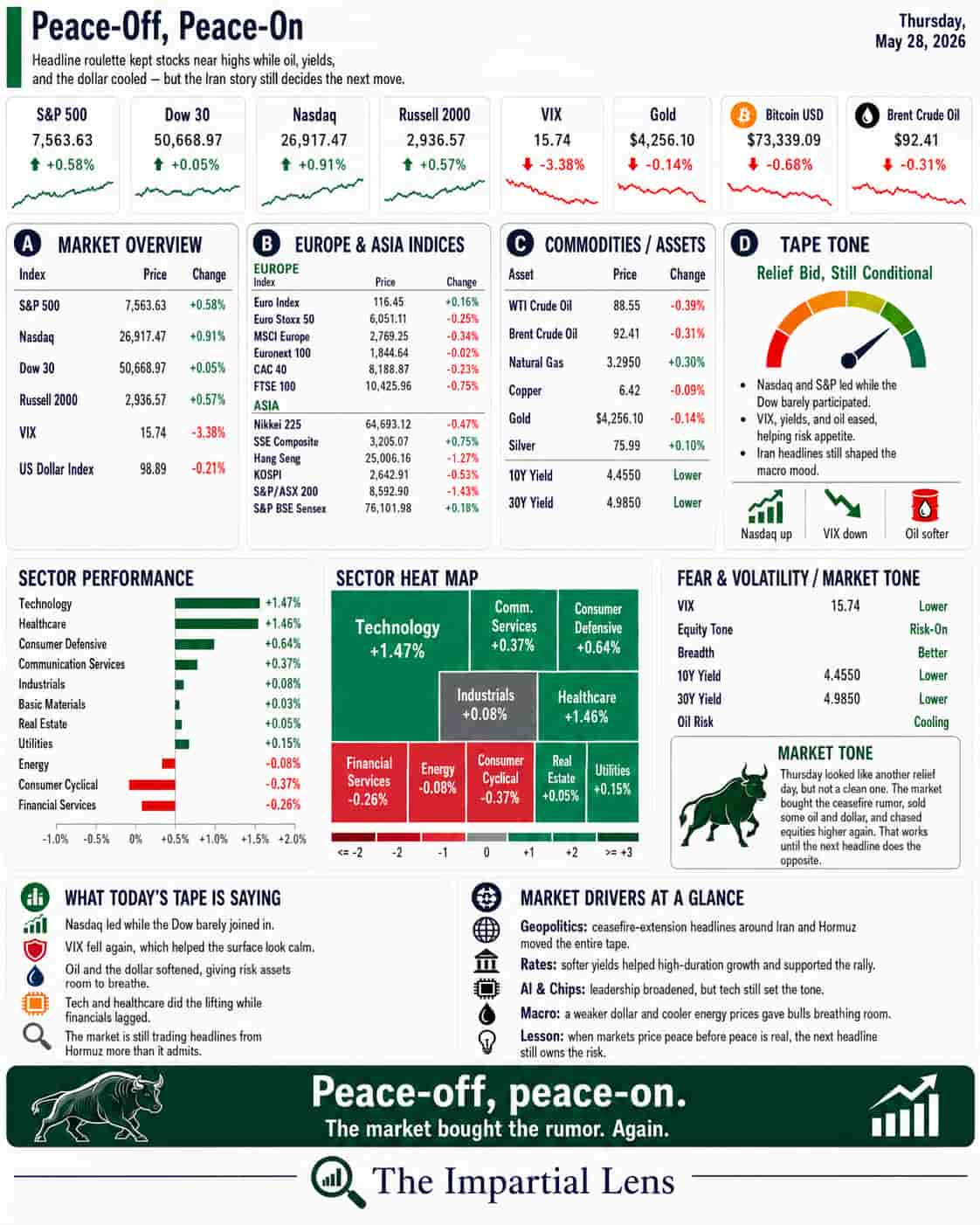

Stocks rallied again as Iran headlines improved, oil fell, and bonds caught a bid. But the market is still trading a political negotiation as if it were a solved problem.

Thursday’s tape looked simple on the surface.

Stocks up.

Bonds up.

Gold up.

Oil down.

Dollar down.

Volatility contained.

The market liked the idea that the U.S. and Iran may be moving toward a 60-day memorandum of understanding to extend the ceasefire. That was enough to push risk assets higher and pull oil lower.

But the key word is “idea.”

The agreement still needed Trump’s approval. Iranian reports pushed back on parts of the story. Vance said Trump was not ready to approve a deal because distance remained on the nuclear issue. Meanwhile, the U.S. had struck an Iranian military site in Bandar Abbas.

That is not a clean peace tape.

That is headline roulette.

And the market is still betting that the ball lands on green.

The Dashboard Says: Relief, But Not Resolution

The market’s message was constructive.

Stocks gained after reports of a tentative U.S.-Iran agreement. Bonds caught a bid. Oil softened. Gold also rose, which is worth noting.

Normally, if investors fully trusted a peace deal, gold might weaken as safe-haven demand fades. But gold rising alongside stocks tells us investors are not completely relaxed.

They want the upside.

But they still want insurance.

That is the first lesson:

When stocks and gold rise together, the market may be optimistic — but it is not carefree.

It is buying risk and protection at the same time.

That is not irrational.

It is exactly what you would expect when the market wants to believe in de-escalation but knows the political story can reverse with one statement.

Geopolitics Is Still the Trade

The market wants to treat Iran as a binary event: deal or no deal.

But geopolitics rarely works that cleanly.

The U.S. struck an Iranian site. Iran disputed parts of the peace narrative. Beirut was hit by Israeli airstrikes after a month of quiet. Canada sent a frigate through the Taiwan Strait despite Beijing’s objections. The Chinese navy pushed a Dutch frigate from claimed waters using electronic warfare. Europe is exploring emergency powers over chip supplies.

These are not side stories.

They are market stories.

Hormuz affects oil and shipping.

Taiwan affects semiconductors.

Europe’s chip rules affect supply chains.

Middle East strikes affect inflation expectations.

Defense spending affects budgets.

Budgets affect bond markets.

That is how political risk becomes financial risk.

Slowly at first.

Then all at once.

Oil Fell, But Energy Risk Did Not Disappear

Oil moved lower because the market believes the probability of a reopened or stabilized Strait of Hormuz has improved.

That matters.

Lower oil gives investors permission to believe inflation pressure may ease. It helps consumers. It helps transport. It helps central banks. It helps risk appetite.

But the oil story is not solved just because crude fell for a day.

The headline stack still included concerns about Cushing inventories, SPR drains, Hormuz tolls, Oman pressure, and whether markets are underestimating the odds of a timely reopening of the Strait.

That is the tension.

The market is pricing relief.

The energy system is still operating under stress.

Oil does not need to explode higher every day to matter. If it stays unstable, it keeps inflation expectations alive and forces businesses, governments, and consumers to plan around uncertainty.

That is not bullish or bearish by itself.

It is fragile.

The Politics of AI Is Arriving

The AI story also changed tone.

The market still loves AI. Anthropic’s valuation, Goldman’s robotics call, chip chokepoints, nuclear supply chains, and hyperscale compute demand all kept the theme alive.

But the politics of AI is becoming harder to ignore.

One headline captured the issue directly: rising energy costs from hyperscale compute demand, combined with fears of AI-driven job displacement, make the Fed’s job more politically combustible.

That matters.

AI is no longer just a technology story.

It is becoming an energy story.

A labor story.

A national-security story.

A chip-supply story.

A grid story.

A political story.

The market keeps treating AI as a growth engine.

That may be right.

But if AI drives electricity demand higher, supports energy inflation, disrupts labor markets, and requires massive capital spending, then it also becomes part of the inflation and rates story.

That is the awkward part.

The same AI boom that supports stocks may also help keep rates higher.

Bonds Still Get the Final Vote

Thursday’s bond action helped the market.

A strong 7-year auction and foreign demand gave investors some breathing room. Bonds rallied. Yields eased. That helped equities.

But one good auction does not end the bond story.

The broader issue remains: the market is still trying to rally through deficits, defense spending, AI capex, energy investment, inflation pressure, and political promises that all cost money.

That is why real yields matter.

If real yields stay high, the market has less room for fantasy. Expensive assets must justify themselves against safer alternatives. Crowded growth trades must keep delivering.

The bond market is not the loudest part of the tape.

But it is still the part with veto power.

The Real Read

Thursday was constructive.

Peace headlines helped.

Oil softened.

Bonds rallied.

Stocks rose.

Gold stayed bid.

AI enthusiasm remained intact.

But the market is still balancing on a fragile set of assumptions.

That Trump approves the Iran deal.

That Iran accepts the core terms.

That Hormuz stabilizes.

That oil stays contained.

That bond yields keep easing.

That AI keeps leading.

That political pressure around energy, labor, immigration, China, and supply chains does not spill into markets.

That is a lot to ask.

The market is not pricing certainty.

It is pricing the hope that the political and geopolitical risks remain manageable long enough for the rally to continue.

That may be enough for now.

But the lesson is clear:

Peace headlines can move markets.

They do not automatically remove risk.

For now, the tape is choosing relief.

But relief is not resolution.

And in this market, the difference still matters.