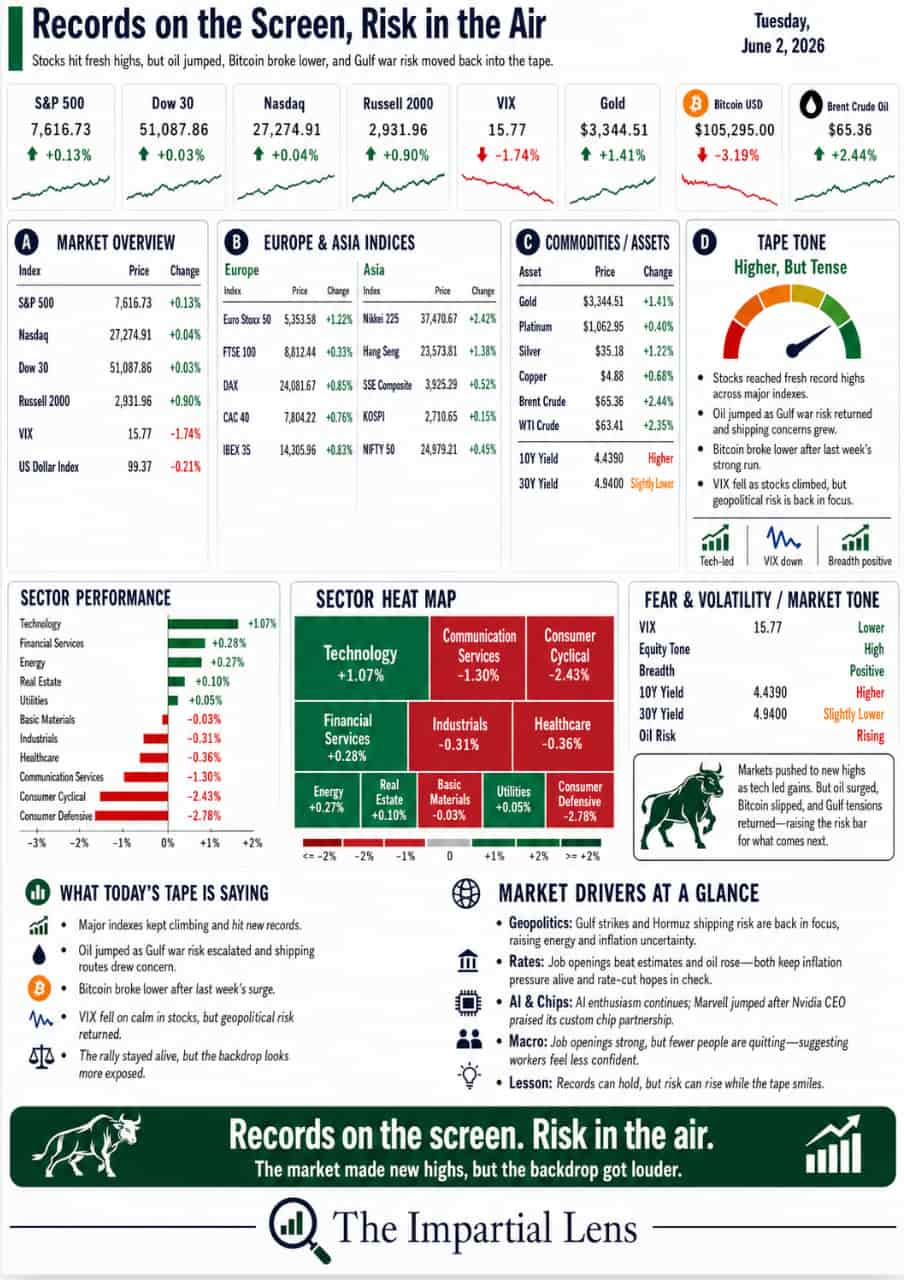

Stocks pushed to fresh highs again, but the market is now juggling a dangerous mix: AI enthusiasm, Middle East escalation, rising oil risk, strange labor data, and investors who still do not want protection.

Tuesday gave investors another green-looking tape.

The major indices pushed to fresh intraday records. The S&P 500, Dow, and Nasdaq 100 all touched new highs. Tech remained supported. AI enthusiasm stayed alive. Semis kept drawing money. Software suddenly found buyers again. Retail appetite remained strong.

On the surface, that looks bullish.

But underneath, the picture was not nearly as clean.

Oil rose as U.S.-Iran headlines turned messy again. Bitcoin was hit hard. Geopolitical risk flared across the Gulf. Job openings jumped far more than expected, but workers were not acting confident. European inflation pushed above 3%. And the market continued to behave as if risk has been politely retired.

It has not.

The market is still climbing.

But the air is getting thinner.

The Dashboard Says: Higher, But Not Healthier

The big message from the tape was simple: investors still want risk.

Stocks extended record levels. AI names kept attracting flows. Marvell rallied after Nvidia’s CEO suggested it could become a trillion-dollar company. Tencent surged on reports that it may launch an AI agent inside WeChat. Software saw a major retail inflow after being ignored for months.

That is real momentum.

But a market can go higher while becoming more fragile.

Several headlines pointed to the same problem: more AI, no protection. Nobody wants downside hedges. Investors are still chasing crowded themes. And the S&P has been rising even on days when more stocks declined than advanced.

That matters.

If an index rises while participation weakens, the headline number can mislead you.

The market looks stronger from the top than it feels underneath.

That is not a crash signal.

But it is a quality warning.

Geopolitics Is Back in the Driver’s Seat

The biggest story was not just AI.

It was war risk.

Iran reportedly launched missiles and drones targeting airbases across the Gulf after a U.S. nighttime attack on Qeshm Island. Explosions and sirens were reported in Kuwait, Saudi Arabia, the UAE, and Bahrain. U.S.-Iran talks were reportedly halted, though Trump called that fake news. Israel and Lebanon had still not reached a final ceasefire. Russia unleashed a major bombardment across Ukraine. The U.S. and China held military deconfliction talks in Hawaii. Taiwan remained in the background.

This is not background noise.

This is the market’s operating system now.

Hormuz affects oil.

Oil affects inflation.

Inflation affects bonds.

Bonds affect valuations.

Valuations affect tech.

Tech affects the index.

That is the chain.

The market keeps trying to skip straight to “AI goes up.”

But geopolitics keeps pulling the conversation back to energy, inflation, supply chains, and defense risk.

That is why this matters.

Oil Is the Real-Time Geopolitical Barometer

Oil rose as the headlines worsened.

That makes sense.

When missiles and drones are moving near the Gulf, crude becomes the market’s first pressure gauge. The Strait of Hormuz remains one of the most important energy chokepoints in the world, and even the threat of disruption can quickly change inflation expectations.

There were also warnings that Europe would have serious problems if U.S. oil exports were reduced. Norway strike risk added another layer of energy uncertainty. Grain prices surged. Copper forecasts were lifted. Venezuela exports hit a seven-year high as buyers search for supply.

This is the world the market is trading inside.

Energy is no longer just a commodity story.

It is a geopolitical story.

It is an inflation story.

It is a consumer story.

It is a bond-market story.

And right now, oil risk is not gone just because traders want peace headlines to work.

The Labor Data Was Strange

The JOLTS report delivered a shock.

Job openings jumped by more than 700,000, far above expectations. Normally, that would suggest a strong labor market.

But quits fell to a six-year low.

That is odd.

When workers feel confident, they quit jobs to find better ones. When quits fall, it can mean workers are becoming less confident, even if job openings still look strong.

So, the labor message was mixed.

Companies may still be posting jobs.

But workers may be getting more cautious.

That matters because the consumer is still the backbone of the economy.

If consumers are nervous, wages are pressured, fuel costs rise, and inflation remains sticky, the market’s “everything is fine” story gets harder to defend.

Bonds Still Get the Final Vote

The bond story is still central.

Eurozone inflation topped 3% for the first time since 2023, strengthening the case for an ECB hike. Fed officials warned inflation trends still need to cool. U.S. job openings surprised to the upside. Oil rose. Commodities stayed active.

That is not a clean backdrop for rate cuts.

The market wants easier policy.

But the data keeps complicating that wish.

The simple bond lesson is this:

If growth holds up and inflation stays sticky, central banks have less room to cut.

That keeps real yields relevant.

And if real yields stay high, expensive assets have to keep justifying themselves every day.

That includes AI.

Especially AI.

AI Is Still the Engine — But the Cost Question Is Growing

AI remains the dominant market force.

But the story is shifting.

The early AI story was about possibility.

Now it is about cost.

Alphabet is reportedly raising massive capital for AI spending. Data centers need power. Chips need memory. Token costs are rising. GitHub users felt the meter turn on. Bain warned that AI cost savings are falling short of projections. Hyperscalers are spending aggressively, but investors are starting to ask whether the value is arriving fast enough.

That is an important change.

AI is still powerful.

But it is no longer free magic in the cloud.

It is infrastructure.

And infrastructure costs money.

The Real Read

Tuesday was constructive on the surface.

Stocks made new highs.

AI stayed strong.

Tech kept leading.

Retail kept chasing.

Software joined the party.

But the risks are getting louder.

Oil rose.

Bitcoin was battered.

Geopolitics escalated.

Iran headlines worsened.

Ukraine was hit again.

Labor data turned strange.

Europe inflation rose.

And investors still showed little interest in protection.

The market is not pricing certainty.

It is pricing faith.

Faith that oil stays contained.

Faith that Iran does not spiral.

Faith that central banks can manage inflation.

Faith that AI spending keeps paying off.

Faith that consumers keep going.

Faith that bonds do not push back.

That is a lot of faith.

The lesson is clear:

A market can make new highs and still become more vulnerable underneath.

For now, the rally still works.

But the higher it climbs on AI, momentum, and relief headlines, the more sensitive it becomes to anything that breaks the story.

The screen says strength.

The backdrop says caution.

Both can be true.