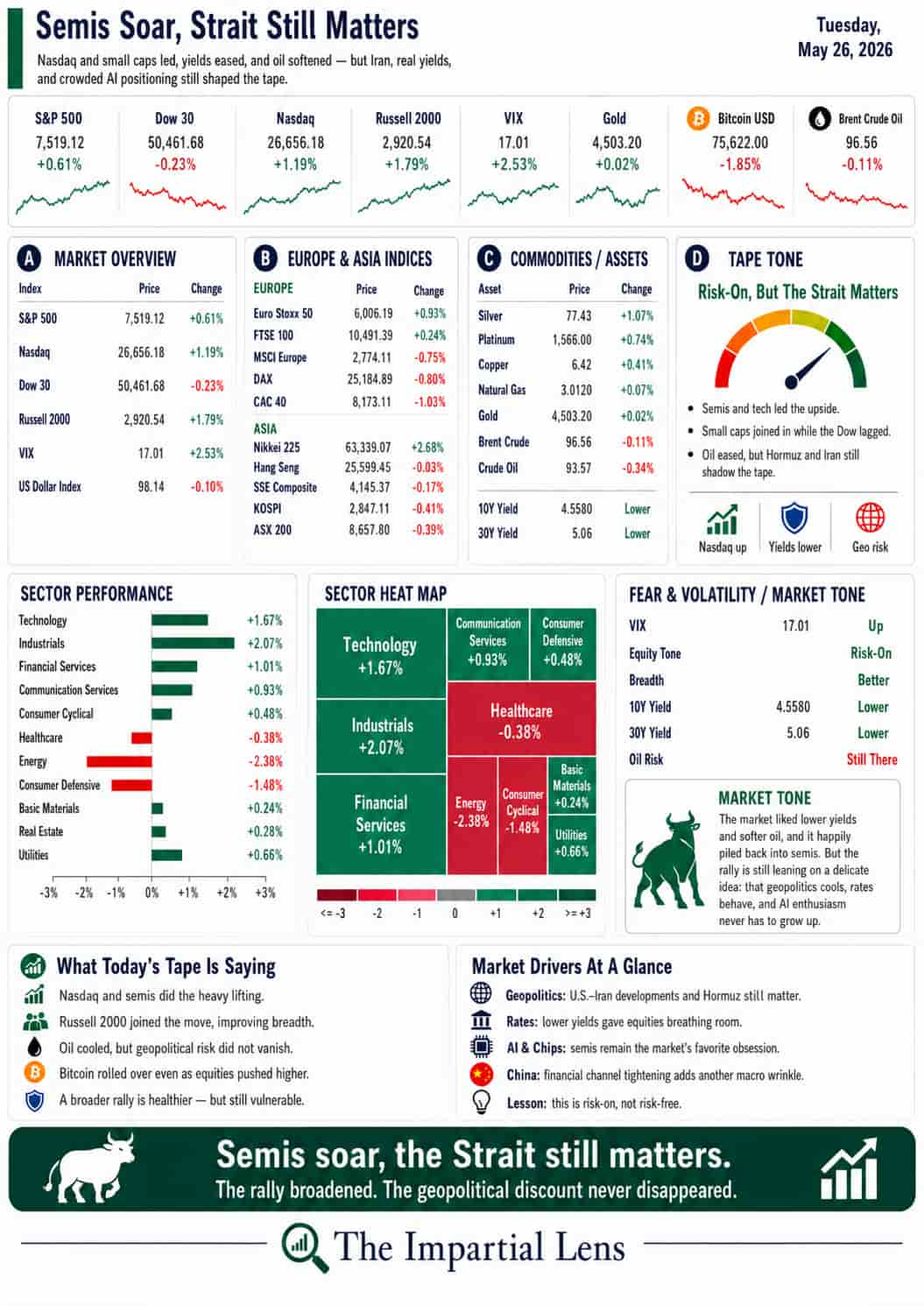

Stocks pushed higher again, but this rally is now leaning on a fragile assumption: that politics, war, oil, and bonds all stay contained at the same time.

Markets came back from the long weekend in risk-on mode.

The S&P 500 rose 0.37%.

The Nasdaq gained 0.19%.

The Russell 2000 climbed 0.91%.

The Dow gained 0.58%.

The VIX slipped to 16.70.

Brent crude rose to about $103.94.

Gold fell 0.70%.

Bitcoin dropped more than 2%.

So yes, stocks were green.

But the more important story is what the market is choosing to look past.

This is not just an AI rally anymore. It is an AI rally taking place inside a world of rising real yields, Middle East strikes, Taiwan pressure, China capital controls, European fiscal stress, and a U.S. political system trying to fund industrial policy, defense, AI infrastructure, and debt service all at once.

That is a heavier backdrop than the index level suggests.

The rally is still working.

But the list of things it needs to ignore keeps getting longer.

The Dashboard Says: Broader, But Not Clean

The good news is that the rally broadened.

The Russell 2000 led, up nearly 1%, which suggests investors were willing to move beyond the largest tech names. Financials helped. Technology gained 0.73%, Industrials rose 0.79%, Healthcare added 0.88%, and Energy was slightly positive.

That is healthier than a narrow Nasdaq-only rally.

But it was not a clean tape.

The Nasdaq gained only 0.19%. Bitcoin sold off. Gold weakened. Oil rose. And the VIX stayed low, suggesting investors are still not paying much for protection.

The market is broadening, but it is not relaxing.

That distinction matters.

A broader rally can be constructive.

But a broader rally sitting on top of geopolitical risk, political uncertainty, and stubborn real yields is still vulnerable.

Geopolitics Is Moving Toward the Center

The geopolitical backdrop is no longer background noise.

The U.S. conducted “self-defense strikes” near Hormuz. Iran vowed a swift response. Rubio signaled optimism on a peace deal in “days.” Hezbollah sites were struck. Chinese aircraft and warships buzzed Taiwan again. Europe is watching Belarus, Ukraine, and energy storage with growing discomfort.

At the same time, Arab states are being pushed toward a broader regional realignment, China is tightening offshore stock-trading channels, Brussels is floating wealth-tax ideas, and Europe’s fiscal stress is becoming harder to hide.

That is not a calm world.

That is a world where politics is moving directly into markets.

This matters because geopolitics is not just “news.” It has a market transmission chain.

Middle East stress affects oil.

Oil affects inflation.

Inflation affects yields.

Yields affect valuations.

Valuations affect tech.

Tech affects the index.

Taiwan stress affects semiconductors.

Semiconductors affect AI.

AI affects capex.

Capex affects power demand.

Power demand affects energy markets.

Energy markets affect inflation.

This is how politics becomes portfolio risk.

Not all at once.

Then suddenly.

Bonds Are Still the Main Lesson

Our weekend bond essay got attention for a reason.

Bonds are no longer boring background furniture. They are the referee.

Goldman’s warning was blunt: if global real yields continue higher, the answer is “nothing good.” That matters because rising real yields are different from ordinary rate noise.

A nominal yield is the headline interest rate.

A real yield is the interest rate after inflation.

If real yields rise, money is getting tighter in a more meaningful way. Investors can earn more in safer assets after inflation, which makes expensive stocks harder to justify.

That is why higher real yields pressure markets.

They compete with equities.

They tighten financial conditions.

They raise the cost of debt.

They raise the bar for AI, tech, housing, private credit, and government spending.

This is the simple lesson:

When real yields rise, the market has to work harder.

And right now, stocks are working hard to pretend that does not matter.

AI Still Leads, But It Is Getting Crowded

AI remains the engine.

Semis are still being chased. Nvidia remains central. China AI is still ripping. Huawei is touting chip progress. Memory, compute, nuclear power, and data-center infrastructure are all being pulled into the same trade.

But crowded trades become fragile.

The more everyone agrees on the same story, the less room there is for disappointment.

That does not mean AI is fake.

It means the trade is mature.

The market is no longer just buying AI because the story is exciting. It is buying AI because it has become the default answer to nearly every macro problem.

That can work.

Until bonds, oil, politics, or geopolitics remind investors that no trade exists in a vacuum.

Investor View

This was a constructive day.

Breadth improved. Small caps participated. Tech held up. Volatility stayed calm.

But the risks are still visible.

Oil remains above $100. Real yields matter. Geopolitics is active. China is tightening financial channels. Europe is showing fiscal strain. The Middle East remains unstable. And the AI trade is increasingly crowded.

The rally is now balancing on several assumptions:

That oil stays contained.

That real yields stop rising.

That Iran headlines improve.

That China does not escalate around Taiwan.

That Europe can manage its fiscal strain.

That AI earnings keep justifying the chase.

That consumers keep spending.

That bonds stay cooperative.

The market is not pricing certainty.

It is pricing the hope that all of these risks remain manageable at the same time.

That may be enough for now.

But the lesson is clear:

The rally can survive noise.

It cannot easily survive a sustained rise in real yields, oil stress, political dysfunction, and geopolitical escalation all at once.

For now, stocks are still climbing.

That’s the daily.