This wasn’t another weekend of screaming headlines. It was something quieter—and far more important: control.

All weekend long, the alerts kept piling up—war risks, oil spiking, political drama, trade tensions. On the surface, it felt like the usual chaotic noise. But if you stepped back, a deeper pattern snapped into focus. The world is suddenly waking up to its own bottlenecks. Global trade has never really been the open highway we liked to imagine. It flows through narrow, fragile corridors that are ridiculously easy to squeeze. And right now, those corridors are lighting up on the map like never before.

The Map That Was Never Flat

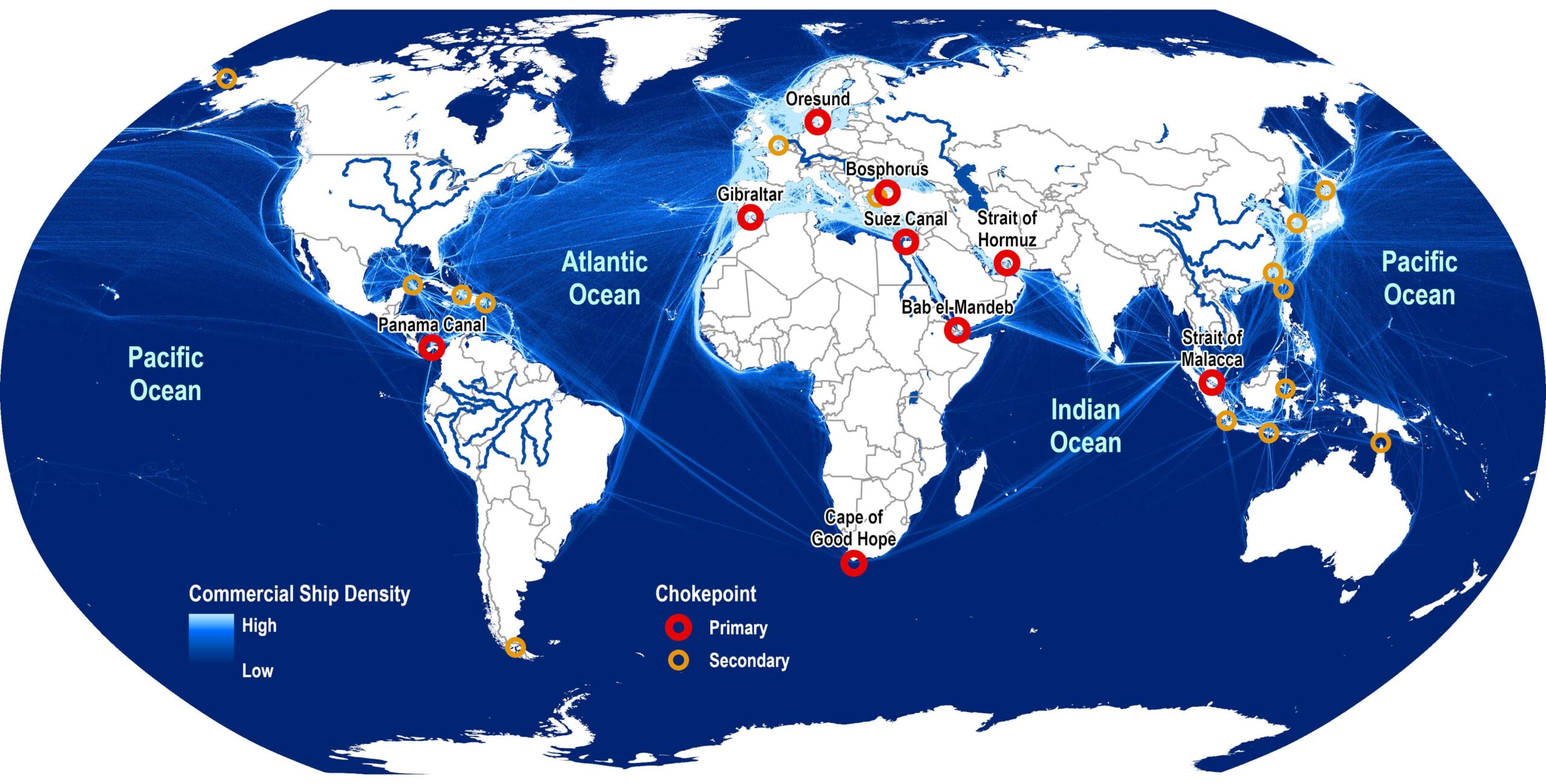

*Global Shipping Traffic Density (2015–2021). Source: IMF World Seaborne Trade Monitoring System via World Bank Data Catalog. Visualization adapted from Visual Capitalist / ArcGIS.

Think about the critical pinch points that actually move the world:

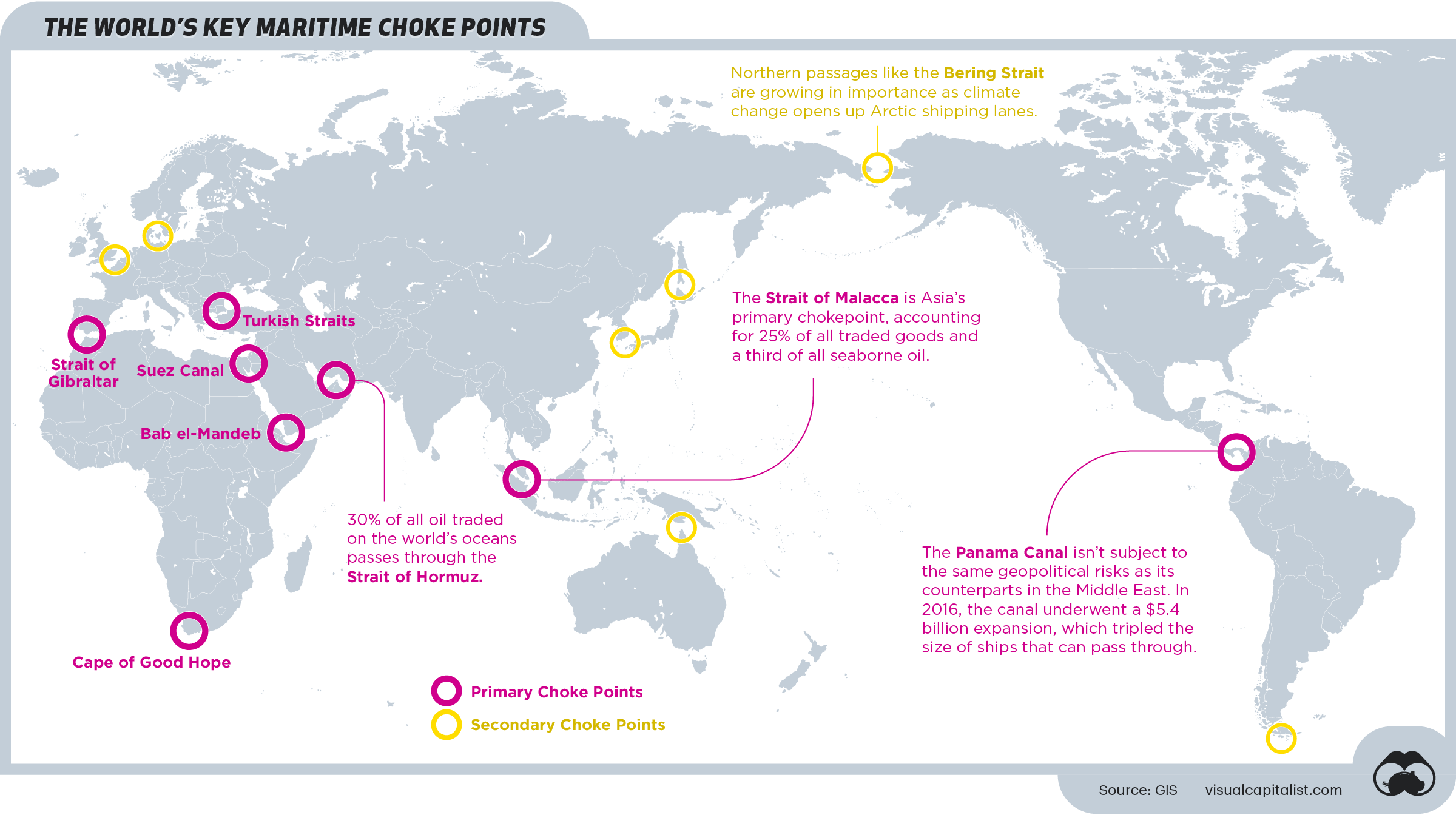

The Suez Canal — Europe’s express lane to Asia.

The Panama Canal — the Atlantic-Pacific shortcut.

The Strait of Hormuz — where a huge chunk of global oil has to squeeze through.

The Strait of Malacca — one of the planet’s busiest shipping highways.

Bab el-Mandeb — the Red Sea gateway.

Gibraltar, the Turkish Straits, and more.

These aren’t just waterways. They’re leverage points. Whoever controls them (or can disrupt them) holds real power over flows, prices, and timing.

And the Map Is Getting New Lines

For decades the system felt stable. Now fresh routes are opening up, especially in the Arctic. The Northern Sea Route promises a shortcut between Asia and Europe. The Bering Strait becomes a new gateway. Sounds exciting—until you look closer.

Russia essentially holds the keys to much of this new Arctic system. Icebreakers, navigation, ports, regulations… none of it runs without their involvement. You might not pay a classic toll, but you’ll pay in escort fees, compliance, dependencies, and strategic favors. It’s gatekeeping with extra steps.

Different routes, same story: control the choke, control the price.

From Free Flow to Friction Economy

We spent decades optimizing for efficiency—long, lean supply chains, just-in-time delivery, rock-bottom costs. That era is cracking. What’s replacing it? Strategic control. Leverage. Access that can be granted or withheld. Conflicts flare up and cool down. But when the actual infrastructure of trade gets politicized and monetized, the effects are permanent.

These arteries carry energy, food, components, even military logistics. Disrupt them and everything downstream feels it.

Why Markets Are Still Missing It

The screens keep reacting to the daily soap opera: “Talks progressing… tensions easing…” Meanwhile, the bigger structural shift is happening in the background. The hardware of globalization is being carved up, protected, and priced.

The chain reaction is already moving:

Chokepoint pressure → higher transport costs → supply headaches → sticky inflation → nervous bond yields → tighter liquidity → pressure on risk assets.

No wonder oil moved first. It’s the most sensitive to route risk, not just demand. While broader markets stayed relatively calm, crude reminded us who’s really in the driver’s seat. Behind the scenes, the smarter money isn’t panicking, but they’re repositioning—trimming exposure, adding hedges, preparing for a world with less margin for error. The market is still charging forward, but the road is narrower and the guardrails are rusting.

Investing in a World of Chokepoints

(Not investment advice—just one way to think about the shift.)

If flows are being controlled, pricing power moves upstream to those who manage, protect, or profit from the friction.

Energy sits at the top of the food chain. Integrated oil majors with strong cash flows, flexible LNG players, and midstream/pipeline operators (the literal toll roads of energy) all stand to benefit when routes get tense.

Shipping & Logistics are the hidden winners when ships reroute, delays pile up, and freight rates spike. Container lines, tankers, and anyone exposed to rising rates can turn inefficiency into profit.

Infrastructure Owners are the purest plays—ports, canals, strategic terminals, rail links. They get paid on volume, regardless of which way the cargo is heading.

Defense & Security become critical when chokepoints matter more. Naval tech, maritime protection, surveillance, contractors—they all thrive when enforcement and deterrence are non-negotiable.

Then come the second-wave commodities: fertilizers, metals, agriculture. Everything that needs reliable timing and passage.

Longer term, look at reshoring and domestic themes—companies that shorten supply chains or build redundancy. And further out, Arctic-related plays (ice-class vessels, northern infrastructure), keeping in mind who actually controls the keys up there.

What to Watch Out For

Avoid the crowded, high-multiple growth stories that assume smooth, cheap global flows. They’re vulnerable to exactly this environment. Same with pure “just-in-time” global businesses that live and die by frictionless trade.

The simple filter: Does this asset benefit from friction and control… or does it suffer when flows get expensive and unpredictable?

The New Game

Last cycle, efficiency won. Next cycle, control gets paid. We didn’t get a fresh crisis this weekend. We got clarity. The world isn’t falling apart—it’s reorganizing around leverage, around arteries old and new, around the realization that some routes will always matter more than others. The story can still be optimistic. But the structure has changed. And smart positioning starts with seeing that clearly.