Tuesday gave the market a reminder.

Risk appetite can return quickly.

But it can leave just as fast.

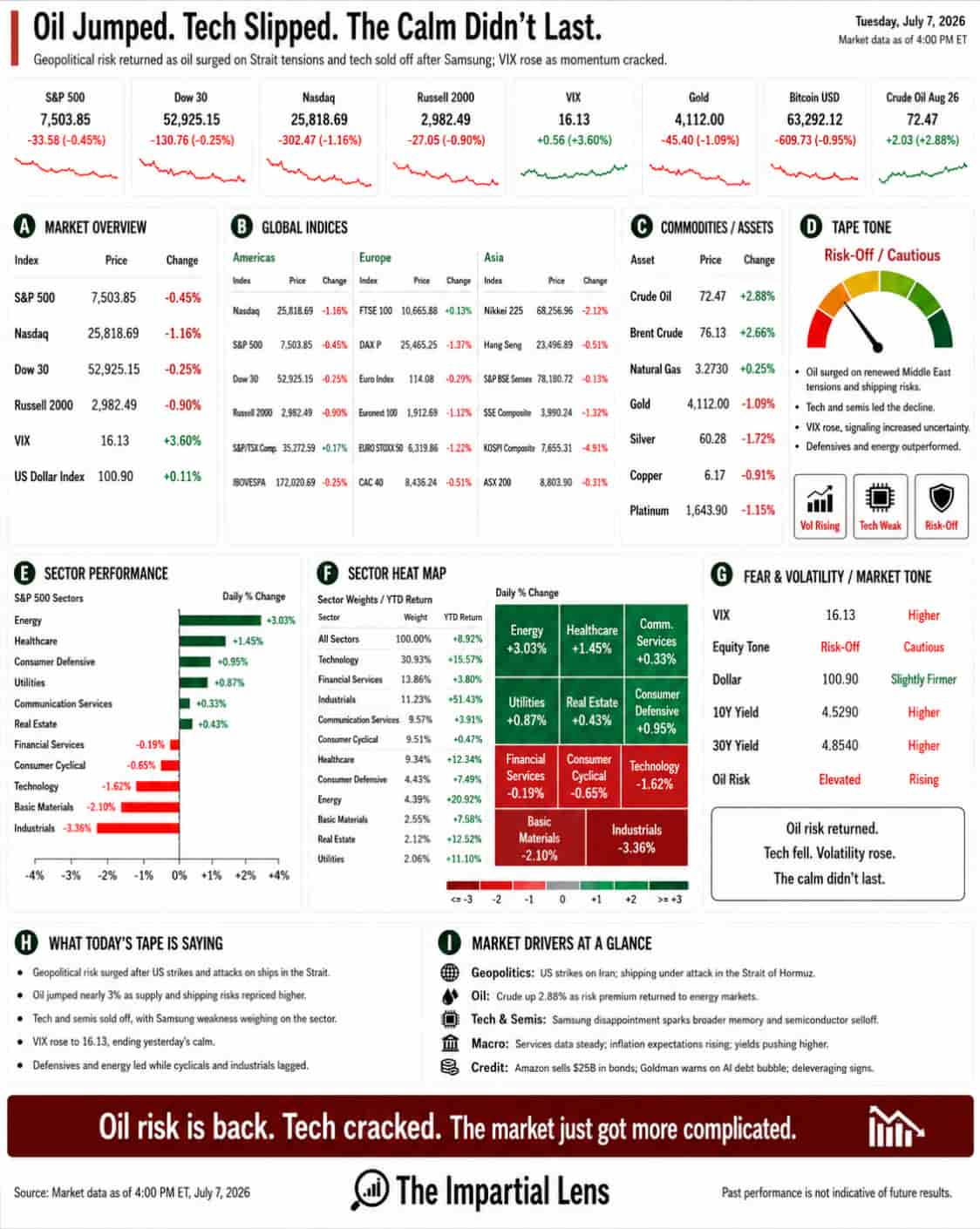

After Monday’s clean growth-led bounce, Tuesday was a different tape. The S&P 500 fell 0.45%. The Dow lost 0.25%. The Nasdaq dropped 1.16%. The Russell 2000 fell 0.90%.

The VIX rose 3.60% to 16.13.

That is not panic.

But it is a change in tone.

Gold fell 1.09%. Bitcoin slipped 0.95%. Crude oil jumped 2.88% to $72.47.

So the market gave us a clear message:

Oil risk came back.

Tech leadership cracked.

And the calm did not last.

The Strait Came Back Into Focus

The biggest macro story was Hormuz.

Fresh U.S. strikes against Iran, following attacks on commercial shipping, put the Strait back at the center of the market conversation. That matters because Hormuz is not just a geopolitical headline. It is a direct line into oil, shipping, insurance, inflation expectations, and central-bank risk.

The two key parts of the interim deal now look vulnerable:

Oil sanctions relief.

And safe passage for vessels through the Strait of Hormuz.

That is why crude jumped.

The market had started to move beyond Hormuz. Oil had been treated as manageable. Geopolitical risk had faded into the background while investors returned to AI, tech, and earnings.

Tuesday pushed back against that.

Iranian attacks on vessels, U.S. retaliation, and renewed uncertainty around commercial shipping reminded investors that the energy risk premium can return quickly.

The market can ignore Hormuz for a few sessions.

It cannot ignore ships being hit.

Tech Lost The Wheel

The other pressure point was tech.

The Nasdaq was the weakest major U.S. index, down more than 1%. Technology fell 1.62%. Industrials dropped 3.36%. Basic materials lost 2.10%. Consumer cyclical fell 0.65%.

That is a very different setup from Monday.

The AI trade had bounced, but it did not follow through.

Semiconductors were under pressure after Samsung. Memory names were weak. Momentum struggled. UBS flagged deleveraging. Goldman warned that the character of the market has changed. Morgan Stanley again pointed clients away from chip stocks and toward hyperscalers.

That is the key point.

The AI trade is not dead.

But it is no longer moving as one clean block.

Investors are separating the companies that may benefit from AI from the companies exposed to pricing pressure, capex risk, supply-chain competition, and crowding.

That is a more mature market.

It is also a more difficult one.

Samsung Was A Warning

Samsung mattered because it exposed the problem with expectations.

When a company can deliver strong numbers and still see its stock punished, the market is telling you the bar is too high.

That is where parts of the AI and memory trade now sit.

The market is no longer asking whether AI demand exists.

It is asking whether the current prices already assume too much.

That distinction matters.

A real theme can still be over-owned.

A real growth story can still get crowded.

A real earnings cycle can still disappoint if investors demand perfection.

Tuesday’s semiconductor weakness was not just about one company. It was about the broader question hanging over AI hardware:

Has the spending boom already been priced beyond the next few quarters?

Rotation Turned Defensive

The sector map told the story.

The winners were not the aggressive growth groups.

Energy rose 3.03%. Healthcare gained 1.45%. Consumer defensive rose 0.95%. Utilities gained 0.87%. Communication services managed a small gain of 0.33%.

That is not a broad risk-on tape.

That is a market moving toward oil, defensives, and selective safety.

Financials slipped. Technology weakened. Consumer cyclicals fell. Industrials were hit hard. Basic materials lagged badly.

This was not a collapse.

But it was a reset.

Investors moved away from the parts of the market most exposed to growth, leverage, and momentum. They moved toward the areas that can hold up when the macro picture gets more complicated.

That is what happens when oil jumps and tech stops leading.

Inflation Risk Reappeared

Oil is still the market’s fastest inflation signal.

When crude rises sharply because of geopolitical risk, the market immediately has to think through second-order effects.

Higher transport costs.

Higher input costs.

Higher inflation expectations.

Higher pressure on consumers.

Less flexibility for the Fed.

More pressure on long-duration growth assets.

That is why Tuesday matters.

This is not just about whether oil is up one day.

It is about whether the market can keep assuming that inflation pressure is contained while the Middle East remains unstable, shipping remains vulnerable, and the AI trade remains crowded.

Those are hard things to balance.

The Fed may be comfortable for now.

But a market with rising oil, rising inflation expectations, and falling tech leadership becomes harder to support.

The Real Read

Tuesday was not a panic.

It was a warning.

The market had just started to believe that growth was back in control. Tech led Monday. Volatility fell. Risk appetite returned.

Then Tuesday arrived.

Oil jumped. VIX rose. The Nasdaq fell. Semis weakened. Momentum cracked. Defensive sectors caught a bid. Energy led. Gold and Bitcoin did not act like strong confirmation assets.

That is a different tape.

It tells us the rally is still vulnerable to two things:

Geopolitics.

And crowded AI leadership.

Those are now the two pressure points.

Hormuz can bring back inflation risk.

AI crowding can bring back market-structure risk.

Put them together, and the calm surface gets much harder to trust.

The market is not broken.

But it is no longer cruising.

Oil jumped.

Tech slipped.

Volatility rose.

The market’s message was simple:

The rally can keep going, but only if energy risk stays contained and AI stops wobbling.