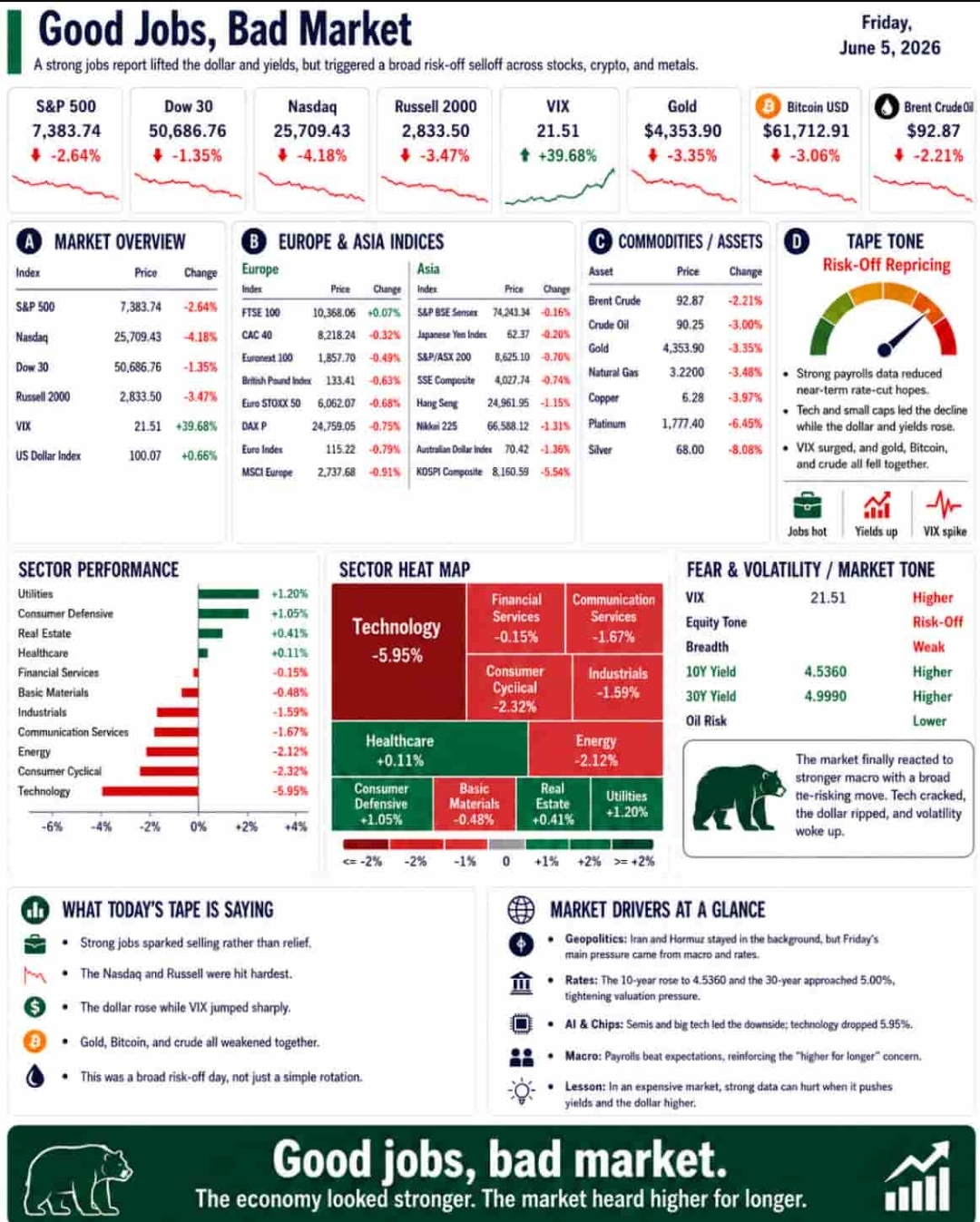

Friday delivered the kind of market reaction that often confuses everyday investors.

The U.S. jobs report came in strong. Payrolls rose by 172,000 in May, beating expectations, while the unemployment rate held steady at 4.3%. On paper, that sounds healthy.

But the market did not celebrate.

Stocks fell. Tech was hit hard. Semis were slaughtered. The dollar surged. Bitcoin weakened. Fear returned to Wall Street. And the S&P’s historic win streak ended abruptly.

That is the key lesson: Good news is not always good news for markets.

When inflation remains sticky, oil risks linger, and the Fed lacks clear room to cut rates, strong jobs data can quickly become a problem. It signals an economy still too warm for easy money — precisely the opposite of what this rally has been pricing in.

The Dashboard Says: Fear Came Back

The tone shifted sharply.

For weeks, investors chased AI, semis, leverage, upside calls, and anything tied to the hottest trade. Protection was out of favor.

On Friday, that flipped. Headlines screamed “Fear Returns to Wall Street” and “Semis Slaughtered.” Risk-on positioning, already stretched to pre-pandemic extremes, suddenly looked vulnerable.

Crowded trades rarely unwind gracefully. When everyone leans the same way — especially with leverage — the first crack can trigger rapid selling. The market wasn’t just reacting to one jobs number. It was reacting to a stretched setup colliding with data that made rate cuts harder to justify.

The Strong Jobs Report Was a Problem for Rate-Cut Hopes

The payrolls number disrupted the market’s favorite narrative:

- Growth slows gently.

- Inflation cools.

- The Fed gains room to cut.

- AI earnings keep rising.

- Stocks keep climbing.

Friday complicated that story. A robust labor market makes it tougher for the Fed to justify immediate support. It also leaves policymakers more cautious amid sticky inflation or rising oil risks.

This doesn’t mean rate cuts are off the table — but the bar is now higher. And when stocks are priced for perfection, a higher bar is rarely welcome.

The clean read: A hot jobs report supports the economy, but it also supports higher-for-longer rates. That tension explains why the market sold off.

Semis Were the Pressure Point

The clearest weakness appeared in semiconductors — the engine of the entire rally.

The AI trade (semis, memory, data centers, hyperscalers, and infrastructure) has carried market psychology for months. On Friday, the most crowded segment finally looked exposed. Korean chip stocks weakened, SK Hynix took a hit, sentiment around Nvidia and peers soured, and Broadcom’s earlier disappointment lingered. Investors began questioning whether the AI boom had grown too crowded, too leveraged, and too dependent on uninterrupted good news.

This does not mean AI is over. That would be simplistic. It means the market is shifting from blind enthusiasm to scrutiny.

The easy question — “Is AI important?” — has been answered with a resounding yes. The harder one now is: “How much of that importance has already been priced in?” That’s where the risk resides.

Geopolitics Stayed in the Tape

The Middle East remained active and messy. U.S. forces reportedly downed Iranian drones over the Strait of Hormuz and struck coastal sites. Air defenses activated over Kuwait. Iran’s oil exports reportedly plunged amid tighter blockades. Meanwhile, reports suggested narrowing gaps in U.S.-Iran talks, though frozen funds continued to complicate progress.

This was not resolution — it was negotiation under pressure.

The market craves a clean peace narrative, but reality stays complicated: strikes, drones, sanctions, oil flows, frozen assets, and shifting red lines.

Geopolitics flows straight into markets:

Hormuz → oil → inflation → rates → valuations → tech → the index.

That chain remains intact. Friday showed the market is less willing to ignore it when rates are already moving against the rally.

The Dollar Sent a Message

The dollar surged — and that mattered.

A stronger dollar often signals tighter financial conditions, demand for safety, or revised rate expectations. Here, the strong jobs data forced investors to reconsider how quickly the Fed could ease.

A firmer dollar pressures commodities, emerging markets, multinational earnings, and overall risk appetite. When stocks fall, semis weaken, Bitcoin drops, and the dollar rises in tandem, the message is clear: liquidity expectations just tightened.

AI Is Still the Story — But the Story Is Changing

AI remains the dominant theme, yet the tone is evolving.

Fresh concerns emerged around data-center spending, token commoditization, AI capex, and potential over-allocation. Meta reportedly weighed large stock sales, SpaceX IPO talk swirled, nuclear power kept surfacing in infrastructure discussions, and electricity prices stayed relevant.

The recurring insight: AI is not just software. It is chips, power, financing, cooling, land, labor, and policy. The more physical and capital-intensive the boom becomes, the harder it is for AI to ignore macro forces like rates, energy costs, and geopolitics.

The Real Read

Friday delivered a warning.

The economy looked strong. The market did not like it. Jobs beat expectations, the dollar jumped, semis came under pressure, Bitcoin weakened, fear returned, geopolitics stayed relevant, and rate-cut hopes grew harder to defend.

The lesson is clear: Strong data is bullish only when inflation is under control. When it instead points to higher yields, fewer cuts, and tighter conditions, good news becomes toxic for expensive markets.

This does not mean the rally is over. But it does mean the setup is more fragile than it appeared during the win streak.

The rally had rested on three key assumptions:

- AI keeps delivering.

- The Fed eventually helps.

- Geopolitics stays contained.

Friday challenged all three at once.