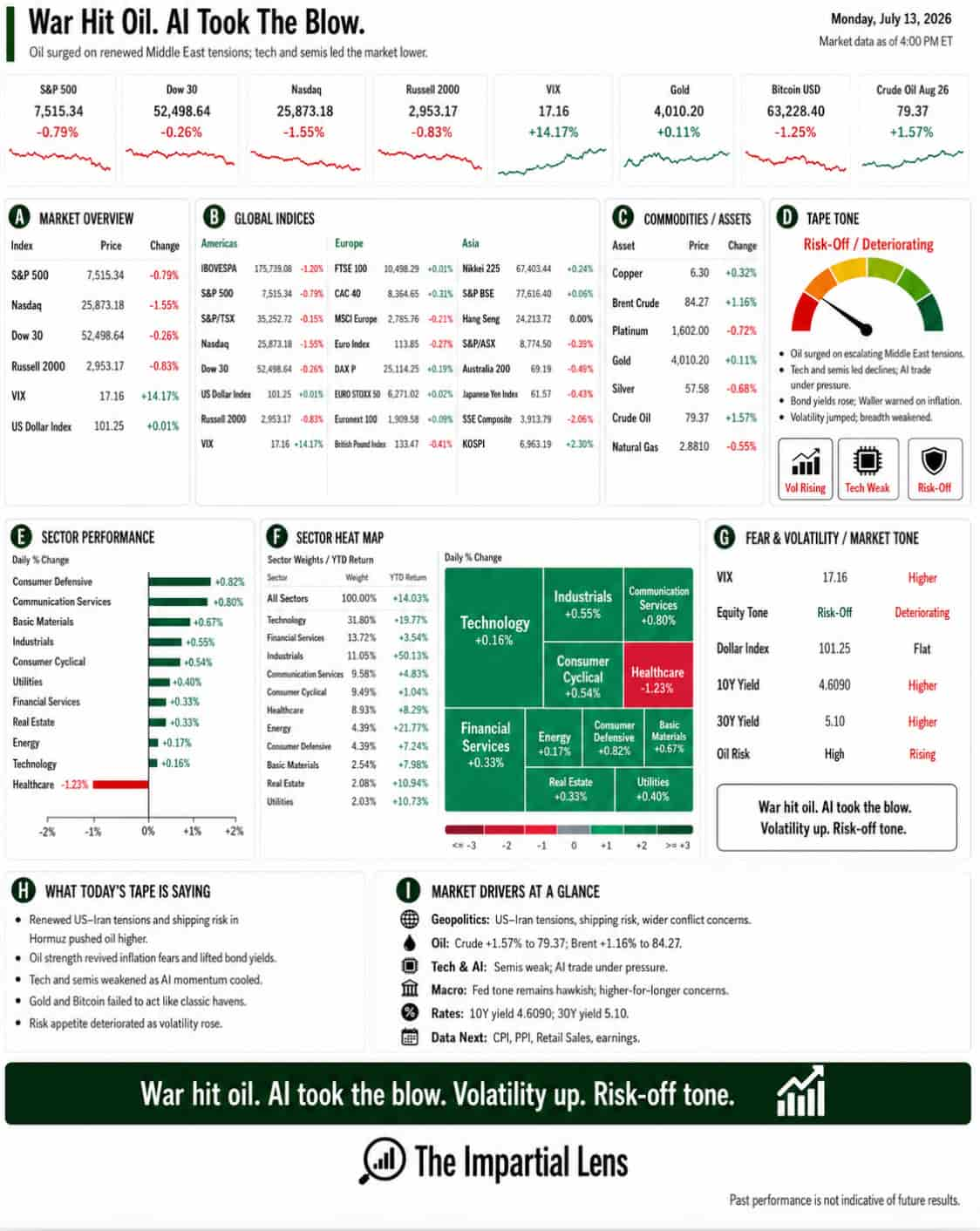

The S&P 500 fell 0.79%. The Dow lost 0.26%. The Nasdaq dropped 1.55%. The Russell 2000 declined 0.83%.

The VIX jumped 14.17% to 17.16.

Gold slipped 0.13%. Bitcoin lost 1.25%.

Crude oil rose 1.59% to $79.38, while Brent gained 1.26% to $84.35.

The 10-year Treasury yield climbed to 4.609%. The 30-year reached 5.10%.

That was not a normal flight to safety.

Stocks fell.

Bonds fell.

Gold fell.

Oil surged.

The market was repricing inflation.

War Took Back The Tape

Thursday’s rally depended on two things:

Oil had to stop rising.

And AI had to keep working.

Monday broke both conditions.

The United States carried out a third consecutive night of strikes against Iran. Iran continued its attacks, while reports pointed to more pressure on commercial vessels in the Strait of Hormuz.

The key signal was not another military headline.

It was shipping.

Traffic through Hormuz reportedly fell sharply, with only a handful of vessels visibly crossing.

The strait does not have to be completely closed to disrupt oil.

It only has to become dangerous, unpredictable, or expensive enough for shipowners and insurers to change their behavior.

That is what markets began to price.

Oil Reopened The Inflation Trade

Hormuz handles a large share of global oil and LNG flows.

A disruption there does not stay inside energy.

Higher crude feeds into transport, shipping, aviation, manufacturing, agriculture, and household spending.

It also raises a harder question for the Fed.

Can policymakers look through another energy shock when inflation is already sticky?

That is why the Nasdaq fell much more than the Dow.

Higher oil is not only a growth problem.

It is an interest-rate problem.

Waller Removed The Cushion

Fed Governor Christopher Waller added to the pressure by warning that another hot core inflation reading could force the Fed to consider tightening again (raising rates).

The market had become comfortable treating geopolitical oil spikes as temporary.

Waller suggested the Fed may not have that luxury if underlying inflation remains firm.

Oil rose because of Hormuz.

Treasury yields rose because of inflation risk.

Technology fell because higher rates reduce the value placed on distant earnings.

Gold struggled because rising yields outweighed demand for protection.

This was not just a war trade.

It was a war-to-inflation-to-rates trade.

AI Lost Its Shield

The second problem came from semiconductors.

SK Hynix suffered a sharp selloff in South Korea, dragging the KOSPI lower and reviving concerns about the durability of the AI trade.

That weakness spread into US chip stocks.

Nvidia fell 3.52%, while SanDisk and other memory-related names also came under pressure.

This does not mean AI demand disappeared.

The issue is valuation, expectations, and funding.

The AI story rests on enormous assumptions about capex, power demand, data centers, chip supply, and future profitability.

That leaves the trade vulnerable when yields rise or a major supplier delivers a negative surprise.

Monday exposed that vulnerability.

Two Selloffs Met In One Day

The market faced two shocks at once.

The geopolitical shock pushed oil and yields higher.

The semiconductor shock challenged the market’s strongest earnings story.

Together, they were harder to ignore.

The Dow fell only 0.26%, while the Nasdaq lost 1.55%.

That gap tells the story.

This was not a full-market liquidation.

It was concentrated pressure on the part of the market most dependent on falling inflation, manageable yields, and confidence in AI spending.

Fear rose.

But there was no panic.

Gold’s Failure Matters

War escalated.

Oil surged.

Volatility jumped.

And gold still fell.

Bitcoin also weakened, while the dollar was broadly flat.

That suggests Monday was driven more by inflation and monetary-policy repricing than by a pure rush into safe assets.

When investors fear persistent inflation and tighter policy, both bonds and gold can struggle.

Monday looked much closer to that scenario.

The Real Read

Monday was not simply a bad session caused by another war headline.

Two assumptions were challenged at once.

The first was that Hormuz risk could be contained before becoming a sustained inflation problem.

The second was that AI strength could continue overpowering weakness elsewhere.

Oil surged.

Bond yields rose.

Waller reopened the possibility of a tighter policy.

And semiconductors cracked.

The market did not panic.

But the path narrowed.

Hormuz has to stabilize.

Inflation has to cooperate.

And AI has to prove Monday was an unwind, not the beginning of a broader reassessment.

Oil surged.

Tech lost control.

And this time, the bond market did not come to the rescue.

The Impartial Lens provides market and geopolitical commentary for educational purposes. It is not investment advice.