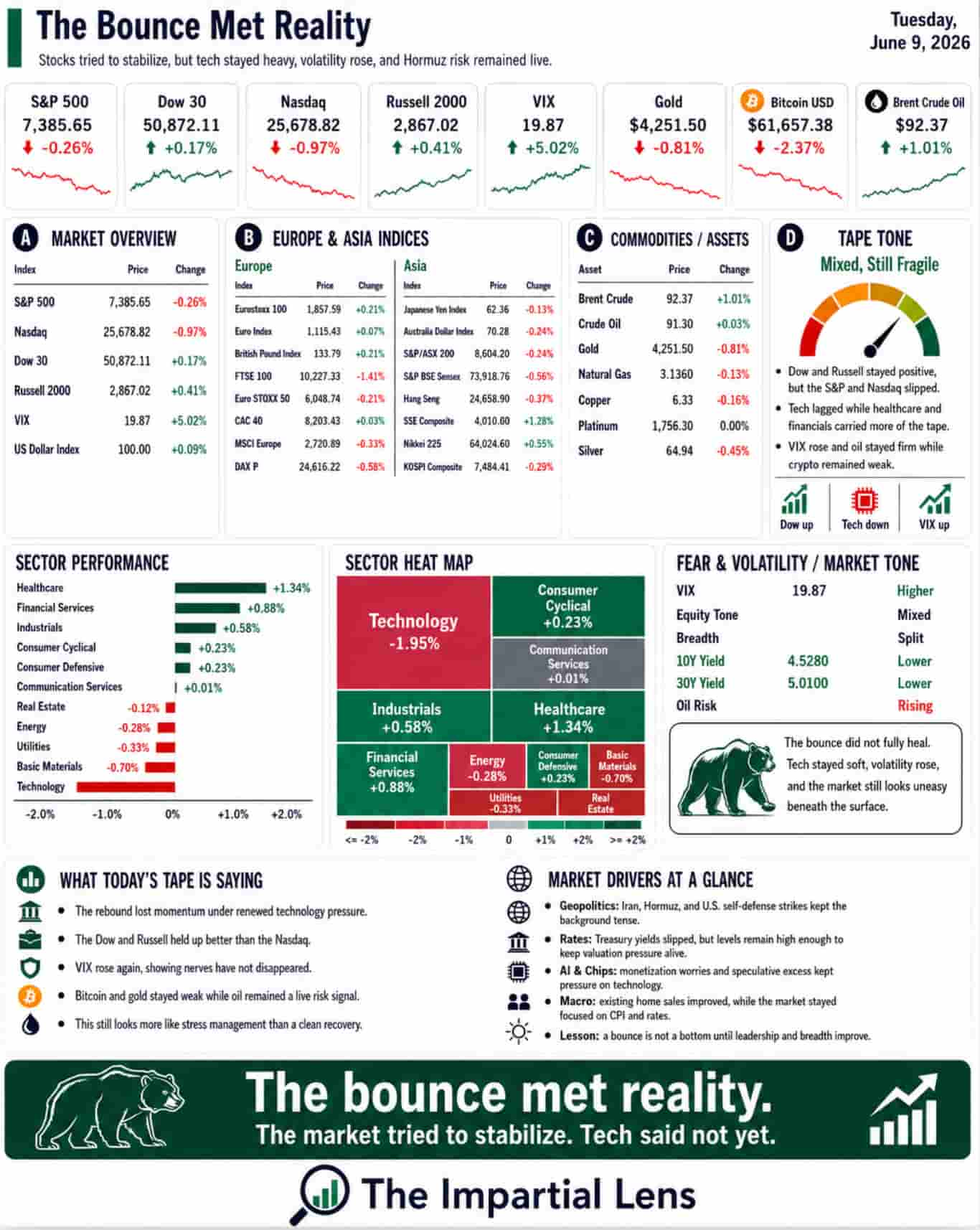

Monday gave the market a bounce. Tuesday asked for proof. The proof didn’t arrive.

After Friday’s sharp selloff, stocks attempted a recovery. Dip-buyers showed up, tech rebounded, Bitcoin stabilized, and sentiment briefly improved. It felt like the healthy reset bulls wanted.

Then Tuesday hit. Tech rolled over again. The S&P and Nasdaq retested Friday’s lows. AI names looked fragile. And the Middle East reminded everyone it doesn’t take orders from Wall Street.

This is the problem with relief rallies: they feel good in the moment, but they still have to prove themselves.

Tuesday was that test. The bounce failed.

The Market Is Learning a Painful Lesson

For months, investors leaned on a simple three-legged stool:

- AI would keep leading

- The Fed would eventually ride to the rescue

- Geopolitics would stay contained

Friday kicked the Fed leg with strong jobs data that reduced rate-cut odds. Tuesday kicked the AI leg as tech selling resumed. Geopolitics continues leaning heavily on the third.

The stool hasn’t collapsed — but it’s getting wobbly.

Tech Is No Longer Getting a Free Pass

Tech, and especially AI, has carried this entire rally. It was the convenient answer to every concern: oil risks, higher yields, weak consumers, deficits — just buy more AI.

Tuesday showed that patience is wearing thin.

The conversation has shifted. It’s no longer “Is AI real?” (Of course it is.) The harder, less exciting question now is:

“Who actually makes real money once you subtract the massive spending on chips, power, data centers, cooling, and debt?”

AI has moved from the dream phase to the accounting phase. That’s usually where the fun dies.

The Casino Is Still Open — But the Lights Flickered

Huge leveraged positions remain tied to semiconductors and AI infrastructure. Leverage works beautifully on the way up. On the way down, it turns normal selling into forced, mechanical selling.

The issue isn’t whether companies like Nvidia, Broadcom, or SK Hynix matter. They do. The issue is whether too many investors tried to own the exact same future at the exact same time.

Crowded trades break. Explanations usually come afterward.

Hormuz Is Becoming a Structural Risk

Markets have been treating the Strait of Hormuz as a short-term headline risk. Tuesday forced a darker question:

What if it never fully returns to normal?

Slow shocks are especially dangerous. Shipping disruptions don’t need daily explosions — just sustained impairment. Inventories draw down. Insurance costs rise. Routes lengthen. Costs compound. Consumers eventually feel it in higher energy and food prices.

This isn’t a one-day oil spike. It’s a potential new baseline with a permanent geopolitical risk premium. Markets are not priced for that scenario.

War Risk Is Spreading

U.S. strikes, Iranian threats, activity in Lebanon, and Gulf states ramping up counter-drone defenses all point to the same thing: the region is preparing for a more dangerous normal.

This isn’t temporary noise. It’s the rising cost of doing business — for energy, shipping, insurance, and defense.

Inflation Is Waiting In The Corner

All of this flows straight back to inflation.

Oil disruption hits energy → which hits transport → which hits food → which hits consumers → which hits politics → which ties the Fed’s hands.

The market wants to skip the messy middle and go straight back to “buy the dip.” But if CPI stays sticky, jobs remain firm, and oil risks linger, there’s no quick Fed rescue coming.

No cape. No easy pivot. Just higher-for-longer with better lighting.

The Real Read

Tuesday wasn’t dramatic because the world ended. It was dramatic because the market tried to bounce — and couldn’t.

Tech weakened again. AI lost some of its magic. Leveraged positions stayed exposed. Oil inflation risk stayed alive. Geopolitics moved deeper into the market’s plumbing.

The market is no longer trading on one clean story. It’s juggling multiple fragile assumptions at once:

- AI must deliver

- Oil risks must stay contained

- The Fed must not tighten further

- CPI must behave

- Consumers must hold up

- Crowded trades must unwind gently

That’s a lot of “musts.”

Tuesday didn’t break the market. But it delivered a clear message: a bounce is not a bottom. And in this environment, hope still needs financing.