Stocks finished the week higher, oil fell, and volatility stayed calm — but the market is still trading hope, not resolution.

Friday gave investors another green tape.

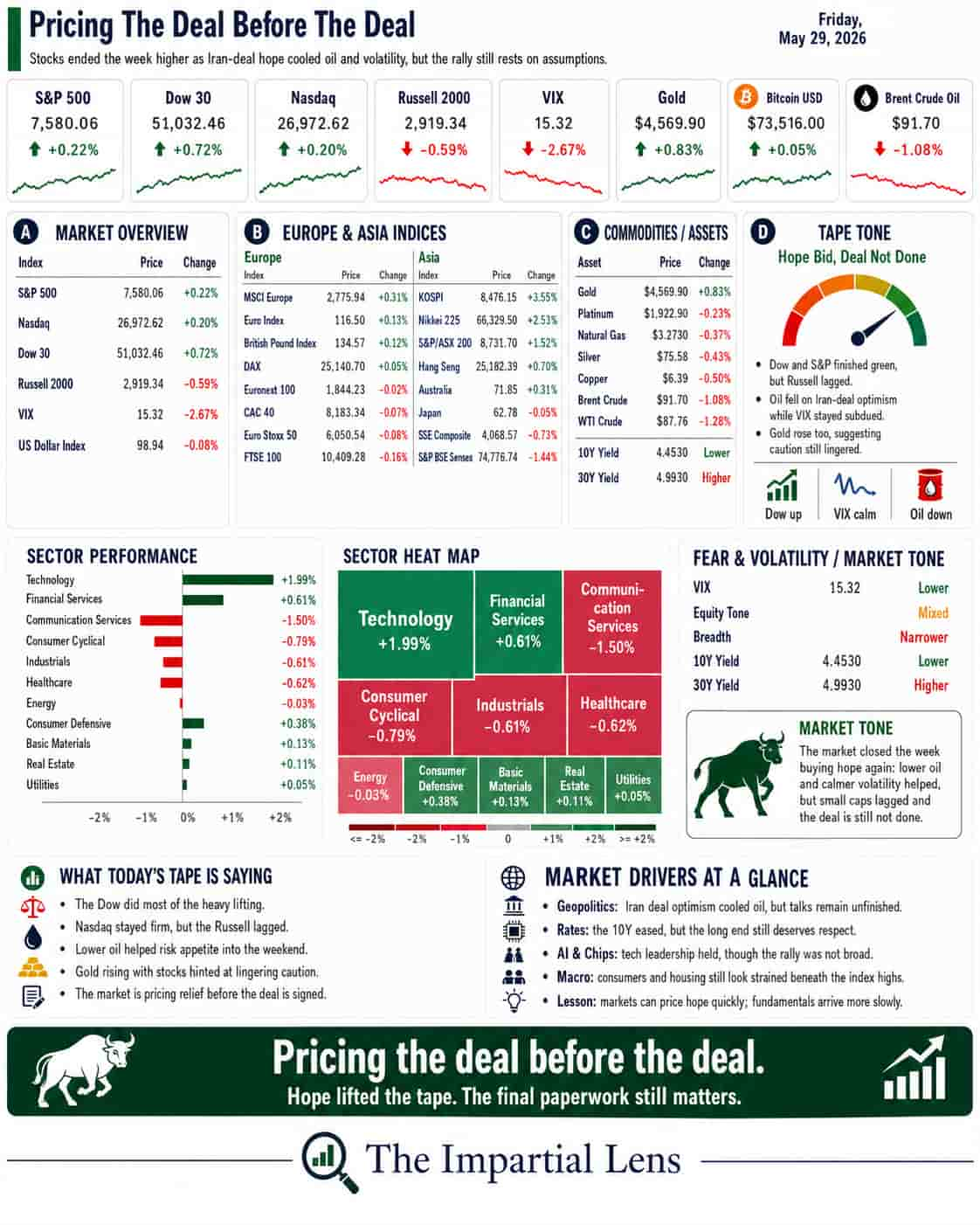

The S&P 500 rose 0.22%.

The Dow gained 0.72%.

The Nasdaq added 0.20%.

The Russell 2000 fell 0.59%.

The VIX dropped to 15.32.

Gold rose 0.83%.

Bitcoin was roughly flat.

Brent crude fell to about $91.70, down more than 1% on the day.

So, the screen looked calm.

But the calm came from a familiar source: the market is once again pricing progress on a U.S.-Iran deal before the deal is finished.

Both sides say an agreement is close. Trump says a final determination is coming soon. But the details still matter, including nuclear restrictions and the unfreezing of Iranian funds.

That is the first lesson:

Markets can rally on the expectation of peace.

But expectations are not policy.

And policy is not reality until it is signed, implemented, and survives the first violation.

The Dashboard Says: Green, But Uneven

The headline tape looked constructive.

The Dow led, the S&P moved higher, and the Nasdaq held firm. Technology was strong again, rising about 1.99%, while Financial Services gained 0.61%.

But the rally was not broad.

The Russell 2000 slipped. Communication Services fell sharply. Consumer Cyclical, Industrials, Healthcare, Energy, and Real Estate were all soft.

That matters.

A strong market with broad participation is one thing.

A market carried by a few leadership pockets while smaller companies lag is something else.

Friday looked more like selective strength than full confidence.

The market is still willing to buy big tech and AI-linked names.

It is less enthusiastic about the parts of the economy that depend on consumers, financing costs, and real-world demand.

Oil Is Falling, But the Story Is Not Finished

Oil had its biggest monthly drop in about a year.

That helped the market.

Lower oil reduces inflation pressure, help consumers, support margins, and give central banks more room to stay calm.

But the oil story is not clean.

The market is pricing an Iran deal. It is also pricing the idea that Hormuz risk is fading. Yet the headline stack still includes warnings that a ceasefire does not solve everything, that damage has already been done to energy infrastructure and supply chains, and that inventories remain dangerously tight.

Japan’s crude imports reportedly collapsed. Exxon and Chevron warned about extremely low inventory levels. RBC warned that treating Iran headlines as “over soon” could lead to a hard landing in oil.

So yes, oil is down.

That is helpful.

But lower oil prices today do not erase the structural risk.

If the deal fails, if shipping stress returns, or if inventories draw too far, the market could quickly rediscover why energy matters.

AI Is Still the Favorite Trade

AI stayed at the center of the tape.

Dell surged after AI-fueled earnings beat. Nvidia remained heavily traded. Semis continue to attract capital. AI data centers, nuclear power, and chip supply chains are all still part of the same story.

But the market is also starting to ask harder questions.

There were warnings about AI data-center funding, opaque accounting, massive Anthropic debt, and whether the real economy is benefiting from the AI buildout.

That is important.

The AI story is no longer just about revenue growth.

It is about funding.

It is about power.

It is about debt.

It is about energy.

It is about whether the infrastructure boom produces durable returns or simply creates the next financing problem.

The market still loves AI.

But it is no longer enough to say “AI” and expect every question to disappear.

Bonds Are Still the Quiet Test

Bonds remain central.

The market keeps acting as if lower oil automatically gives risk assets a clean runway. But the bond market still has the final vote.

Japan is preparing to slow or end quantitative tightening because bond-market turmoil is becoming harder to manage. U.S. inflation progress remains stalled according to Fed officials. Mortgage rates are still hurting housing. Consumer sentiment remains weak even as stocks sit near highs.

That is the tension.

Stocks are pricing optimism.

Consumers are pricing pressure.

Bonds are pricing discipline.

Those three cannot diverge forever.

The bond lesson remains simple:

When yields stay high, money stays expensive.

That pressures housing, credit, government debt, AI capex, and equity valuations.

The rally can keep going while bonds behave.

But if bonds start pushing back again, the tone changes quickly.

Politics is still on the Tape

Friday was also full of political risk.

Iran negotiations remained unresolved. Russia warned the U.S. against sending more troops near its borders. NATO condemned Russia after a drone hit Romania. Bessent signaled a crackdown on dark-money-funded NGOs. Courts remained active around Trump-related disputes. The U.S. seized Iranian crypto assets. China, Taiwan, sanctions, energy, and capital flows all stayed in the background.

This is why politics has to be part of the market read.

The market is not operating in a clean economic laboratory.

It is operating inside elections, wars, sanctions, capital controls, defense spending, energy insecurity, and central banks that are no longer free to ignore inflation.

That does not mean every headline deserves panic.

It means investors need to understand the chain:

Politics affects policy.

Policy affects energy, spending, and rates.

Rates affect valuations.

Valuations affect the market.

That is the mechanism.

The Real Read

Friday was constructive.

Stocks ended higher.

Volatility stayed low.

Oil fell.

Gold rose.

AI leadership remained alive.

The Iran deal narrative gave the market another reason to buy risk.

But the rally is still balancing on assumptions.

That the Iran deal gets finalized.

That oil keeps falling.

That bonds stay calm.

That AI earnings keep delivering.

That consumers keep spending.

That geopolitical stress remains contained.

That the real economy does not weaken beneath the index.

That is a lot to ask.

The market is not pricing certainty.

It is pricing hope with momentum behind it.

That can work.

For a while.

But the lesson of the week is clear:

Relief can lift markets.

It does not remove the underlying risk.

The market may be right to rally.

But it is still buying the deal before the deal is done.

And that is always a more fragile trade than it looks.