Stocks looked calm, but the tape underneath was less comfortable: AI momentum is still alive, geopolitics is still active, and the market is starting to notice the cracks.

Wednesday was not a dramatic market day on the surface.

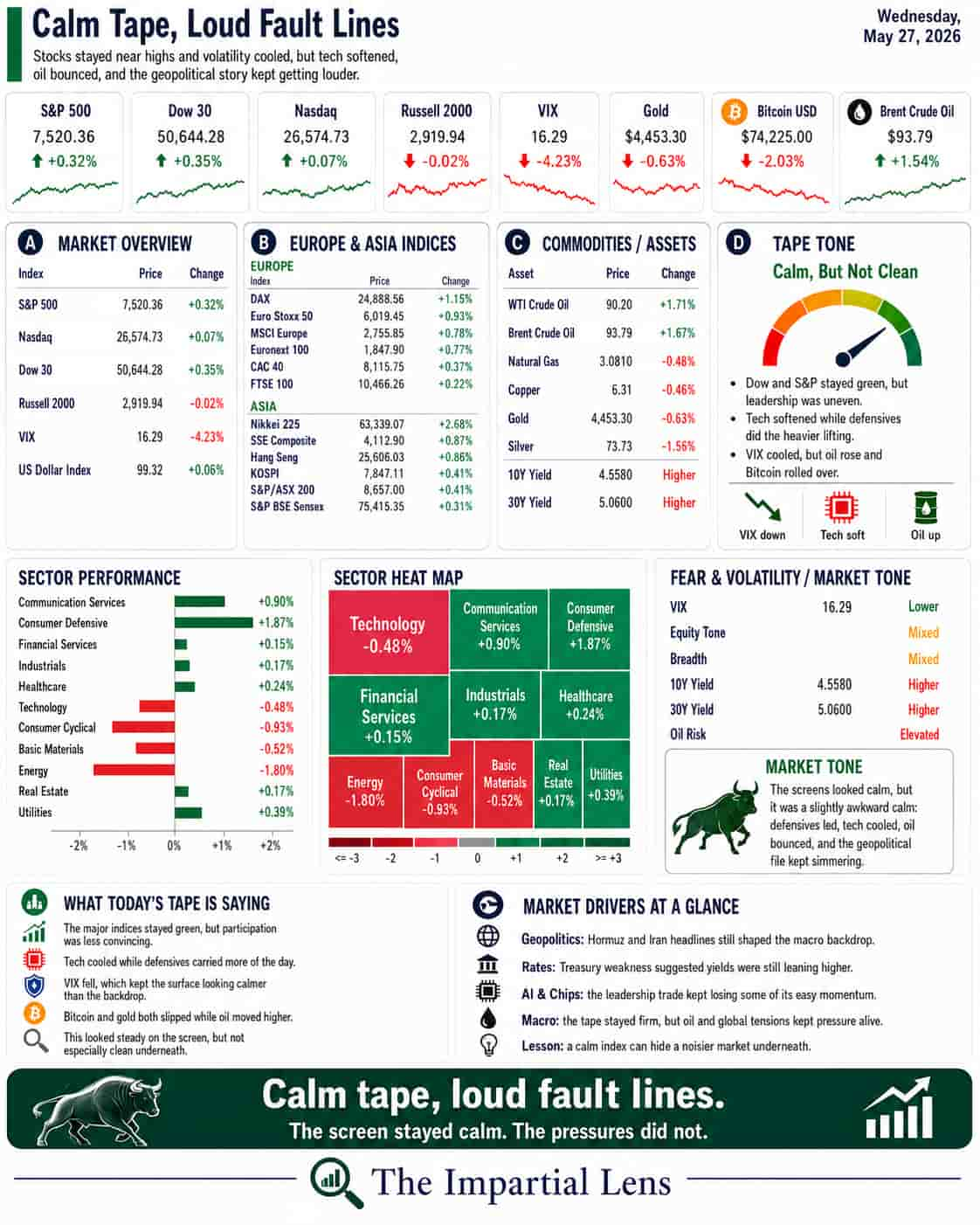

Stocks were mostly flat. Oil fell. Bonds behaved. The major indices hovered close to record highs. Nothing exploded.

But that is exactly why the day matters.

The market is no longer moving only on simple risk-on or risk-off signals. It is now trying to process several different stories at once:

AI momentum is still powerful.

Semiconductor trades are still crowded.

Oil is falling despite new strikes near Hormuz.

Bonds are still cheap compared with stocks.

China is tightening capital channels.

And geopolitics is no longer staying politely in the background.

This is not a broken market.

But it is a more complicated one.

The Dashboard Says: Calm, But Not Clean

The broad market did not send a panic signal.

Stocks consolidated below record highs. Oil declined on continued Middle East peace hopes. Tesla and Amazon helped support the tape. Travel and leisure benefitted from lower energy prices. Communications saw strength from new subscription efforts across Meta’s platforms.

That is the good news.

But the tape was not as strong underneath.

The headline stack pointed to “Shanghai, Straits, Semis, and Selling.” That is a good summary of the day. The market is still trying to hold together, but leadership is becoming more uneven.

The AI trade remains alive, but the upside reflex is fading. Momentum still owns the trend, but the strongest parts of the market are starting to show exhaustion.

That is the first lesson:

A market can stay near highs while the quality of the rally gets worse.

Price is what everyone sees.

Participation is what tells you whether the move is healthy.

Semis Are Still the Center of the Trade

The semiconductor trade remains the market’s most important risk pocket.

AI still leads. Nvidia still matters. Memory still matters. Korea still matters. Taiwan still matters. China still matters.

But the trade is getting stretched.

One headline warned that the “semis leverage machine” may be starting to wobble. Another noted the biggest SOXL down candle ever. Another flagged Korea’s AI mania entering “air pocket” territory, with older investors now accounting for a major share of margin debt.

That is not a normal, quiet, institutional accumulation story.

That is a crowded momentum story.

The point is not that AI is fake.

The point is that the trade is crowded enough that even good news may start producing weaker reactions.

When everyone already owns the same story, the market needs more than confirmation. It needs constant acceleration.

That is a difficult standard to maintain.

Geopolitics Is Driving the Macro Map

The geopolitical story grew louder again.

The U.S. conducted new strikes in Iran around the Hormuz Strait after drone intercepts. Iran had already vowed retaliation after earlier U.S. port strikes. Hamas confirmed the death of a top military commander in an Israeli strike. Russia warned Rubio to get diplomats and Americans out of Kiev ahead of “systematic strikes.” China increased military activity around Taiwan.

This is not isolated noise.

It is a map of pressure points.

Hormuz affects oil and shipping.

Taiwan affects semiconductors.

Ukraine affects energy, defense, and European fiscal strain.

China affects capital flows, supply chains, and AI competition.

The Middle East affects inflation expectations.

That is why geopolitics belongs in market commentary.

It is not separate from the tape.

It is part of the tape.

Oil Falling Does Not Mean Risk Is Gone

Oil declined on hopes that a U.S.-Iran deal might still be possible.

That helped the market.

But the strange part is that oil softened while military activity continued. That tells us traders are still pricing the possibility of negotiation more than the reality of escalation.

That may prove right.

But it is not risk-free.

Oil does not need to go straight to $150 to matter. It only needs to remain unstable long enough to keep inflation expectations, shipping routes, and policy decisions under pressure.

The market wants to believe the Hormuz problem is contained.

But the headlines keep saying: not yet.

Bonds Are Still the Referee

The bond market remains central.

One headline noted that Treasuries still look historically cheap versus stocks. Another warned that the Fed funds rate may be roughly 100 basis points too low. Another flagged that rate hikes could still be coming.

That matters because the market keeps trying to rally as if monetary conditions are easy.

But if real yields stay elevated, the math changes.

Higher real yields make safe assets more competitive. They pressure valuations. They raise the bar for growth stocks. They make AI capex, housing, government debt, and private credit more expensive.

That is the simple lesson:

If bonds keep offering more return with less risk, stocks have to justify their price.

And expensive, crowded stocks have to justify it most of all.

The heel of the hunt.

This was not a crisis day.

But it was not a clean day either.

The market is still near highs, but the number of stress points is growing.

Semis are crowded.

AI leadership is still powerful but less effortless.

Hormuz remains unresolved.

Oil is trading peace hopes while military headlines keep arriving.

China is tightening capital channels.

Taiwan risk is active.

Ukraine risk is active.

Bonds still matter.

And consumer sentiment remains weak beneath the surface.

The market is not pricing certainty.

It is pricing the hope that these risks remain manageable.

That may be enough for now.

But the lesson is clear:

A market can remain strong while becoming more fragile underneath.

For now, the melt-up still owns the trend.

But the easy part may be over.

The next phase will depend less on whether AI remains exciting and more on whether bonds, oil, geopolitics, and positioning allow the rally to keep breathing.